Q. What is 2019 retirement plan contribution limit?

A. The Internal Revenue Service has issued the new benefit and contribution limits for qualified retirement plans for plan years beginning in 2019.

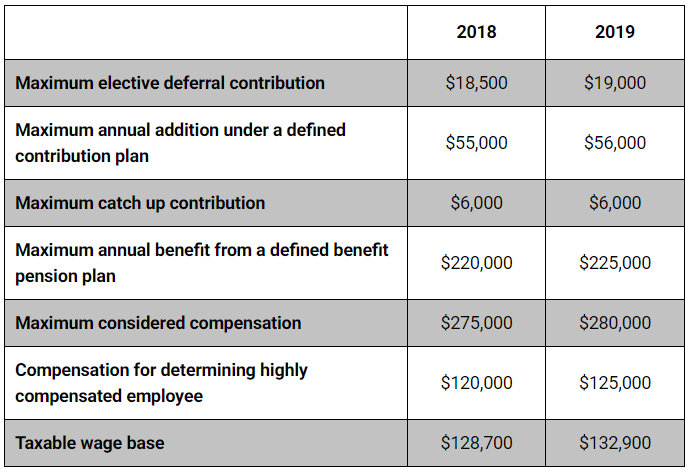

Below are some of the key limitation amounts for the upcoming year.

A. The Internal Revenue Service has issued the new benefit and contribution limits for qualified retirement plans for plan years beginning in 2019.

Below are some of the key limitation amounts for the upcoming year.

RSS Feed

RSS Feed