For archived newsletters, please visit here.

|

Q. What resources are out there if no money for mortgage or rent payment?

A. Assistance is out there, here is what you need to do - Mortgage payment help Contact your loan servicer right away if you think you can't make payment. Fannie Mae and Freddie Mac have already said they are suspending foreclosures on mortgages they guarantee for 60 days. What exactly can you expect?

Rent payment help Fannie Mae and Freddie Mac will offer multifamily property owners loan deferrals if they promise not to evict tenants. Although various jurisdictions have temporarily halted evictions, you should call your landlord to explore your options. Keep in mind even if your landlord is able to get a forbearance for their mortgage, you will likely have to catch up on the missed rent payments later. For archived newsletters, please visit here.

7 Best salary information websites

1. Salary.com The most popular salary-specific job site, Salary.com lists every position in a field with free salary info. Their collection of data includes cost-of-living calculators, comparison tools, and lists of benefits, as well as negotiation tips. Salary.com doubles as a career site, providing job listings and advice for those on the lookout. Overall, this is probably the best site for salary info. 2. Glassdoor Glassdoor is known for its extensive company reviews and employee feedback. A salary search provides data for specific jobs at specific companies, rather than a general estimation. Employees share info on salaries, benefits, interview questions, and more—a great insider resource if you’re starting out at a new company. 3. PayScale A good resource for new grads, PayScale offers a free salary report based on experience, education, and other factors. Students should check out its College Salary Report for the lowdown on what various majors can expect to earn (and some negotiation tips). The career research section includes a Career Goal Tracker with salary data for the jobs you want. 4. Indeed The well-known job site aggregator has a salary search tool. Indeed lets you use keywords to search, in addition to job titles. Since Indeed users can access over 50 million job postings from unique sources, there’s a ton of salary data here. 5. SalaryList All the data on SalaryList comes from official reporting by companies or the United States Department of Labor, so you know you’re getting accurate information. The site provides salary data records for existing jobs by title, company, and state. 6. Salary Expert With data updated daily, Salary Expert offers not only free salary reports but cost of living analysis and career salary potential. You can also search for jobs by salary, if you’re thinking about switching fields. 7. Bureau of Labor Statistics The most recent Occupational Outlook handbook from the Bureau of Labor Statistics (available online or in print) provides salary data for thousands of jobs, searchable by field. It’s also a good idea to investigate any sites specific to your field or career for salary data. These sites may have more info on industry norms, particularly if your field’s a rarer one. What factors should you consider? Sites will often allow you to search based on job title, education and experience level, and location. But how does each factor affect the compensation you should ask for? 1. Job title Titles reflect responsibility and experience. While some companies allow you a little latitude in naming your job, others won’t be so flexible. Make sure you’re clear on the responsibilities of the title offered (or the title you want). 2. Career field Depending on the profit ratio of your industry, the same title can come with a different salary. Sales representatives, for instance, can work in multiple fields. But sales reps in high-demand fields, like pharmaceuticals, may be able to ask for more than those in other industries. 3. Location If you live in a location where housing, transit, food and other essentials cost more than the national average—like a large city, a coastal city, or a tourist destination—you should earn more. A Cost of Living Analysis (COLA) comparison, offered on many of the sites above, lets you know what to expect in your region. 4. Experience Work experience in your field can increase your value and your salary. Internships may count in your favor, depending on your responsibilities there. 5. Education Having a degree, period—an associate’s, a bachelor’s, or an advanced degree—should boost your salary expectations. Having a degree in your field is even better. 6. Where you went to college can sometimes make a difference, too. PayScale has a College ROI (Return on Investment) report that analyzes how degrees from different colleges can affect your salary. If you didn’t go to the Ivy League or a “top” school, don’t count yourself out! Education’s one of many factors that employers consider when setting compensation, and the more experience you get, the less it typically matters. 7. Special skills Whether it’s a software program, a type of design, or a foreign language, special skills can be lucrative in the job market. Try doing a keyword search for a unique skill, and see which employers are willing to pay more for it. The key is supply and demand. Workers in more in-demand fields, like nursing or computer science, tend to have more negotiating room. But, as you can see, there are plenty of factors that determine the “right” compensation for your job. And there are variables you can’t control. Racial and gender wage gaps, for instance, still persist. Industries in decline, or going through a temporary financial slump, may not have as much money to offer. Tips for the salary negotiation

The 3 websites below could help you find great values on airfares and hotels -

Scott's Cheap Flights It will send out international deals to subscribers for free Airfare Watch Dog It will send out daily emails with a long list of fares from airports you choose. The emails will flag sales, including from Southwest which is normally absent from daily newsletters. Secret Flying It provides instant alerts on flight deals that depart from cities across the U.S. to subscribers who download its app. For archived newsletters, please visit here.

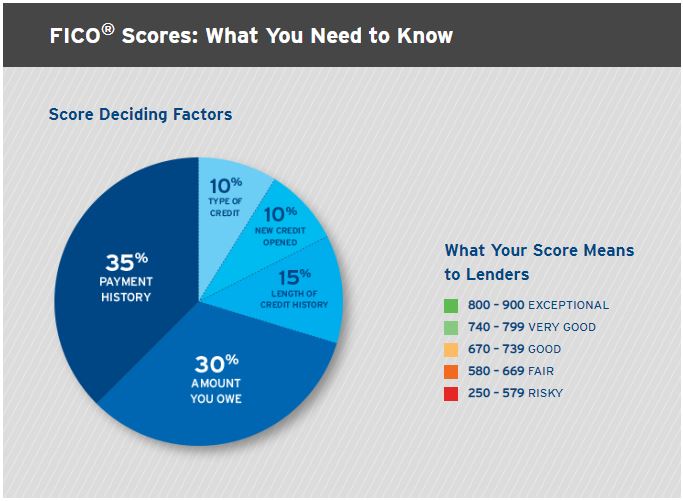

Q. What are the factors deciding my FICO score and what are their importance in deciding my FICO score? A. At the high level, there are 5 factors deciding your FICO score, and their importances are shown in the chart below -  For archived newsletters, please visit here.

For archived newsletters, please visit here.

JoinHoney.com

This browser extension automates your savings, it's best for online coupons and private alerts. When you check out at Amazon or any other 30,000 websites, you just click on Apply Coupons in a pop-up box, and HOney will input coupon codes for you. It can also alert you when a product's price drops and provide price histories on many items. Fakespot.com This browser extension is essential if you shop at amazon.com, walmart or any other e-retailers that offer products sold by third parties. It checks if a review is fake or real. It's best for you to decide what and where to buy! PriceBlink.com This browser extension checks prices at 11,000 stores. When you shop at Amazon.com and land at a product page, a yellow bar will pop up, click on Compare Prices and you will get a list of prices for that item at other stores. Rakuten.com Use this browser extension on your computer will earn you cash back when you making qualifying online purchases at more than 3,500 stores such as amazon.com. It sends out a check in the mail quarterly once you reach $5 in rewards. Credit scores could have big impact on many things, from better terms on credit cards and lower mortgage rates, to lower premiums on auto and homeowners insurance, and sometimes even the ability to get approved to lease an apartment (or to waive the upfront deposits).

However, here are 7 myths regarding what may (but actually doesn’t) help or hurt the credit scores - 1. Checking credit scores can hurt the credit score (a “hard inquiry” where a financial firm is evaluating a potential loan to you can have an impact, but a “soft inquiry” like an employer conducting a background check does not, nor does a soft inquiry of checking your own credit score); 2. Paying bills on time is all you need to worry about (it’s not, as “credit utilization” also matters, because paying on time but always being maxed out is a negative compared to ‘just’ using 30% of your available credit each month, which can be remedied by spending less or simply asking for a credit limit increase); 3. Carrying a balance helps boost the credit score (it doesn’t, it just racks up interest charges!); 4. Closing an old card with a high interest rate will help (it doesn’t, and closing a long-standing card can actually reduce the score by reducing the average age of your credit accounts); 5. Opening a new retail card at a 0% rate is good for your score (it’s not, it’s a hard inquiry that’s more likely to reduce the score); 6. Shopping for a mortgage/auto/student loan hurts the credit score (hard inquiries matter, but if multiple hard inquiries come together, they’re bundled together as a single query, and recognized as a single transaction that reflects the borrower is likely just shopping around); 7. Assuming credit reports are accurate in the first place (the FTC found in 2012 that 21% of consumers had errors, with 5% of the cases so serious it impaired their credit… which means it really is important to monitor your credit score to ensure credit events are being reported properly!). For archived newsletters, please visit here.

How do you like this service - a price-protection services combs your email inbox for order confirmations and shopping receipts from major retailers and for hotel reservations from selected booking sites, then searches for price drops and claims the refund for you?

If you like it, here are two websites would do it for you - Earny.co It works with more than 15 retailers as well as all Citibank credit cards and all Mastercards (for up to 4 claims per year). It will deduct 25% fee from each refund, or you can pay $9.99 for a monthly subscription. If you link credit card accounts that offer price protection, you can also get refunds on purchases from Amazon.com. Paribus.co It's a Capital One company, it will monitor your inbox for receipts from more than 25 major retailers, but it does not monitor your credit card accounts. For archived newsletters, please visit here.

For archived newsletters, please visit here.

Tired of typing long emails or text messages to clients, prospects, and team members? Want to show them how to do something that would take too much time to explain? Loom is a free Chrome extension that lets you record your screen, your camera, and microphone all at the same time. Don’t need all three at once? You can also choose to record just your screen or just your webcam, along with your microphone.

Loom puts all those elements together in a video for you. If you use your camera, your face will appear in the lower-left portion of the video, with the screen capture taking up most of the real estate. All videos are accessible by a URL. Instead of a long email, your client gets to see your face and hear your voice. Plus, they can always revisit the URL to refer back to your message if they need it. Loom lets you store your videos in folders, making them easy to find and re-use. You could record videos for new client onboarding, or explain the quoting process. You can show your team how you want them to do something, or show your developer the problem you’re having with your website. Video makes everything faster in all these use cases. As we write this, Loom has a rating of 4.8/5 stars, with over 9,400 reviews. There’s a desktop app in the works so you can record from your computer without opening a browser. If you are expecting your first child, congratulations! Here is a childbirth checklist prepared by AIG that might come handy for you. Money really can buy happiness, as it turns out — but you might not need as much as you think.

A large analysis published in the journal Nature Human Behavior used data from the Gallup World Poll, a survey of more than 1.7 million people from 164 countries, to put a price on optimal emotional well-being: between $60,000 and $75,000 a year. That aligns with past research on the topic, which found that people are happiest when they make about $75,000 a year. But while that may be the sweet spot for feeling positive emotions on a day-to-day basis, the researchers found that a higher figure — $95,000 — is ideal for “life evaluation,” which takes into account long-term goals, peer comparisons, and other macro-level metrics. The researchers, from Purdue University, also found that it may be possible to make too much money, as far as happiness is concerned. They observed declines in emotional well-being and life satisfaction after the $95,000 mark, perhaps because being wealthy — past the point required for daily comfort and purchasing power, at least — can lead to unhealthy social comparisons and unfulfilling material pursuits. Still, the findings don’t mean that getting a huge raise won’t lead to individual satisfaction: It simply suggests, according to the researchers, that a group of people making $200,000 a year is likely no happier than a group of people making $95,000. The well-documented “hedonic treadmill” phenomenon also suggests that people adjust relatively quickly to their newly flush bank accounts, with happiness leveling back off over time. In the new study, the researchers note that their estimates pertain specifically to individuals, and ideal household income is likely higher. Plus, while the figures in the paper represent global estimates, earning satisfaction also varies widely around the world, and in urban versus rural areas within countries. Certain regions — Western Europe, North America, Australia, New Zealand, East Asia, and the Middle East — had higher financial thresholds for both emotional well-being and life evaluation, while areas including Eastern Europe, Southeast Asia, Latin America, and Sub-Saharan Africa were lower than the global numbers. All told, the ideal income for life evaluation ranged from $35,000 in Latin America to $125,000 in Australia and New Zealand. In North America, the optimal amount for life evaluation was estimated at $105,000, and the range for emotional well-being was slated at $65,000 to $95,000. The researchers didn’t observe significant differences between men and women, but they did find that education level influenced monetary ideals. Highly educated people tended to have loftier income satisfaction points, likely because they had higher expectations of wealth and were more susceptible to social comparison. All said if your income is below — or above — the researchers’ ideal threshold, don’t despair. Research suggests that while money can buy happiness, the quality of your spending is just as important as the quantity. For archived newsletters, please visit here.

Have you thought about what is really fulfilling and “enough” to make you happy?

Wealthy, Successful, and Miserable is a New York Times article that looks at how more and more research shows what really makes us happy in our jobs, yet in practice people are less and less happy at work. Jack Bogle told the anecdote in his book Enough: “At a party given by a billionaire on Shelter Island, Kurt Vonnegut informs his pal, Joseph Heller, that their host, a hedge fund manager, had made more money in a single day than Heller had earned from his wildly popular novel Catch-22 over its whole history. Heller responds,’Yes, but I have something he will never have . . . enough.'” Q. What is "widow's penalty" tax trap and how to avoid it?

A. Widow's penalty tax trap refers to the situation that after a spouse’s death, the survivor will eventually go from a joint return to being a single filer. The widow or widower’s tax bracket likely will rise, resulting in a plumper tax bill.This bracket creep occurs because the survivor’s taxable income may be about the same as it was on a joint return. (The reduction in taxable income from the loss of one Social Security check may will be partially or fully offset by a smaller standard deduction.) For example, someone could go from a 24% tax bracket, filing jointly, to a 32% bracket for the survivor. The result will be thousands of dollars a year in extra tax payments. As a single filer, the surviving spouse also could owe more tax on Social Security benefits or face more exposure to the 3.8% surtax on net investment income. How to Avoid Widow's Penalty? First, it is important to address the widow’s penalty while both members of the couple are alive. After age 59-1/2, but before begin taking Social Security benefits, couples could convert part of their traditional IRAs to Roth IRAs at a lower tax rate. The 10% early distribution penalty won’t apply then and the conversion would be taxed at the lower joint filing rate. Moreover, Roth IRA conversions reduce taxable RMDs from traditional IRAs after age 70-1/2. Today’s tax rates for married couples filing jointly are relatively low, no higher than 24% on taxable income (after deductions) up to $321,450. That same income would put a single filer in the 35% bracket. A series of partial conversions should be done over a period of years, taking care to keep the amounts within low tax brackets. For the money moved to the Roth IRA, there are no RMDs for the owner or the surviving spouse, therefore, the account can continue to grow or be used with no tax consequences. Drawing down a reverse mortgage line of credit or taking life insurance policy loans could be other sources of cash flow that won’t trigger highly taxed income. For archived newsletters, please visit here.

For archived newsletters, please visit here.

For archived newsletters, please visit here.

Bank and Brokerage Accounts

Once you haven't touched your account for 3 to 5 years, banks usually transfer your money to the state of your last known address. Visit unclaimed.org and follow links to the website of each state where you have lived. You can also recover money in a deceased relative's account if you have proper documentation. Life Insurance Policies If it is not listed on unclaimed.org, use the Life Insurance Policy Locator at naic.org, a service run by state insurance regulators. Retirement and Pension Accounts Visit freeERISA.com to find your old employer's latest form 5500, which has contact information for the administrator. If your 401(k) was terminated, check askebsa.dol.gov/abandonedplansearch for contact information. If your pension plan failed or was shut down, you may still qualify for a payment from the Pension Benefit Guaranty Corp, look for your plan at pbgc.gov/search-unclaimed-pensions. If all this is fruitless, the nonprofit Pension Rights Center (pensionrights.org) may be able to help. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed