Below is an article from Dec 4 2020 WSJ:

Amid a wave of optimism in financial markets, investors can relax about the expected profit rebound in 2021. They might worry more about 2022.

Amid a wave of optimism in financial markets, investors can relax about the expected profit rebound in 2021. They might worry more about 2022.

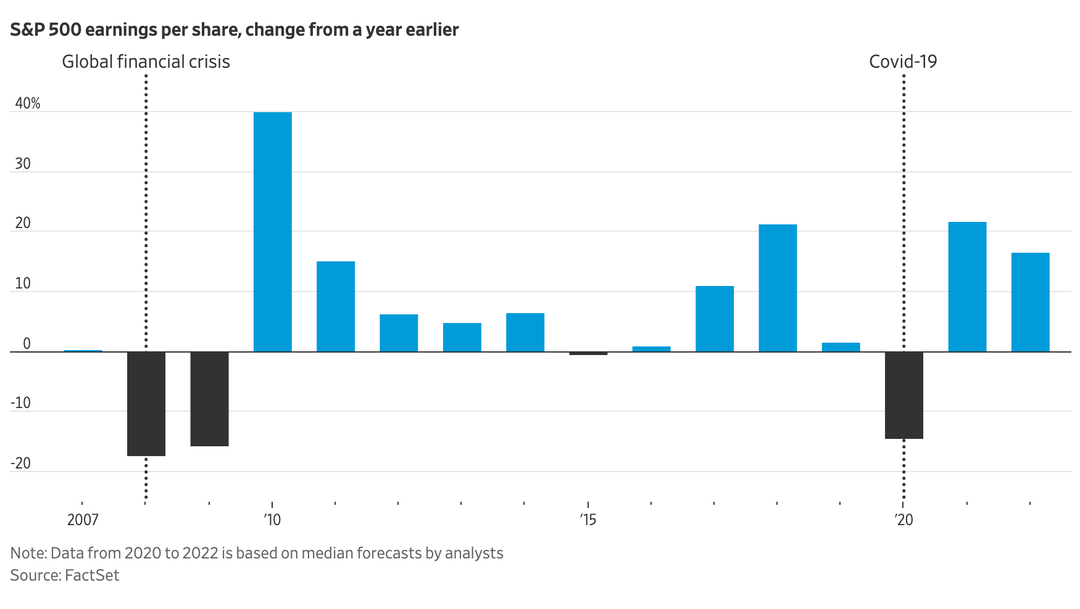

Wall Street is factoring in a 22% increase in S&P 500 earnings per share for next year. This seems reasonable, even cautious, following the expected 15% fall this year. This summer showed that consumption can return very quickly when restrictions are eased, and global trade and manufacturing already seem to be on a steady path to recovery. In 2010, after the global financial crash, profit growth was 40% as a result of a dismal 2009.

But forecasts for 2022, the first “normal” year after the crisis, say more about what the market is thinking. Those expectations look less grounded.

As of now, S&P 500 earnings per share are seen expanding another 17% in 2022. This is in line with what happened in 2011, when they rose 15%. Back then, however, profits were far less elevated because the downturn had lasted longer: Relative to their 2007 peak, they were up only 11% in 2011. Current expectations of 2022 earnings place them 21% above 2019 levels. Consumer-cyclical companies such as auto makers and hotels would be up 35% overall.

Stocks look expensive compared with 2019 profits: 48% of companies in the broader S&P Composite 1500 index trade at higher valuations than at the end of last year. The proportion is broadly unchanged relative to 2021 earnings. Yet the figure falls to 29% when 2022 expectations are used for the calculation.

But forecasts for 2022, the first “normal” year after the crisis, say more about what the market is thinking. Those expectations look less grounded.

As of now, S&P 500 earnings per share are seen expanding another 17% in 2022. This is in line with what happened in 2011, when they rose 15%. Back then, however, profits were far less elevated because the downturn had lasted longer: Relative to their 2007 peak, they were up only 11% in 2011. Current expectations of 2022 earnings place them 21% above 2019 levels. Consumer-cyclical companies such as auto makers and hotels would be up 35% overall.

Stocks look expensive compared with 2019 profits: 48% of companies in the broader S&P Composite 1500 index trade at higher valuations than at the end of last year. The proportion is broadly unchanged relative to 2021 earnings. Yet the figure falls to 29% when 2022 expectations are used for the calculation.

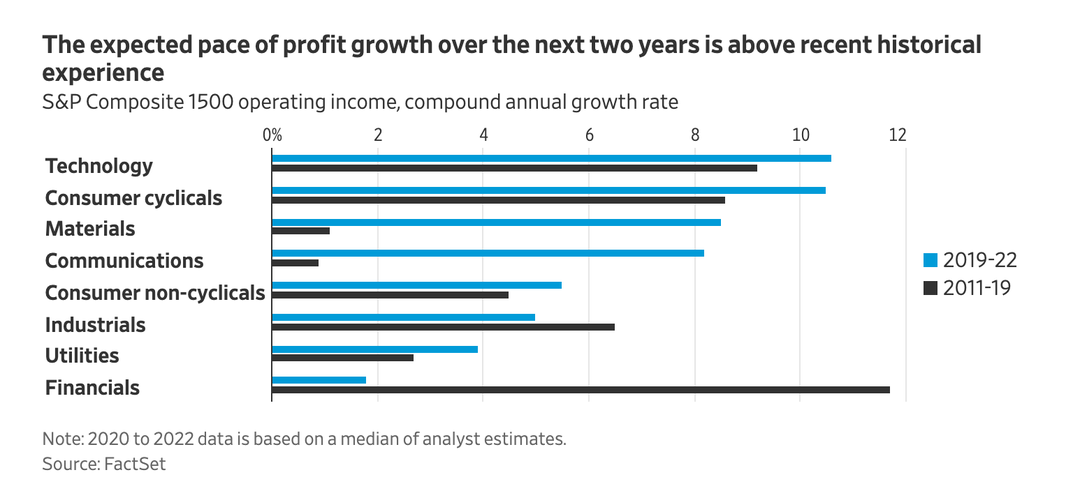

In many S&P 1500 sectors, to make good on such forecasts, the compound annual growth rate in earnings from 2019 to 2022 would need to be above the recent historical norm—itself inflated by the impact of President Trump’s tax cuts in 2018. Maybe tech companies will gain an edge from the pandemic. It is harder to argue that other industries will emerge from this crisis permanently reinforced.

In short: Markets are baking in not just a “V-shaped” rebound next year but also a consumer-led boom in 2022.

Such a scenario is possible. Pent-up savings will kick in after the economy reopens, especially if U.S. lawmakers manage to agree on a new round of fiscal aid. Still, the growing ranks of long-term unemployed, as well as potential trouble overseas—for example, among the weaker European economies—are reminders of the risk that the global economy will emerge scarred by Covid-19.

Staying invested in stocks makes sense for now, given the potential for upgrades to 2021 forecasts. Longer term, caution is warranted when it comes to fully embracing cyclical sectors, particularly pandemic-battered “value” stocks like hotels and airlines, despite the enthusiastic New Year outlooks that asset managers are publishing at the moment.

A rebound from pandemic troughs is almost a given. A 2022 economy that looks much better than 2019’s isn’t.

In short: Markets are baking in not just a “V-shaped” rebound next year but also a consumer-led boom in 2022.

Such a scenario is possible. Pent-up savings will kick in after the economy reopens, especially if U.S. lawmakers manage to agree on a new round of fiscal aid. Still, the growing ranks of long-term unemployed, as well as potential trouble overseas—for example, among the weaker European economies—are reminders of the risk that the global economy will emerge scarred by Covid-19.

Staying invested in stocks makes sense for now, given the potential for upgrades to 2021 forecasts. Longer term, caution is warranted when it comes to fully embracing cyclical sectors, particularly pandemic-battered “value” stocks like hotels and airlines, despite the enthusiastic New Year outlooks that asset managers are publishing at the moment.

A rebound from pandemic troughs is almost a given. A 2022 economy that looks much better than 2019’s isn’t.

RSS Feed

RSS Feed