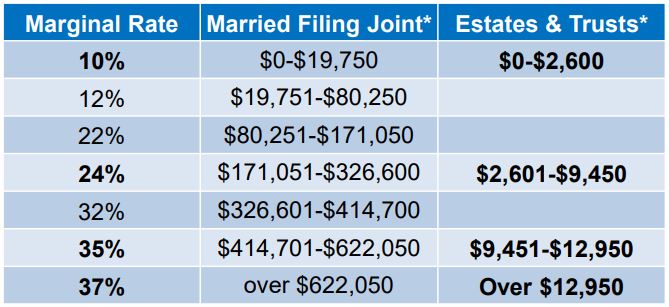

Irrevocable non-grantor trust is taxed at trust rates, see table below.

Benefits of Non-grantor irrevocable trusts –

A case study

Ann Weston has two children

Trustees discusses benefits of using a nonqualified deferred annuity.

What are the benefits?

There are two options to consider.

Option 1. Purchase one nonqualified deferred annuity for $1M with Ann as the annuitant

Option 2. Purchase two nonqualified deferred annuities for $500K each

- Credit shelter trusts

- Revocable living trusts upon death of the grantor

A case study

Ann Weston has two children

- Jon – son of Ann’s second husband, Robert, and his first wife

- Julie – daughter of Ann and her first husband

- Wish to leave a legacy for their two children

- Upon Robert’s death, trust was funded with $6M

Trustees discusses benefits of using a nonqualified deferred annuity.

What are the benefits?

- Avoids higher trust income taxes until distributed

- Avoids 3.8% net investment income tax, if applicable

- Trustee buys nonqualified annuity contract to benefit trust beneficiary

- Trust is owner and beneficiary of annuity

- Trustee names annuitant

There are two options to consider.

Option 1. Purchase one nonqualified deferred annuity for $1M with Ann as the annuitant

- Trust purchases one $1M annuity

- 50% of death benefit distributed and taxed to Jon at Ann's death

- 50% of death benefit distributed and taxed to Julie at Ann's death

Option 2. Purchase two nonqualified deferred annuities for $500K each

- Jon named as annuitant on one

- Julie named as annuitant on the other

- Trust purchases two $500K annuities

- Jon and Julie each is named as the annuitant of one annuity contract

- Trustee distributes annuity contract to Jon and Julie respectively at Ann's death - no taxation

RSS Feed

RSS Feed