In our last blogpost, we showed the first couple how they use term life and stuck in their current tax bracket.

Couple 2: Has tax-sensitive distribution strategy

The second married couple has the ability to design a tax-sensitive distribution strategy because they are using permanent life insurance to protect their family and their wealth.

Just like the previous couple, their desired income is $100,000 and their required income is $78,950. However, they have the flexibility to take out $21,050 from any of the three financial toolboxes.

This year, they decide they want to be as tax-efficient as possible and will take dollars from a tax-advantaged toolbox to fill their income gap.

Net worth: Includes assets from all three financial tools: capital assets, retirement income and tax-advantaged

Achieving desired income

The taxpayers with a tax-sensitive distribution strategy desire to be as tax-efficient as possible.

Desired income of $100,000 Sources of income

Required income $78,950 Social Security and RMDs

Income gap $21,050 Filled with income from a tax-advantaged asset (cash value life insurance)

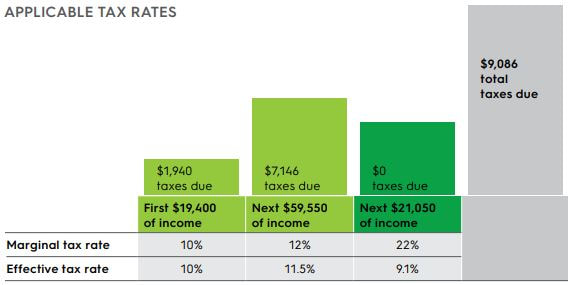

Taxes for tax-sensitive couple

This couple will pay taxes in the first two tax brackets only. Their total taxes due will be $9,086, and their effective tax rate is 9.1 percent.

Couple 2: Has tax-sensitive distribution strategy

The second married couple has the ability to design a tax-sensitive distribution strategy because they are using permanent life insurance to protect their family and their wealth.

Just like the previous couple, their desired income is $100,000 and their required income is $78,950. However, they have the flexibility to take out $21,050 from any of the three financial toolboxes.

This year, they decide they want to be as tax-efficient as possible and will take dollars from a tax-advantaged toolbox to fill their income gap.

Net worth: Includes assets from all three financial tools: capital assets, retirement income and tax-advantaged

Achieving desired income

The taxpayers with a tax-sensitive distribution strategy desire to be as tax-efficient as possible.

Desired income of $100,000 Sources of income

Required income $78,950 Social Security and RMDs

Income gap $21,050 Filled with income from a tax-advantaged asset (cash value life insurance)

Taxes for tax-sensitive couple

This couple will pay taxes in the first two tax brackets only. Their total taxes due will be $9,086, and their effective tax rate is 9.1 percent.

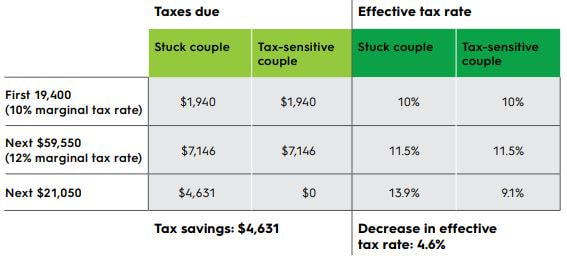

Results

In this case, the second couple has a tax savings of $4,631 and a decrease in the effective tax rate of 4.6 percent compared to the other couple:

In this case, the second couple has a tax savings of $4,631 and a decrease in the effective tax rate of 4.6 percent compared to the other couple:

RSS Feed

RSS Feed