For people who have tax deductions that exceed their total income – in essence, having negative income – they can benefit from a 0% tax rate on Roth conversions or other ordinary income tax events (as increasing income from negative to zero still won’t owe any taxes on the additional income).

A Case Study

Blanche is a 60-year-old widow who lives in a fully-paid-off Florida home, living primarily off her husband’s Social Security survivor benefits of $24,000/year, plus $500/month that she generates via tax-free municipal bond interest from a $300,000 brokerage account (while she leaves her $300,000 IRA untouched until the RMD phase more than a decade from now).

For income tax purposes, Blanche’s Social Security benefits are not taxable (as her Social Security provisional income is 50% x $24,000 + $6,000 (bond interest) = $18,000, well below the $25,000 threshold that triggers taxation of Social Security.

As a result, Blanche’s total taxable income is $0 (as her $24,000 of Social Security benefits are not taxable, nor is the $6,000/year of municipal bond interest), which means with a $12,400 standard deduction, Blanche’s taxable income will actually be -$12,400!

Accordingly, Blanche decides to do a $10,600 partial Roth conversion, which increases her income by $12,400 (as it causes her Social Security provisional income to rise to $28,600, causing $1,800 of her Social Security benefits to become taxable). Still, though, Blanche’s actual tax liability is not increased, as her standard deduction of $12,400 is still enough to offset the $12,400 of additional income.

Thus Blanche is able to move $10,600 from her IRA to a Roth IRA at a tax rate of 0%.

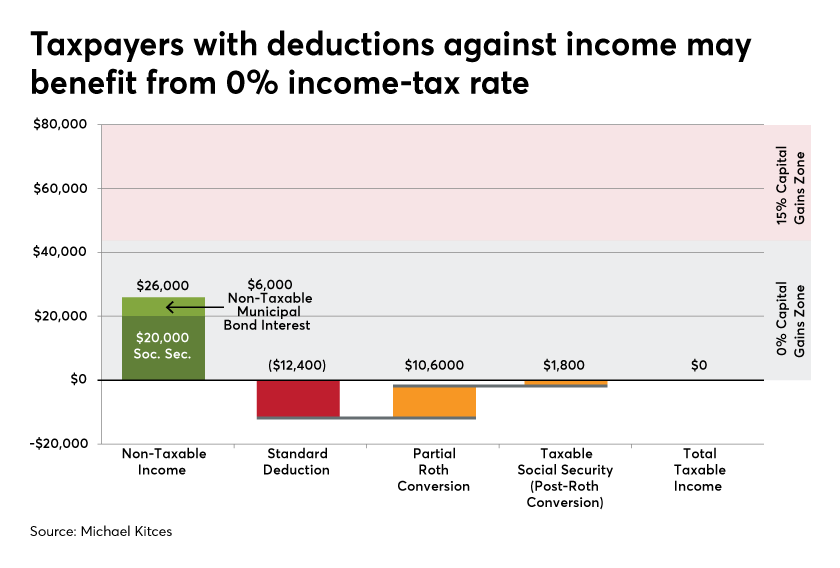

A Case Study

Blanche is a 60-year-old widow who lives in a fully-paid-off Florida home, living primarily off her husband’s Social Security survivor benefits of $24,000/year, plus $500/month that she generates via tax-free municipal bond interest from a $300,000 brokerage account (while she leaves her $300,000 IRA untouched until the RMD phase more than a decade from now).

For income tax purposes, Blanche’s Social Security benefits are not taxable (as her Social Security provisional income is 50% x $24,000 + $6,000 (bond interest) = $18,000, well below the $25,000 threshold that triggers taxation of Social Security.

As a result, Blanche’s total taxable income is $0 (as her $24,000 of Social Security benefits are not taxable, nor is the $6,000/year of municipal bond interest), which means with a $12,400 standard deduction, Blanche’s taxable income will actually be -$12,400!

Accordingly, Blanche decides to do a $10,600 partial Roth conversion, which increases her income by $12,400 (as it causes her Social Security provisional income to rise to $28,600, causing $1,800 of her Social Security benefits to become taxable). Still, though, Blanche’s actual tax liability is not increased, as her standard deduction of $12,400 is still enough to offset the $12,400 of additional income.

Thus Blanche is able to move $10,600 from her IRA to a Roth IRA at a tax rate of 0%.

RSS Feed

RSS Feed