Q. What factors should I consider if I should prepay mortgage or not?

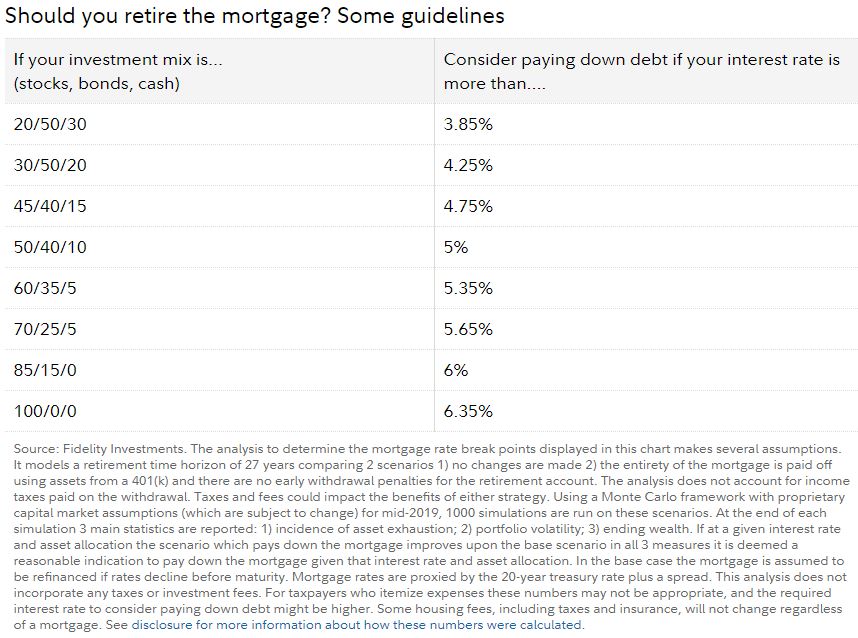

A. You need to consider your portfolio mix when you consider whether to prepay mortgage or not. Below is a guideline from Fidelity -

A. You need to consider your portfolio mix when you consider whether to prepay mortgage or not. Below is a guideline from Fidelity -

Case studies:

Let's take a look at a hypothetical example. Say Joan is 10 years into a 30-year mortgage with an interest rate of 4%, an outstanding balance close to $275,000, and a monthly payment of about $1,300. She is approaching retirement and trying to decide if she should use her savings to pay off the mortgage before she stops working.

Let's say Joan is a conservative investor—she holds about 20% of her portfolio in stocks, about 50% in bonds, and 30% in cash. If she prepays her mortgage, our estimate indicates she will end up improving her financial condition by reducing the risk of running out of money in retirement by about 10%, and improving her final balance by about 3% on average.

But what if she was a more aggressive investor and held 70% of her portfolio in stocks and 25% in bonds and 5% in cash. According to our estimates, if Joan decides to prepay, she would still reduce her risk of running out of money. But in terms of wealth, the outcome would likely change: Instead of increasing her final balance, prepaying the mortgage would actually hurt her wealth. Because her investments would have grown more than savings from repayment, Joan would see her final balance decrease by about 10% on average.

Let's take a look at a hypothetical example. Say Joan is 10 years into a 30-year mortgage with an interest rate of 4%, an outstanding balance close to $275,000, and a monthly payment of about $1,300. She is approaching retirement and trying to decide if she should use her savings to pay off the mortgage before she stops working.

Let's say Joan is a conservative investor—she holds about 20% of her portfolio in stocks, about 50% in bonds, and 30% in cash. If she prepays her mortgage, our estimate indicates she will end up improving her financial condition by reducing the risk of running out of money in retirement by about 10%, and improving her final balance by about 3% on average.

But what if she was a more aggressive investor and held 70% of her portfolio in stocks and 25% in bonds and 5% in cash. According to our estimates, if Joan decides to prepay, she would still reduce her risk of running out of money. But in terms of wealth, the outcome would likely change: Instead of increasing her final balance, prepaying the mortgage would actually hurt her wealth. Because her investments would have grown more than savings from repayment, Joan would see her final balance decrease by about 10% on average.

RSS Feed

RSS Feed