The article below is from an insurance carrier's pension department, it should be very interesting for people who runs his or her own single person business.

What is a Single-Participant 401(k) Plan?

A single-participant 401(k) plan is a 401(k) plan that is sponsored by an employer and has no other employees except the business owner. Under such plans, the business owner wears two hats: his employee hat and his employer hat. A single participant 401(k) plan is typically funded by a combination of employee salary deferral contributions (the “employee” part) and employer profit sharing contributions (the “employer” part).

Taxes, Taxes, Taxes

For years, the conventional wisdom has been that contributions to the plan should be made on a pre-tax basis to defer taxes to the participant’s retirement years when he is expected to be in a lower tax bracket. Employee deferrals have usually been of the pre-tax variety and employer profit sharing contributions have usually been made on a tax-deductible basis.

Does conventional wisdom still hold true today?

For some single-participant 401(k) plan sponsors the answer very well may be no.

The reason for this is the effect that §199A of the Tax Cuts & Jobs Act of 2017 had on the taxation of small businesses such as sole proprietorships, partnerships, S-Corporations and LLCs. For qualifying employers §199A reduces the top marginal tax rate on business income from 37% to 29.6%. The top personal income tax rate remains at 37%.

Therefore, a business owner might ask himself the question, “Does it make sense for me to contribute to a plan and take a deduction at 29.6% when I might pay 37% on the money when I take it out of the plan down the road?”

The business owner has a point. Fortunately, there is a way to provide him with tax-free income at retirement if he chooses to pay taxes on his current contributions instead of waiting to pay tax when he retires. To do so we would follow a three-step process.

Three-Step Process to Maximize Tax Free Income In Retirement

Step One:

Switch from making his salary deferrals on a traditional pre-tax basis to an after-tax Roth basis instead. Everybody can make Roth salary deferral contributions if their 401(k) plan permits it. For 2019, a participant may make up to $19,000 in Roth salary deferrals. Participants age 50 or more may add on an extra $6,000 in Roth catch up contributions.

Roth contributions plus the investment earnings they generate can be withdrawn from the plan tax-free if the Roth deferrals are kept in the plan for the requisite minimum holding period. In general, the required holding period is the later of:

• The fifth year following the year that the first Roth deferral contribution was made, or

• Attainment of age 59 ½

Step Two:

Stop making profit sharing contributions to the plan and instead allow the business owner to make additional voluntary after-tax contributions to the plan. For 2019, this can be as much as $37,000 if the maximum Roth salary deferral has been made.

Voluntary after-tax contributions have been around for a long time but have fallen out of use ever since they became subject to discrimination testing under Code §401(m). As very few, if any, non-highly compensated employees will ever make voluntary after-tax contributions plans that allow them are quite likely to fail discrimination testing and require that voluntary after-tax contributions made by highly compensated employees be refunded.

Discrimination testing is not a concern in a single-participant plan because there are no non-highly paid employees to discriminate against. Such plans can accept voluntary after-tax contributions without any worries.

Discrimination testing also does not apply to plans where the only participants are the owner and his spouse, his children or his parents. It also does not apply if the only participants are co-owners of the business, such as a partnership, as long as each participant owns more than 5% of the business. Testing also does not apply to plans where every participant is a highly compensated employee, i.e. everyone has earnings in excess of $125,000 for 2019.

Add non-highly compensated employees into the mix, even one, and voluntary after-tax contributions will probably be disallowed because of discrimination testing.

Step Three:

Have the business owner elect to make an in-plan Roth conversion of his voluntary after-tax contributions right after they have been made. Since the contributions were made on an after-tax basis there will be no tax consequences from making the Roth conversion election.

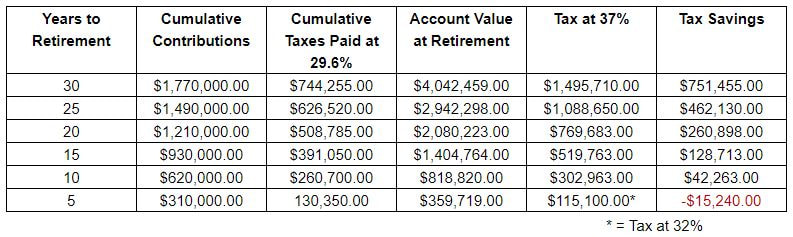

The Results

The results can be very interesting. Here is a chart of potential tax savings assuming that the maximum contribution rate remains unchanged at 2019 levels and the contributions generate an investment return of 5% compounded annually:

What is a Single-Participant 401(k) Plan?

A single-participant 401(k) plan is a 401(k) plan that is sponsored by an employer and has no other employees except the business owner. Under such plans, the business owner wears two hats: his employee hat and his employer hat. A single participant 401(k) plan is typically funded by a combination of employee salary deferral contributions (the “employee” part) and employer profit sharing contributions (the “employer” part).

Taxes, Taxes, Taxes

For years, the conventional wisdom has been that contributions to the plan should be made on a pre-tax basis to defer taxes to the participant’s retirement years when he is expected to be in a lower tax bracket. Employee deferrals have usually been of the pre-tax variety and employer profit sharing contributions have usually been made on a tax-deductible basis.

Does conventional wisdom still hold true today?

For some single-participant 401(k) plan sponsors the answer very well may be no.

The reason for this is the effect that §199A of the Tax Cuts & Jobs Act of 2017 had on the taxation of small businesses such as sole proprietorships, partnerships, S-Corporations and LLCs. For qualifying employers §199A reduces the top marginal tax rate on business income from 37% to 29.6%. The top personal income tax rate remains at 37%.

Therefore, a business owner might ask himself the question, “Does it make sense for me to contribute to a plan and take a deduction at 29.6% when I might pay 37% on the money when I take it out of the plan down the road?”

The business owner has a point. Fortunately, there is a way to provide him with tax-free income at retirement if he chooses to pay taxes on his current contributions instead of waiting to pay tax when he retires. To do so we would follow a three-step process.

Three-Step Process to Maximize Tax Free Income In Retirement

Step One:

Switch from making his salary deferrals on a traditional pre-tax basis to an after-tax Roth basis instead. Everybody can make Roth salary deferral contributions if their 401(k) plan permits it. For 2019, a participant may make up to $19,000 in Roth salary deferrals. Participants age 50 or more may add on an extra $6,000 in Roth catch up contributions.

Roth contributions plus the investment earnings they generate can be withdrawn from the plan tax-free if the Roth deferrals are kept in the plan for the requisite minimum holding period. In general, the required holding period is the later of:

• The fifth year following the year that the first Roth deferral contribution was made, or

• Attainment of age 59 ½

Step Two:

Stop making profit sharing contributions to the plan and instead allow the business owner to make additional voluntary after-tax contributions to the plan. For 2019, this can be as much as $37,000 if the maximum Roth salary deferral has been made.

Voluntary after-tax contributions have been around for a long time but have fallen out of use ever since they became subject to discrimination testing under Code §401(m). As very few, if any, non-highly compensated employees will ever make voluntary after-tax contributions plans that allow them are quite likely to fail discrimination testing and require that voluntary after-tax contributions made by highly compensated employees be refunded.

Discrimination testing is not a concern in a single-participant plan because there are no non-highly paid employees to discriminate against. Such plans can accept voluntary after-tax contributions without any worries.

Discrimination testing also does not apply to plans where the only participants are the owner and his spouse, his children or his parents. It also does not apply if the only participants are co-owners of the business, such as a partnership, as long as each participant owns more than 5% of the business. Testing also does not apply to plans where every participant is a highly compensated employee, i.e. everyone has earnings in excess of $125,000 for 2019.

Add non-highly compensated employees into the mix, even one, and voluntary after-tax contributions will probably be disallowed because of discrimination testing.

Step Three:

Have the business owner elect to make an in-plan Roth conversion of his voluntary after-tax contributions right after they have been made. Since the contributions were made on an after-tax basis there will be no tax consequences from making the Roth conversion election.

The Results

The results can be very interesting. Here is a chart of potential tax savings assuming that the maximum contribution rate remains unchanged at 2019 levels and the contributions generate an investment return of 5% compounded annually:

For most participants except those nearing retirement Roth salary deferral contributions and Roth conversions of voluntary after-tax contributions can be an attractive option.

If you found the above piece interesting, we can help you set up retirement plans for you, please contact us here.

If you found the above piece interesting, we can help you set up retirement plans for you, please contact us here.

RSS Feed

RSS Feed