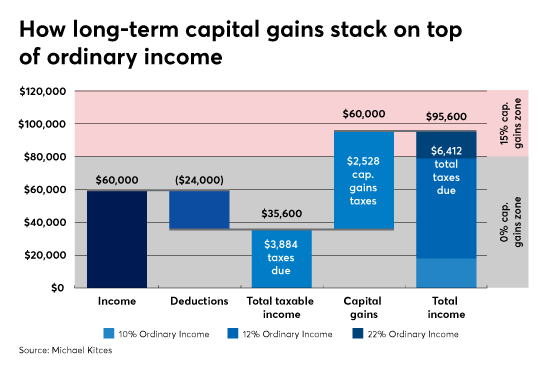

An Example: how long term capital gain stack on top of ordinary income

A married couple has $60,000 of ordinary income, on top of which they are taking a $60,000 capital gain as well. In 2019 they will be eligible for a $24,400 standard deduction.

Under the ordering rules for ordinary income and capital gains, the $24,400 standard deduction will be applied first against the $60,000 of ordinary income, on top of which the $60,000 long-term capital gain will be stacked. This results in $35,600 of ordinary income that falls within a combination of the 10% and 12% tax brackets, for a total ordinary income tax liability of $3,884, while the remaining $60,000 long-term capital falls across the 0% and 15% long-term capital gains tax brackets — with the first $43,150 falling in the 0% bracket up to the threshold, and the remaining $16,850 taxed at 15%, for a total capital gains tax liability of $2,528.

A married couple has $60,000 of ordinary income, on top of which they are taking a $60,000 capital gain as well. In 2019 they will be eligible for a $24,400 standard deduction.

Under the ordering rules for ordinary income and capital gains, the $24,400 standard deduction will be applied first against the $60,000 of ordinary income, on top of which the $60,000 long-term capital gain will be stacked. This results in $35,600 of ordinary income that falls within a combination of the 10% and 12% tax brackets, for a total ordinary income tax liability of $3,884, while the remaining $60,000 long-term capital falls across the 0% and 15% long-term capital gains tax brackets — with the first $43,150 falling in the 0% bracket up to the threshold, and the remaining $16,850 taxed at 15%, for a total capital gains tax liability of $2,528.

RSS Feed

RSS Feed