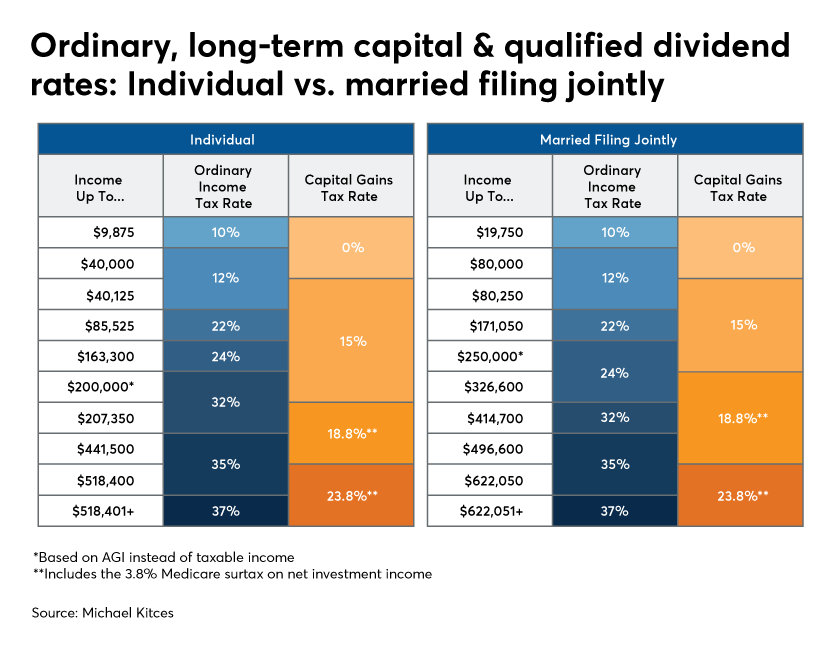

Income harvesting strategies can be especially appealing in scenarios where the income itself can actually be harvested tax free (i.e., at a 0% tax rate).

For instance, those who are in the bottom two ordinary income tax brackets (i.e., the 10% and 12% brackets) are eligible for a 0% long-term capital gains rate on any capital gains (or qualified dividends) that also fall within those tax brackets (at least for federal tax purposes).

For instance, those who are in the bottom two ordinary income tax brackets (i.e., the 10% and 12% brackets) are eligible for a 0% long-term capital gains rate on any capital gains (or qualified dividends) that also fall within those tax brackets (at least for federal tax purposes).

A Case Study

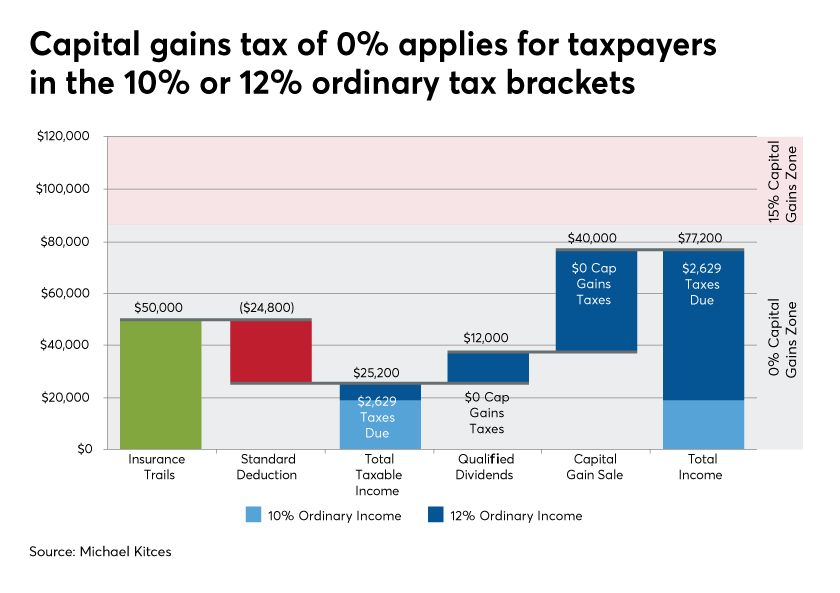

Rose and Charlie retired early at age 55, living off $50,000/year of Charlie’s insurance trails (as a former insurance agent), plus $1,000/month from the dividends generated by a $400,000 brokerage account (which include $70,000 of embedded capital gains from recent market growth), while they wait for their Social Security benefits to begin (and wait to tap Charlie’s $300,000 IRA).

With a standard deduction of $24,800 in 2020, the couple’s ordinary income (after deductions) is only $50,000 – $24,800 = $25,200, placing the couple at the bottom end of the 12% tax bracket (which in 2020 runs from $19,750 to $80,250 of income after deductions). In fact, even with the additional $12,000/year of dividends, the couple’s income would still be in the 12% tax bracket… which means their (assumed-to-be-qualified) dividends are eligible for a 0% tax rate.

Accordingly, the couple chooses to proactively sell the most appreciated investments (a $90,000 ETF with a $50,000 cost basis) in their brokerage account to cause a $40,000 long-term capital gain. That brings their total income up to $50,000 + $12,000 + 40,000 – $24,800 = $77,200.

Because their total income after deductions is still below the $80,250 upper threshold for the 12% tax bracket, they will enjoy a 0% federal tax rate on both the qualified dividends and the $40,000 of long-term capital gains.

Rose and Charlie retired early at age 55, living off $50,000/year of Charlie’s insurance trails (as a former insurance agent), plus $1,000/month from the dividends generated by a $400,000 brokerage account (which include $70,000 of embedded capital gains from recent market growth), while they wait for their Social Security benefits to begin (and wait to tap Charlie’s $300,000 IRA).

With a standard deduction of $24,800 in 2020, the couple’s ordinary income (after deductions) is only $50,000 – $24,800 = $25,200, placing the couple at the bottom end of the 12% tax bracket (which in 2020 runs from $19,750 to $80,250 of income after deductions). In fact, even with the additional $12,000/year of dividends, the couple’s income would still be in the 12% tax bracket… which means their (assumed-to-be-qualified) dividends are eligible for a 0% tax rate.

Accordingly, the couple chooses to proactively sell the most appreciated investments (a $90,000 ETF with a $50,000 cost basis) in their brokerage account to cause a $40,000 long-term capital gain. That brings their total income up to $50,000 + $12,000 + 40,000 – $24,800 = $77,200.

Because their total income after deductions is still below the $80,250 upper threshold for the 12% tax bracket, they will enjoy a 0% federal tax rate on both the qualified dividends and the $40,000 of long-term capital gains.

RSS Feed

RSS Feed