The following chart shows various national median rates for care settings based on 2020 survey.

|

|

|

The following chart shows various national median rates for care settings based on 2020 survey.

0 Comments

Below is a brochure from American National for its CENTURY PLUS ANNUITY for NY. This annuity product offers 4 major benefits:

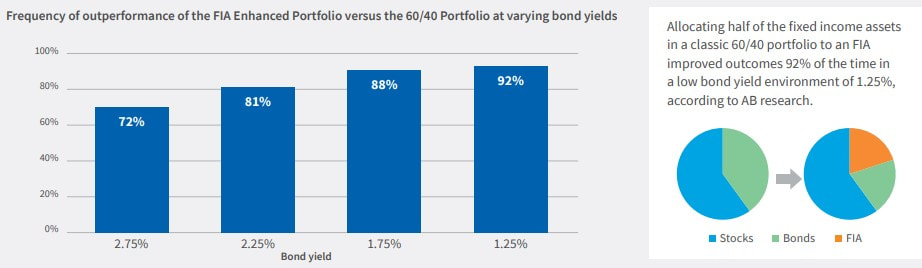

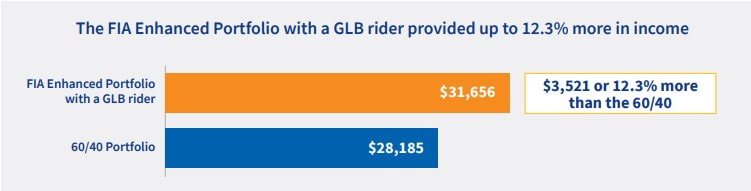

Are you using fixed income assets like CDs and bonds for yield, safety, or both? With 5-year CD rates at only 0.28% and bond yields at 1.95%1 , retirees relying on these assets to cover their expenses may not have enough income to meet their needs. Adding a fixed index annuity (FIA) can help protect against market downturns, while enhancing the performance potential of your clients’ portfolios, according to recent research by leading asset manager AllianceBernstein (AB). AB research showed that portfolio outcomes improved up to 92% of the time with a fixed index annuity  Adding a lifetime income benefit improved outcomes 99% of the time AB also found that when it came to providing retirement income, adding an FIA with a guaranteed living benefit (GLB) rider enhanced results 99% of the time over a 60/40 portfolio. In the best-performing scenarios, the FIA Enhanced Portfolio with a GLB rider provided almost $3,500 more in annual retirement income, an increase of more than 12% over the 60/40 Portfolio.  Whether you are getting started with the planning process, or need to review your existing plans, your legacy requires careful planning and the appropriate legal documents to ensure that your assets and belongings transfer to your loved ones as you wish.

A well-designed legacy plan can help you: ■ Arrange for the guardianship of your minor children ■ Preserve wealth and promote your values throughout generations ■ Protect assets from creditors, divorces and lawsuits ■ Minimize family discord ■ Provide for orderly family business succession ■ Promote a charitable cause ■ Provide for loved ones who have special needs while preserving eligibility for government assistance ■ Avoid probate and probate fees ■ Minimize or eliminate estate taxes at death Taxes and Transfer Costs Whether you do bare bones planning by drafting a will or fail to plan altogether, you have an estate that is subject to probate administration. Your estate must be administered through the probate court located in the county of your legal residence at the time of death. The overall cost of probate will vary according to state law and will generally hinge on the size of the estate—the more you own, the more you owe. In addition, generally the federal government imposes an estate tax on all property you pass to your loved ones upon your passing. Every asset you own at that time will be included in determining the value of your estate and any taxes due. Any amount that is above the applicable estate tax exemption in the year you pass away will be subject to federal estate taxes. In 2015, the estate tax exemption is $5.43 million. Some states impose their own separate estate tax. For example, in New Jersey, the estate tax exemption is $675,000. It is possible that an estate that is too small to generate federal estate taxes may nonetheless trigger state estate taxes. Some states impose an inheritance tax in addition to the state estate tax. Inheritance tax is imposed on the right to receive property by inheritance or legal succession. The tax imposed is based on the beneficiary’s relationship to you and the amount of property received from your estate CONTROL OVER THE RECOGNITION AND TAXATION OF IRREVOCABLE TRUST EARNINGS

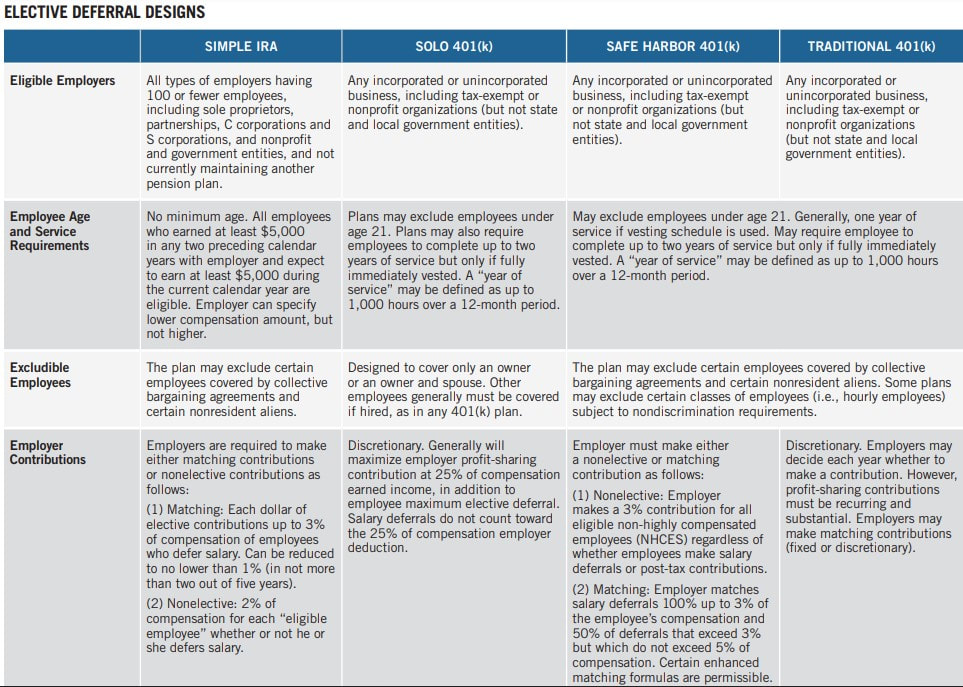

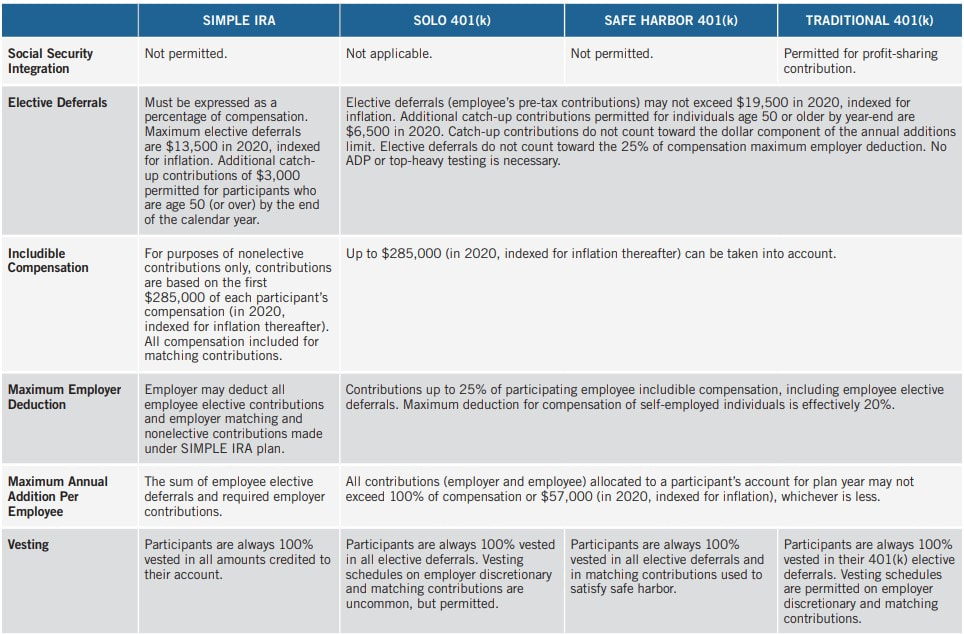

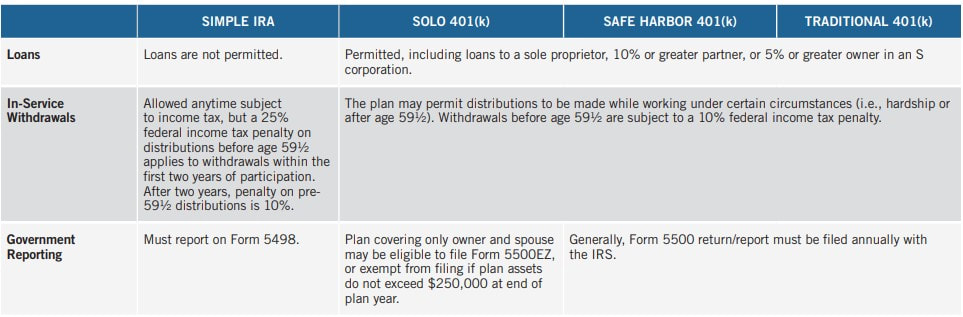

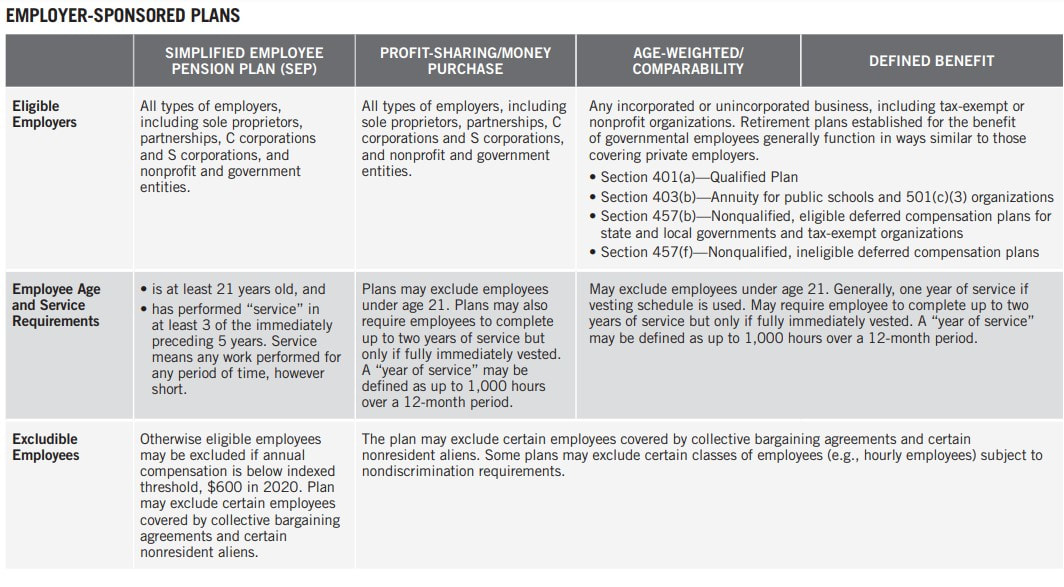

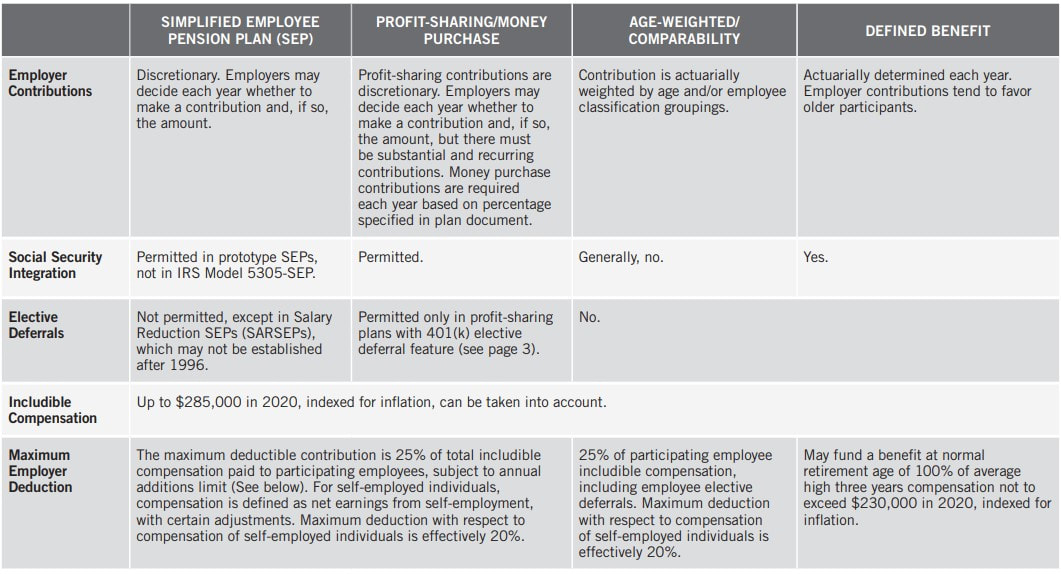

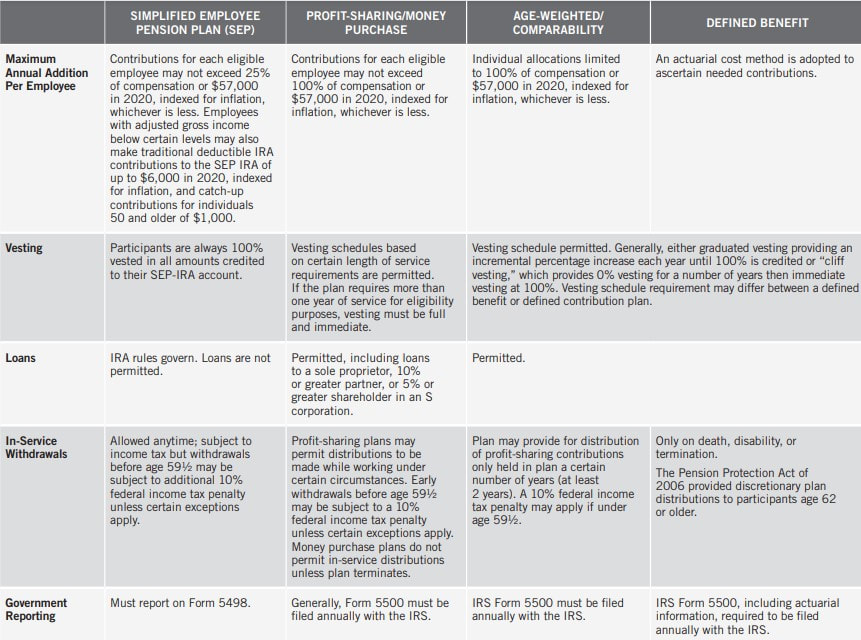

Investing trust assets in an annuity can provide income tax efficiency within the trust and help meet the needs of trust beneficiaries. Taxable income retained by certain non-grantor trusts is subject to comparatively higher effective trust income tax rates and may be subject to an additional 3.8% net investment income tax. Although income may be distributed to trust beneficiaries to help reduce the impact of the trust tax rates, payment of income to the trust beneficiaries may not be desirable. Investment in an annuity by a trust meeting certain requirements may avoid this tax dilemma. Keep in mind that the manner in which the annuity is titled will have an impact on how the annuity contract operates. The titling options and rules are described throughout the remainder of this brochure. ANNUITIES AND TRUSTS: IRC SECTION 72(u) Annuities that are owned by trusts that act solely for the benefit of living individuals will receive tax deferral under IRC Section 72(u). With annuities that meet the requirements under IRC Section 72(u), the appreciation of the annuity remains tax-deferred until the trustee requests a distribution. Annuities owned by trusts that benefit nonnatural entities, businesses, or charities will not receive tax deferral. FLEXIBLE INVESTMENT OPTIONS WITH GROWTH POTENTIAL Changing trust objectives and economic conditions may cause the trust to change or modify its investment allocations. In many cases, the reallocation of trust assets may result in transaction costs and/or the realization of capital gains. DEATH BENEFITS WITH POTENTIAL TO ENHANCE THE VALUE OF ASSETS PASSING TO TRUST BENEFICIARIES An annuity with a guaranteed death benefit or enhanced death benefit offers the potential for long-term growth with downside protection, allowing the trustee to consider a more aggressive asset allocation for the benefit of the remainder beneficiaries. If the account performs poorly, an enhanced death benefit may provide an amount higher than the original account value at the death of the annuitant. GUARANTEED LIFETIME INCOME An annuity can satisfy a need for trust income through a guaranteed lifetime income stream for the income beneficiary of a trust. This can be beneficial for two reasons: 1. It allows the trustee to allocate a specific amount of trust assets to generate a lifetime stream of income. 2. It enables the trustee to invest more aggressively without fear of compromising income needed for the beneficiary’s life, thereby potentially growing the trust assets for the benefit of the remainder beneficiaries. In last blogpost, we discussed employer-sponsored plans for business owners. Now we will discuss Elective Deferral Designs.       In next blogpost, we will compare ELECTIVE DEFERRAL DESIGNS.

In last blogpost, we discussed Conduit trust. Now we will discuss Accumulation trust.

With an accumulation trust, the trustee has broad discretionary authority to either pay out or accumulate retirement plan distributions during the lifetime of the primary beneficiary for possible distribution to another beneficiary, at a later date. However, after SECURE, even an accumulation trust isn’t the perfect solution. It has its tradeoffs. An accumulation trust may resolve someone's concerns about the beneficiary receiving too much too quickly, but at a prohibitively expensive income tax hit. SECURE requires that all retirement benefits be paid to the accumulation trust within 10 years, following the year of the death. To the extent the trustee accumulates retirement plan benefits in the trust, they will be taxed at the highest trust rates due to its compressed tax brackets. Yet, a strategy that combines an accumulation trust with the purchase of a life insurance policy may be the right solution to help offset the accelerated tax liability with an income-tax free death benefit at the death. Aimed at increasing access to tax-advantaged accounts and preventing older Americans from outliving their assets, the Setting Every Community Up for Retirement Enhancement Act (SECURE Act) is far-reaching retirement savings legislation that took effect in January. One significant provision eliminated stretch IRAs as an estate planning tool by requiring full distribution of an IRA to beneficiaries within 10 years, following the year of the employee or IRA owner’s death. Now is the time to identify new options to pass legacy to beneficiaries without also passing a big tax bill.

Conduit trust The new legislation may be most problematic for people with conduit trusts because the conduit trust will no longer operate the way originally expected it to work. Under a conduit trust, the trustee immediately pays all retirement plan distributions to the primary or lifetime trust beneficiary (“conduit” beneficiary). All retirement plan distributions paid to the trust are forced out to the conduit beneficiary and nothing accumulates in the trust. Historically, conduit trusts regulated and controlled the systematic and gradual payout of someone's sizeable retirement plan over the beneficiary’s lifetime. They were used to address the fears regarding the beneficiary’s potentially questionable financial judgment, discipline and restraint as well as concerns about creditors’ and other claimants’ (ex-spouses) attempts to access those assets, if otherwise, left outright the beneficiary. SECURE mandates the trustee accelerate distributions under the 10-year payout rule to the conduit beneficiary rather than make small incremental distributions over the beneficiary’s lifetime unless the beneficiary is an “eligible designated beneficiary” (EDB). An EDB is a surviving spouse, a disabled or chronically ill individual, minor child of client, or an individual who is not more than 10 years younger than the client. As a result, SECURE may expose a conduit beneficiary to an increased income tax burden and undermine the intent, purpose and utility of the trust if the designated beneficiary is not an EDB. At a minimum, people should have their conduit trusts reviewed and either modified to name an EDB, if appropriate for their circumstances, or potentially switch to an accumulation trust. In next blogpost, we will discuss Accumulation trust. One of the major fears your clients face is outliving their income. A Palladium® Single Premium Immediate Annuity (SPIA) could help you shield you from this risk . SPIA allows a lump sum to be converted into a steady stream of guaranteed annuity payments, providing a guaranteed income for as long as it's needed. Attached here is a case study from AIG on the new Lifetime Income Choice’s Max Income Option. Max Income Option Provides:

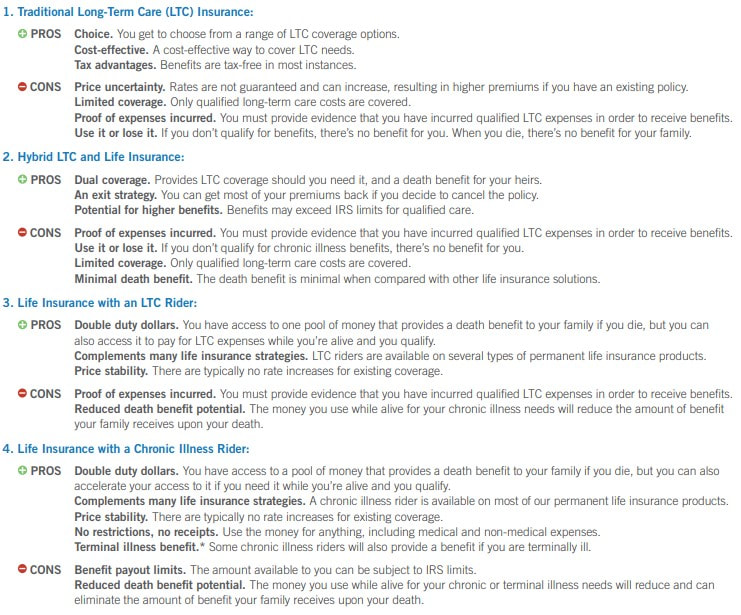

In last blogpost ,we showed 4 insurance options to protect against chronic illnesses.  Being chronically ill means you’re unable to perform at least two of the Activities of Daily Living (eating, bathing, etc.) for at least 90 days; or you suffer from a severe cognitive impairment. Here’s a quick snapshot of four common insurance options that people may consider for financial protection in the event of a chronic illness.  In next blogpost, we will compare the pros and cons of each option. The following AIG flyer shows a scenario where one could use a combination of Term and GUL to protect from both pre- and post-retirement risks! Although having a retirement savings number is important, it’s also a moving target and fixating on one number runs the risk that you won’t adjust your savings goals to new circumstances, such as higher health care costs, inflation or the vagaries of the economy. Life isn’t stationary and your retirement plan, including any target savings number, shouldn’t be either.

Instead of focusing exclusively on the size of your nest egg, create a comprehensive retirement plan that you’ll refine and change over time. It should include your financial goals, a net worth statement, a working budget, debt management strategy, emergency funds and any insurance. Any retirement plan also should reflect your expected retirement lifestyle, investing horizon, risk tolerance, savings goals and estate planning. You’ll want to consider how your retirement savings would hold up under different scenarios, simulating extreme market conditions or unexpected life events, to be sure your bases are covered. A financial professional can help you do it or use Microsoft’s free online Retirement Financial Planner template. Revisit the plan every few years while you’re accumulating assets and whenever you have a life change, such as switching jobs, losing a family member or moving. As retirement nears, the plan should factor in your required minimum distributions to minimize your tax burden. You want an appropriate mix of taxable and nontaxable investments, such as a Roth IRA combined with a taxable brokerage account, as well as a balance of stocks, bonds, real estate and other assets. Many retirement spending models use the 4% rule in which retirees withdraw 4% from their retirement portfolio in the first year of retirement. Each year thereafter, they adjust the dollar amount of their withdrawals by the previous year’s rate of inflation. The rule is designed to prevent retirees from running out of money during a 30-year-retirement. Your current spending also may be nothing like your retirement expenses because when we have more leisure, we often spend more. In retirement, health care costs escalate dramatically. Working households spend about 6% of their annual budget on health expenses, versus 14% for retirees, according to the Kaiser Family Foundation. You need to allow for flexibility because your life is going to change over time. Although you may be perfectly healthy now, things could happen, and there could be additional costs associated with your care. Thinkadvisor.com has an article that introduces the new state birthday rules, and calling it one of the least known opportunities for seniors.

Medigap Basics The Medicare Part A hospitalization program pays hospital bills, and the Medicare Part B program pays outpatient and physician services bills. Medigap policies can help consumers pay their Medicare Part A deductible and meet the traditional Medicare copayment and coinsurance requirements. Consumers can also buy Medicare Advantage plans. Those policies tend to offer enrollees broader coverage than the traditional Medicare program, in exchange for giving the enrollees financial incentives to use in-network providers and requiring the enrollees to get preauthorization for some medical procedures. Many producers strongly prefer selling consumers Medigap policies, because they see both the rules for producers and the coverage rules for the patients as being more flexible. For producers, one obstacle to selling Medigap policies has been higher monthly premium costs for Medigap coverage. Another obstacles has been the difficulties unhappy Medigap users have with switching policies. Medigap Enrollment Period Rules Health insurers, and some voluntary public health benefits programs, use “open enrollment period” systems, or limits on when people can buy coverage without going through much, or any, medical underwriting, to encourage healthy people to pay premiums even when they feel fine. The idea is to keep healthy people in the risk pool, by raising the possibility that they could break legs or suffer heart attacks, and have no way to get health coverage, outside the open enrollment period. Federal law creates a one-time, six-month Medigap policy open enrollment period period after a consumer’s 65th birthday. After that, Medigap users must show they qualify for a special enrollment period to switch Medigap policies. Users can get special enrollment periods easily when they move to new markets. Otherwise, they may have to show that their Medigap plan issuer has broken federal government rules or shut down. Idaho, Illinois and Nevada The new Idaho birthday rule is set to take effect March 1 2022. It will create a 63-day plan switching period beginning on the policyholder’s birthday. The new policy must offer the same level of benefits as the existing coverage or a lower level of benefits. The Medigap policy user can either switch insurers or change to a new Medigap policy from the same issuer. Idaho will switch to a community rating system for Medigap enrollees, meaning that premium rates will no longer be based on the age of the applicant. In Illinois, a new birthday rule will take effect Jan. 1, 2022. The Illinois rule will let Medigap users ages 65 through 75 have annual Medigap open enrollment periods lasting 45 days after their birthday anniversaries. The new policy must offer the same level of benefits as the existing coverage or a lower level of benefits. In Nevada, a new birthday rule will take effect Jan. 1, 2022, and provide 60-day plan switching periods starting on the first day of a Medigap user’s birthday month. Eligible consumers can buy new coverage, with the same or lesser benefits, from either their existing carriers or new carriers, without medical underwriting. A consumer cannot use the new rules to get policies with extra, innovative benefits, such as dental insurance, vision insurance, hearing benefits or gym memberships, officials say. Why the Quirks? One reason the new birthday rules are complicated is that insurers and government officials have been trying to give consumers ways to switch coverage without increasing the odds that some especially generous or well-run Medigap issuers will attract large numbers of new enrollees with very high health care costs. Another reason is that Congress created the Medigap program before the Medicare Advantage plan, and it left much more responsibility for regulating Medigap policies in the hands of the states. States have more ability to tailor Medigap rules to suit local needs, but that means producers who do business in two or more states may have to use different strategies for clients in different locations. Financial-planning.com has an article analyzes if Roth IRA conversion is still a risk worth taking this year, see below -

Go all out on contributions to retirement plans Didn’t max out your contribution limits last year? The IRS allows contributions for 2021 to be made through April 15, 2022. That’s three days before this year’s April 18 filing deadline, which was extended due to the Emancipation Day holiday in Washington, D.C. Some contributions are deductible, so they’ll lower the total amount of income on which taxes fall, a savings to the taxpayer. For 2021 returns being filed now, Americans could contribute a maximum $6,000, plus an extra $1,000 if aged 50 or older, to a traditional individual retirement plan (IRA) or Roth IRA. So an older married couple can put in a maximum $14,000. Traditional IRAs are generally funded with money on which taxes haven’t yet been paid, while Roth plans are fueled by after-tax dollars. Pretax contributions grow tax-deferred, with the owner paying ordinary rates on future withdrawals. While investors can also contribute money on which they’ve already paid taxes, they pay ordinary tax on withdrawals, making after-tax contributions to a traditional IRA a double tax hit. In contrast, Roth plans grow tax-free, with no levies on withdrawals. Deductions get complicated, depending on how much a taxpayer makes and whether she or a spouse has a workplace retirement plan. A traditional IRA owner who doesn’t have a workplace retirement plan (or whose spouse lacks one) or whose income is below $76,000 gets a whole or partial deduction. If a married couple filing jointly has one spouse with an employer-sponsored retirement plan, typically a 401(k), then an IRA contribution by the other spouse is no longer deductible once their joint income hits $214,000. Straightforward Roth IRA plans are a little different. The contribution limits are the same. But while there are no income limits on who can contribute to a traditional IRA, contributions to Roth plans now are limited to people who made under $140,000 last year (under $208,000 for couples). Because their assets grow tax-free and don’t bear future taxes, Roth contributions aren’t deductible. The Roth conundrum It’s still not clear what might happen to so-called backdoor Roth conversions, a mainstay of large retirement accounts and estate planning for the wealthy, under stalled legislation in Congress. While emerging versions of the Build Back Better tax-and-spending bill aim to limit or ban the ability of high earners to own Roths through indirect methods, the legislation is mired in infighting by Democrats. But some tax and retirement experts think that it’s probably safe to take advantage of their current tax benefits, even as legislators work to curb them. January 31, 2022 8:36 PMBackdoor conversions involve an investor converting a traditional IRA into a Roth. They’re a way for wealthy people to sidestep the income limits for direct contributions to a Roth. An early version of the House bill banned conversions of after-tax dollars in IRAs and 401(k)s. The House passed a somewhat softened version of that proposal last November. The legislation, which has to be passed by the Senate, would outlaw so-called mega-backdoor Roth conversions starting Jan. 1, 2022. The strategy came under a spotlight when ProPublica showed how PayPal co-founder Peter Thiel used it to transmute less than $2,000 worth of pre-IPO shares into a $5 billion account. The bill would still allow regular Roth conversions but would ban people with higher incomes from doing them starting in 2032. Last December, the Senate offered its own version of Build Back Better that proposes those same limitations. The backdoor strategy involves using hefty after-tax contributions to a 401(k) plan that permits them. Under IRS rules, a taxpayer could put as much as $58,000 last year into a workplace retirement plan ($64,500 for those 50 or older). One chunk of the money reflects the maximum pre-tax amount of $19,500 ($26,000 if 50 or older), while the remainder, up to $38,500, reflects after-tax dollars. The limits include any company matches. The taxpayer then converts her 401(k) to a tax-free Roth. The higher amounts can swell a retirement portfolio far beyond what direct contributions to an ordinary Roth can. Christine Benz, Morningstar’s director of personal finance, wrote in a Jan. 21 research note that it’s “unlikely” that when a final bill makes it to President Joe Biden’s desk for signature, if indeed one does, the proposed curbs would be retroactive to the start of this year. “Given that these contributions and conversions are currently allowable,” she wrote, financial advisors have “been urging their clients to go ahead with them until the law officially changes." Benz quoted Aron Szapiro, the head of retirement studies and public policy for Morningstar, as saying that the likelihood of a retroactive ban on after-tax contributions is "close to zero.” Of course, nothing’s final on Capitol Hill until it’s final. Nonetheless, Benz wrote, “given that backdoor Roths are one of the few mechanisms that higher-income heavy savers can use to achieve tax-free withdrawals and avoid RMDs in retirement, many such savers are apt to conclude that it’s a risk worth taking." Thinkadvisor.com recently had an article that highlights the flaws of target date funds, it's worth a reading if you have or plan to invest in target date funds.

Highlights of the article include:

Just 8 quick questions can help check your retirement readiness. Size up your situation with the Integrity Life Quick Check one-pager to prep for new year planning. When reviewing different Medicare options, some retirees might first look at the cost of premiums when selecting from the available plan options. However, because not all Medicare plans are created equal (and because retirees will have varying needs for medical care), choosing a plan with a lower premium could end up costing a retiree more in the long run.

One of the major decisions when enrolling in Medicare is whether to choose traditional fee-for-service Medicare or Medicare Advantage. Medicare Advantage plans can be attractive for some retirees because they often have lower premiums than the alternative of using traditional Medicare with Medigap and Part D prescription plans, and can come with additional benefits, such as prescription, dental, and vision benefits. Nonetheless, these plans can have high maximum out-of-pocket limits that could be reached if the insured has significant medical needs. Further, Medicare Advantage plans steer retirees to ‘in-network’ providers, meaning that a policyholder could end up paying significantly more for care if they are seen by an ‘out-of-network’ provider. Similarly, retirees choosing among Medigap policies might be tempted to choose the plan with the cheapest higher-deductible premium (which could result in significant out-of-pocket expenses if the retiree ends up needing expensive medical care), or at the opposite end, the plan with the most comprehensive coverage (which might lead the retiree to pay more in premiums when they could afford the deductibles and coinsurance of a plan with cheaper premiums). In the end, there is no ‘one-size-fits-all’ approach to selecting Medicare plans Navigating Medicare enrollment can be a tricky task for retirees, a Medicare specialist can help choose a particular plan that fits the retiree's situation the best.

First, the agent-vetting process can occur as the retiree is approaching Medicare eligibility age (typically 65), and a good agent should be familiar with the pros and cons of starting Medicare at the age of eligibility if the retiree has other options (e.g., a workplace retirement plan). Also, a good agent will also guide the retiree through the process of applying for Medicare Parts A and B, even though they will not earn a commission for doing so (as Medicare specialists are typically only compensated for Medigap supplemental policies, Medicare Part D prescription drug plans, and Medicare Advantage plans). Next, agents should be able to explain how the retiree’s Medicare premiums will be impacted by the Income-Related Monthly Adjustment Amount (IRMAA) based on the income. Finally, the agent can then help the retiree choose among Medigap, Medicare Part D, and Medicare Advantage plans for their specific state. For example, if the retiree is considering a Medicare Advantage plan, having an agent that is familiar with the insurance carriers and hospital networks in the retiree's state can help choose a plan that includes the best medical providers for the individual situation. Q. I am moving to another state where my Part D drug plan is not available. Can I get another plan?

A. If you have Original Medicare, you can get a new Part D plan without penalty if you do it in a timely way. If you get your medication coverage from a Medicare Advantage (MA) plan, it's a bit more complicated. You will likely need to switch to a new plan for all your coverage, as plans often do not cross state lines. The timetable is the same for original Medicare or an MA plan: your special enrollment period starts a month before your move and lasts until two months after the month you move. Q. If I am enrolled in Medicare, but I am still working, can I still contribute to my HSA?

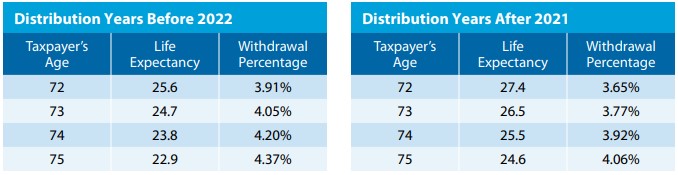

A. No, you can no longer contribute to your HSA because you can only contribute tax-free dollars to an HSA if you have a high-deductible plan and no other health coverage. If you enroll in Medicare, you can still use HSA money to pay for out of pocket costs, but you cannot continue to make contributions to it. Note, you can still contribute to FSA, but you do have to use the FSA dollars in the same or following year. RMD Factors Revised for 2022 IRS regulations have updated the life expectancy tables used in calculating required minimum distributions (RMDs). The new tables are effective for distribution years beginning on or after January 1, 2022. They replace old tables that were last updated in 2002. Need to Know: Taxpayers turning 72 in 2021 and having a required beginning date of April 1, 2022, cannot use the new tables to calculate their RMD for 2021 (even though they have until April 1, 2022 to take that first distribution). The Effect: RMDs Reduced The new tables contain updated distribution periods that reflect increased life expectancies since the last tables were issued. The differences in the tables are not huge. However, use of the new tables will result in smaller RMDs. The below compares a small portion of the Uniform Lifetime Table. The new tables are easy to use for lifetime RMDs. Taxpayers simply use the new table to calculate their RMDs for their 2022 distribution year. For Example: IRA Owner, Age 75 Patty turns 75 in 2022. Her one IRA had a value of $550,000 as of 12/31/21. She must distribute a minimum of $22,357.72 ($550,000/24.6) before 12/31/22. This is $1,659.75 less than the $24,017.47 that would have been required under the old table ($550,000/22.9).  In last blogpost, we discussed what is a Roth 401K. Now we will discuss Roth 401K's Pros and Cons.

The Pros Potentially tax-free growth It can be complicated to quantify the value of potentially tax-free growth versus a current tax deferral. You don't know what your income will be in the future, nor what your tax rate will be. If you expect your marginal rate to be at least as high after retirement as it is currently—which would apply to many younger participants who anticipate growing incomes over time—the Roth option could work in your favor over the long term. This also sometimes applies to those who plan to move after retirement from a low-tax state to a high-tax state, say Texas to California. It could also work out that the dollar amount difference in the taxes you'd pay by the time you get to retirement is very small, meaning the income tax you would pay per year on Roth 401(k) contributions could be roughly equal to what you'd pay eventually on distributions after 59½. Your age and your level of income will influence the bottom line. Help with RMD concerns Required minimum distributions (RMDs) apply to Roth 401(k)s in the same way they do to tax-deferred 401(k)s, meaning you'd have to start taking out a specified amount once you turn 72 if you are no longer working. However, once you are retired, you can roll over your plan into a Roth IRA, and then it would no longer be subject to the RMD rules (at least during the lifetime of the original owner), and you could withdraw the money on your own timetable. Access to tax-free growth at higher income limits High earners start getting restricted from making full Roth IRA contributions above $125,000 in modified adjusted gross income in 2021 for individuals and $198,000 for married couples filing jointly, and this will be $129,000 for individuals and $204,000 for couples in 2022. But Roth 401(k) plans follow 401(k) plan rules on this issue, which means there are no income restrictions. You can also make higher contributions in a Roth 401(k) than a Roth IRA. An individual can put $6,000 into a Roth IRA per year, or $7,000 if over 50 in 2021 and 2022. In contrast, you can put $19,500 into a Roth 401(k) for 2021 and $20,500 for 2022, plus $6,500 catch-up if you're over 50 in both years. Or you can mix and match percentages and make some pre-tax contributions and some post-tax contributions. You can adjust throughout the year according to your needs and your plan specifications. The cons No tax deferral now The list of cons may be short for Roth 401(k)s, but missing tax deferral is a big one. When faced with a choice of paying more tax now or later, most people choose to pay later, hence the low participation rates for Roth 401(k)s. Encouraging people to save for retirement is important, and tax deferral has always been a key driver of savings. The financial justification for this has been that historically, people typically had lower tax rates in retirement than during their working years, and the math generally worked in their favor to have a lower adjusted gross income now and take taxable distributions in retirement. There are a host of other reasons why a taxpayer might benefit from a lower adjusted gross income today, such as the calculation of child tax credits, financial aid for college, or divorce settlements. Then there is the impact on take-home pay. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed