If you own company stocks, there is a tax break that could save you a bundle on taxes—if you qualify.

What Is NUA?

Anyone who owns company stock will eventually have to decide how to distribute those assets—typically when you retire or change employers. Taking a distribution could leave you facing a tax bill, but a little-known tax break—dealing with net unrealized appreciation (NUA)—has the potential to help.

NUA is the difference between the price you initially paid for a stock (its cost basis) and its current market value. Say you can buy company stock in your plan for $20 per share, and you use $2,000 to purchase 100 shares. Five years later, the shares are worth $35 each, for a total value of $3,500: $2,000 of that figure would be your cost basis and $1,500 would be NUA.

A Case Study

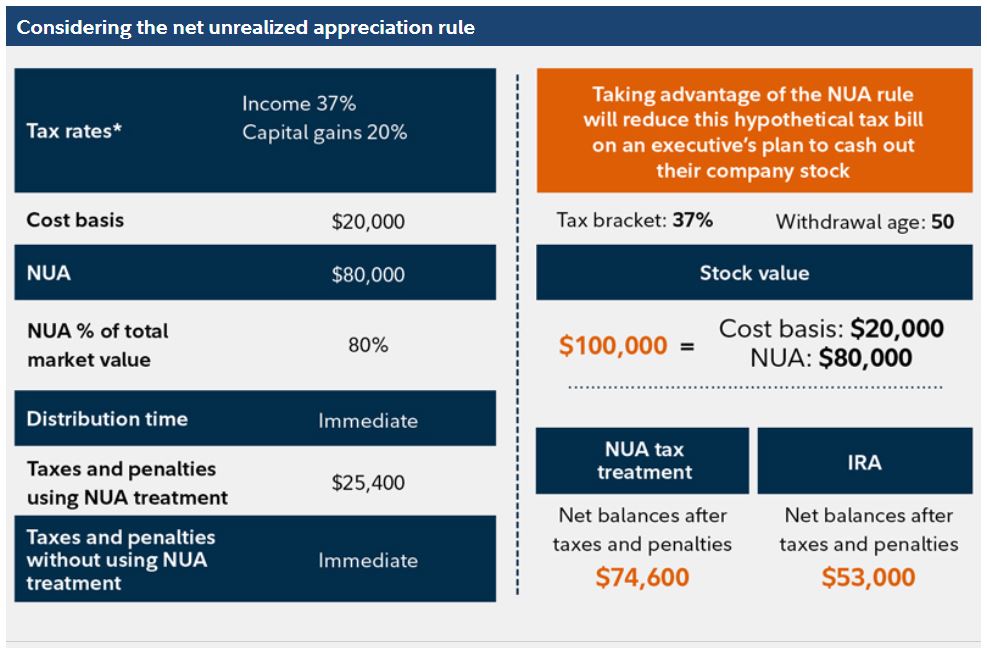

An executive in the 37% tax bracket decides to retire at age 50. She holds $100,000 worth of company stock with a cost basis of $20,000, resulting in NUA of $80,000, and she wants immediate access to the cash.

She decides to distribute the assets into a taxable account and elect NUA tax treatment. She pays income tax and a 10% early withdrawal penalty on just her $20,000 cost basis—a total of $9,400. She then immediately sells her company stock and pays 20% capital gains tax on the stock's $80,000 NUA. In all, she pays taxes and penalties of $25,400, leaving her with $74,600.

Imagine she instead rolled her company stock into an IRA, then sold the shares and withdrew the cash. In that case, she would pay income tax and penalties on the entire $100,000, for a total of $37,000 in income tax and $10,000 in early withdrawal penalties. As a result, she would wind up with just $53,000.

What Is NUA?

Anyone who owns company stock will eventually have to decide how to distribute those assets—typically when you retire or change employers. Taking a distribution could leave you facing a tax bill, but a little-known tax break—dealing with net unrealized appreciation (NUA)—has the potential to help.

NUA is the difference between the price you initially paid for a stock (its cost basis) and its current market value. Say you can buy company stock in your plan for $20 per share, and you use $2,000 to purchase 100 shares. Five years later, the shares are worth $35 each, for a total value of $3,500: $2,000 of that figure would be your cost basis and $1,500 would be NUA.

A Case Study

An executive in the 37% tax bracket decides to retire at age 50. She holds $100,000 worth of company stock with a cost basis of $20,000, resulting in NUA of $80,000, and she wants immediate access to the cash.

She decides to distribute the assets into a taxable account and elect NUA tax treatment. She pays income tax and a 10% early withdrawal penalty on just her $20,000 cost basis—a total of $9,400. She then immediately sells her company stock and pays 20% capital gains tax on the stock's $80,000 NUA. In all, she pays taxes and penalties of $25,400, leaving her with $74,600.

Imagine she instead rolled her company stock into an IRA, then sold the shares and withdrew the cash. In that case, she would pay income tax and penalties on the entire $100,000, for a total of $37,000 in income tax and $10,000 in early withdrawal penalties. As a result, she would wind up with just $53,000.

In our next blogpost, we will discuss how to qualify for NUA treatment and when to choose NUA treatment.

RSS Feed

RSS Feed