The client

Age 75 to 85; has $150,000 from a large build up in a Non-Qualified Annuity not subject to surrender charges or money from a CD; views proceeds as lazy or emergency money.

The situation

Client is concerned about efficiently funding an extended health care or Long-Term Care (LTC) event. Has already identified assets to use but wants preservation of their capital, a reasonable rate of return and access and control over their money if they need it. The agent’s current BD doesn’t allow sale of Indexed Annuities.

A solution

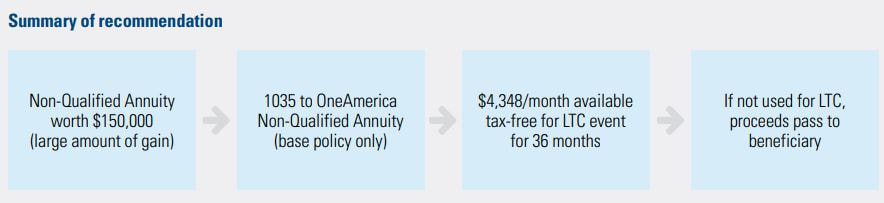

To address the specific concerns of the client, a 1035 transfer to Annuity Care, base policy only, may be a possible solution.

This solution offers the client on $150,000:

• The ability to access gains tax-free for extended care or LTC events

• A 34.8% tax-free income stream for 36 months ($4,348 a month) for qualifying LTC expenses

• Can add a spouse or other insured giving both access to the full monthly benefit

• Retain access and control over the assets just like in their current annuity

• No medical underwriting or cognitive phone interview for base policy only

• Ability to add a rider doubling pool of assets or lifetime coverage (requires cognitive phone interview)

Age 75 to 85; has $150,000 from a large build up in a Non-Qualified Annuity not subject to surrender charges or money from a CD; views proceeds as lazy or emergency money.

The situation

Client is concerned about efficiently funding an extended health care or Long-Term Care (LTC) event. Has already identified assets to use but wants preservation of their capital, a reasonable rate of return and access and control over their money if they need it. The agent’s current BD doesn’t allow sale of Indexed Annuities.

A solution

To address the specific concerns of the client, a 1035 transfer to Annuity Care, base policy only, may be a possible solution.

This solution offers the client on $150,000:

• The ability to access gains tax-free for extended care or LTC events

• A 34.8% tax-free income stream for 36 months ($4,348 a month) for qualifying LTC expenses

• Can add a spouse or other insured giving both access to the full monthly benefit

• Retain access and control over the assets just like in their current annuity

• No medical underwriting or cognitive phone interview for base policy only

• Ability to add a rider doubling pool of assets or lifetime coverage (requires cognitive phone interview)

RSS Feed

RSS Feed