In our last blogpost, we discussed method 1 - spread the conversion tax cost. Now we will discuss method 2 below.

Method 2. Consider a Charitable Contribution

For high-income earners, a charitable contribution is a method worth considering. The tax deduction for a contribution to a public charity can be up to 60% of adjusted gross income (AGI) for cash donations and up to 30% for donations of securities (generally deductible at fair market value when long-term appreciated securities are gifted) in a given year. And if a contribution exceeds these limits, the excess can generally be carried forward for up to 5 years.

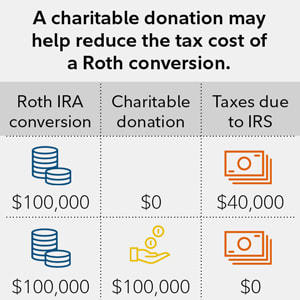

The amount of the charitable deduction available to claim can generally be estimated by adding the taxable portions of a conversion amount to AGI. For example, for those planning to convert $200,000 to a Roth IRA, with a $150,000 AGI before the conversion, the estimated AGI would be $350,000 after the conversion. Up to $210,000 (60% of $350,000) of a charitable cash contribution or $105,000 (30% of AGI) of a charitable donation of securities with long-term appreciation, could potentially be deducted. This could significantly reduce the tax impact of a conversion. See illustration below.

Method 2. Consider a Charitable Contribution

For high-income earners, a charitable contribution is a method worth considering. The tax deduction for a contribution to a public charity can be up to 60% of adjusted gross income (AGI) for cash donations and up to 30% for donations of securities (generally deductible at fair market value when long-term appreciated securities are gifted) in a given year. And if a contribution exceeds these limits, the excess can generally be carried forward for up to 5 years.

The amount of the charitable deduction available to claim can generally be estimated by adding the taxable portions of a conversion amount to AGI. For example, for those planning to convert $200,000 to a Roth IRA, with a $150,000 AGI before the conversion, the estimated AGI would be $350,000 after the conversion. Up to $210,000 (60% of $350,000) of a charitable cash contribution or $105,000 (30% of AGI) of a charitable donation of securities with long-term appreciation, could potentially be deducted. This could significantly reduce the tax impact of a conversion. See illustration below.

RSS Feed

RSS Feed