The last blogpost showed one advantage of annuity over bond. Now the second advantage -

It Costs Less to Fund Retirement with Annuities Vs. Bond Ladders

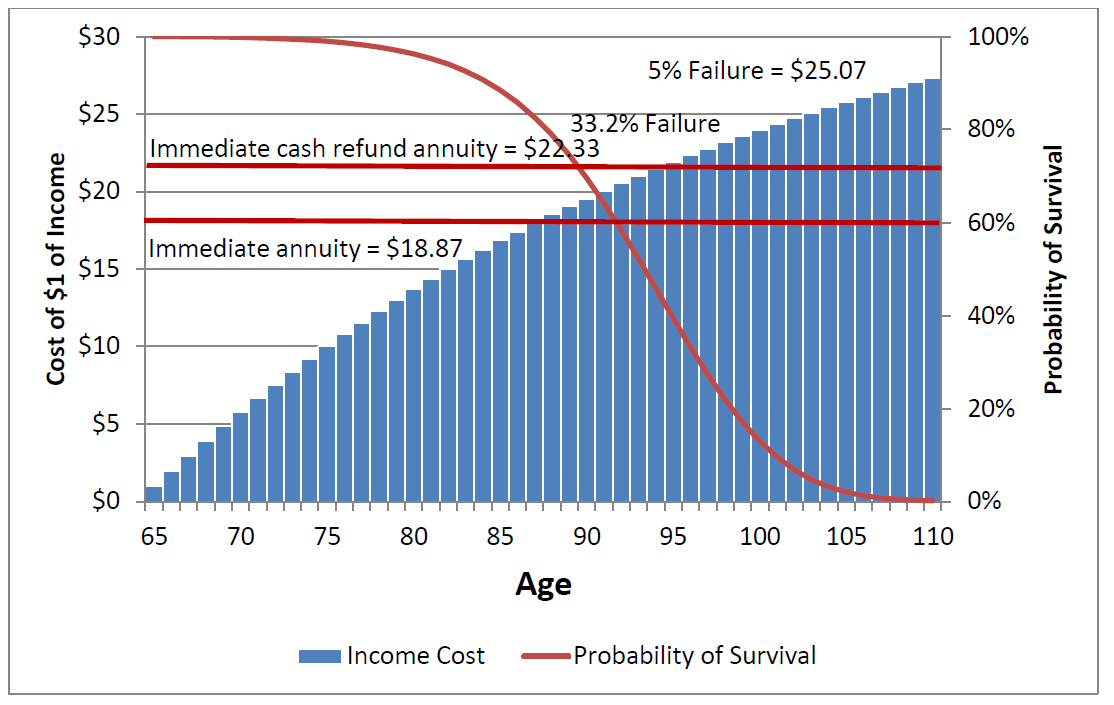

David Blanchett, Head of Retirement Research at Morningstar Investment Management, and Michael Finke, Dean at The American College, also studied annuities in their paper “Annuitized Income and Optimal Asset Allocation.” Using a slightly different lens than Professor Pfau, they compared setting money aside at retirement to either (a) fund a bond ladder or (b) buy an immediate income annuity.

Creating enough income through a bond ladder to last long enough for 95% of couples’ lives costs $25.07 for every dollar of annual income needed. For example, if a 65-year-old couple wanted to spend $100,000 per year, it would require them to set aside 25.07x today, or $2,507,000.

To create that same $100,000 per year by buying an immediate income annuity, it would cost only 18.87x, or $1,887,000, and the money would last for 100% of couples’ lives. (They also looked at a more expensive immediate income annuity that includes a refund at premature death, for which the cost was a little higher at 22.33x.)

It Costs Less to Fund Retirement with Annuities Vs. Bond Ladders

David Blanchett, Head of Retirement Research at Morningstar Investment Management, and Michael Finke, Dean at The American College, also studied annuities in their paper “Annuitized Income and Optimal Asset Allocation.” Using a slightly different lens than Professor Pfau, they compared setting money aside at retirement to either (a) fund a bond ladder or (b) buy an immediate income annuity.

Creating enough income through a bond ladder to last long enough for 95% of couples’ lives costs $25.07 for every dollar of annual income needed. For example, if a 65-year-old couple wanted to spend $100,000 per year, it would require them to set aside 25.07x today, or $2,507,000.

To create that same $100,000 per year by buying an immediate income annuity, it would cost only 18.87x, or $1,887,000, and the money would last for 100% of couples’ lives. (They also looked at a more expensive immediate income annuity that includes a refund at premature death, for which the cost was a little higher at 22.33x.)

The annuity costing less than the bond ladder has two important implications:

If you have digested the information and are convinced that annuities are better than bonds, there are a few actions you need to take.

- You can retire with less money, which might mean that you could retire sooner than you thought, or

- You can invest more money in riskier, but potentially higher returning, assets without risking your standard of living.

If you have digested the information and are convinced that annuities are better than bonds, there are a few actions you need to take.

RSS Feed

RSS Feed