If you are interested in knowing more about this product from American National, please contact us.

|

|

|

If you are interested in knowing more about this product from American National, please contact us.

0 Comments

In our last blogpost, we discussed how to qualify for NUA treatment.

Now we will discuss when to use NUA treatment. You should consider the following factors as you decide whether to roll all your assets into an IRA or to transfer company stock separately into a taxable account:

Please consult your tax advisor for more details, this blog series is for information only. In our last blogpost, we discussed what is NUA and used a case study to show how it could be used to get tax break.

Now we will discuss how to qualify for NUA treatment. You must meet all 4 of the following criteria to take advantage of the NUA rules:

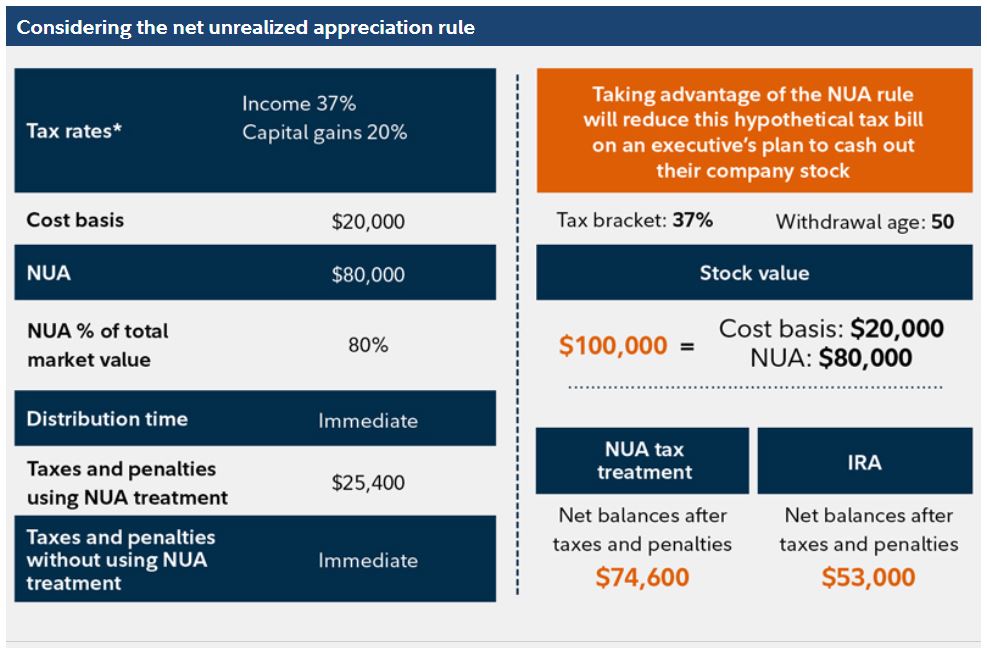

The IRS enforces these rules strictly, if you do not meet one of the criteria—for example, if you fail to distribute all assets within one tax year - your NUA election will be disqualified, and you would owe ordinary income taxes and any penalty on the entire amount of the company stock distribution. For more information on these complex rules, as well as situations that trigger additional tax restrictions, review IRS Publication 575, Pension and Annuity IncomeOpens in a new window, which is available at IRS.gov. In our next blogpost, we will discuss when to use NUA treatment. If you own company stocks, there is a tax break that could save you a bundle on taxes—if you qualify. What Is NUA? Anyone who owns company stock will eventually have to decide how to distribute those assets—typically when you retire or change employers. Taking a distribution could leave you facing a tax bill, but a little-known tax break—dealing with net unrealized appreciation (NUA)—has the potential to help. NUA is the difference between the price you initially paid for a stock (its cost basis) and its current market value. Say you can buy company stock in your plan for $20 per share, and you use $2,000 to purchase 100 shares. Five years later, the shares are worth $35 each, for a total value of $3,500: $2,000 of that figure would be your cost basis and $1,500 would be NUA. A Case Study An executive in the 37% tax bracket decides to retire at age 50. She holds $100,000 worth of company stock with a cost basis of $20,000, resulting in NUA of $80,000, and she wants immediate access to the cash. She decides to distribute the assets into a taxable account and elect NUA tax treatment. She pays income tax and a 10% early withdrawal penalty on just her $20,000 cost basis—a total of $9,400. She then immediately sells her company stock and pays 20% capital gains tax on the stock's $80,000 NUA. In all, she pays taxes and penalties of $25,400, leaving her with $74,600. Imagine she instead rolled her company stock into an IRA, then sold the shares and withdrew the cash. In that case, she would pay income tax and penalties on the entire $100,000, for a total of $37,000 in income tax and $10,000 in early withdrawal penalties. As a result, she would wind up with just $53,000.  In our next blogpost, we will discuss how to qualify for NUA treatment and when to choose NUA treatment.

Money really can buy happiness, as it turns out — but you might not need as much as you think.

A large analysis published in the journal Nature Human Behavior used data from the Gallup World Poll, a survey of more than 1.7 million people from 164 countries, to put a price on optimal emotional well-being: between $60,000 and $75,000 a year. That aligns with past research on the topic, which found that people are happiest when they make about $75,000 a year. But while that may be the sweet spot for feeling positive emotions on a day-to-day basis, the researchers found that a higher figure — $95,000 — is ideal for “life evaluation,” which takes into account long-term goals, peer comparisons, and other macro-level metrics. The researchers, from Purdue University, also found that it may be possible to make too much money, as far as happiness is concerned. They observed declines in emotional well-being and life satisfaction after the $95,000 mark, perhaps because being wealthy — past the point required for daily comfort and purchasing power, at least — can lead to unhealthy social comparisons and unfulfilling material pursuits. Still, the findings don’t mean that getting a huge raise won’t lead to individual satisfaction: It simply suggests, according to the researchers, that a group of people making $200,000 a year is likely no happier than a group of people making $95,000. The well-documented “hedonic treadmill” phenomenon also suggests that people adjust relatively quickly to their newly flush bank accounts, with happiness leveling back off over time. In the new study, the researchers note that their estimates pertain specifically to individuals, and ideal household income is likely higher. Plus, while the figures in the paper represent global estimates, earning satisfaction also varies widely around the world, and in urban versus rural areas within countries. Certain regions — Western Europe, North America, Australia, New Zealand, East Asia, and the Middle East — had higher financial thresholds for both emotional well-being and life evaluation, while areas including Eastern Europe, Southeast Asia, Latin America, and Sub-Saharan Africa were lower than the global numbers. All told, the ideal income for life evaluation ranged from $35,000 in Latin America to $125,000 in Australia and New Zealand. In North America, the optimal amount for life evaluation was estimated at $105,000, and the range for emotional well-being was slated at $65,000 to $95,000. The researchers didn’t observe significant differences between men and women, but they did find that education level influenced monetary ideals. Highly educated people tended to have loftier income satisfaction points, likely because they had higher expectations of wealth and were more susceptible to social comparison. All said if your income is below — or above — the researchers’ ideal threshold, don’t despair. Research suggests that while money can buy happiness, the quality of your spending is just as important as the quantity. For archived newsletters, please visit here.

|

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed