This is a case study, we have two couples, each couple puts away the same amount for retirement, but they allocate assets differently among the tools. Some contributions were made to qualified plans.

Couple 1: Stuck in their tax bracket

The first couple chooses to protect their family’s dreams, aspirations and accumulated wealth with term life insurance until it runs out. They focus solely on capital assets and retirement income assets to fund their retirement.

Desired income: $100,000

Required income: $78,950; required income includes income clients are obligated to receive due to automatic payments, like pensions, or tax law (e.g., Required Minimum Distributions – RMDs, starting at age 70½)

Retirement income gap: $21,050; which will be filled using their capital asset or retirement income toolbox

Net worth: Includes only capital assets (e.g., investments and real estate) and retirement income assets, or qualified assets

Achieving desired income: The taxpayers stuck in their tax bracket decide to take dollars out of their retirement income toolbox to cover their income gap.

Desired income of $100,000 Source of income

Required income $78,950 Social Security and RMDs

Income gap $21,050 Filled with only retirement income assets (taxed at ordinary income rates)

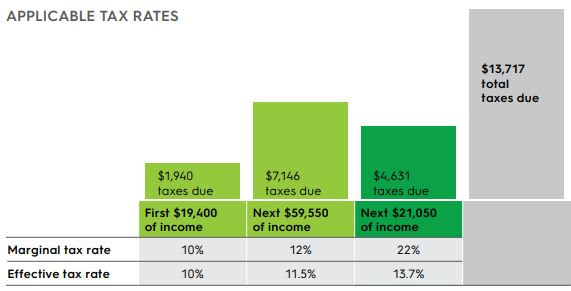

Taxes for “stuck” married couple: This couple will pay taxes on the first two tax brackets and some ($21,050) in the 22 percent brackets. Their total taxes due will be $13,717 and effective tax rate is 13.7 percent.

Couple 1: Stuck in their tax bracket

The first couple chooses to protect their family’s dreams, aspirations and accumulated wealth with term life insurance until it runs out. They focus solely on capital assets and retirement income assets to fund their retirement.

Desired income: $100,000

Required income: $78,950; required income includes income clients are obligated to receive due to automatic payments, like pensions, or tax law (e.g., Required Minimum Distributions – RMDs, starting at age 70½)

Retirement income gap: $21,050; which will be filled using their capital asset or retirement income toolbox

Net worth: Includes only capital assets (e.g., investments and real estate) and retirement income assets, or qualified assets

Achieving desired income: The taxpayers stuck in their tax bracket decide to take dollars out of their retirement income toolbox to cover their income gap.

Desired income of $100,000 Source of income

Required income $78,950 Social Security and RMDs

Income gap $21,050 Filled with only retirement income assets (taxed at ordinary income rates)

Taxes for “stuck” married couple: This couple will pay taxes on the first two tax brackets and some ($21,050) in the 22 percent brackets. Their total taxes due will be $13,717 and effective tax rate is 13.7 percent.

In our next blogpost, we will look at the second couple that uses permanent life insurance smartly.

RSS Feed

RSS Feed