The greatest strength of life insurance lies in the ability to provide money to a family when someone passes away. Sometimes this amount can be many multiples of the premiums that were paid into the insurance policy.

Many people think of life insurance only as a way to provide for a family after the loss of a breadwinner. But some families are also using life insurance as an asset to ensure that an inheritance can be passed on to their family, regardless of how their other assets perform. This is increasingly important to many families who are still uneasy after the 2008 market crash and unsure of where the market is headed. A badly timed down market can devastate a planned legacy for years. The chart below shows market fluctuations in recent years, based on the 5-year S&P 500® Index, without dividends.

By taking a portion of your assets each year to cover the cost of life insurance premiums, you may be able to hedge a portion of your portfolio against fluctuations in the marketplace, because payment comes from the life insurance company, not your assets directly. Knowing that your beneficiaries will be cared for may also allow you to make other choices with your remaining assets — perhaps a more aggressive, growth-oriented strategy, or you might invest more conservatively, knowing you don’t need as much growth.

How the strategy works

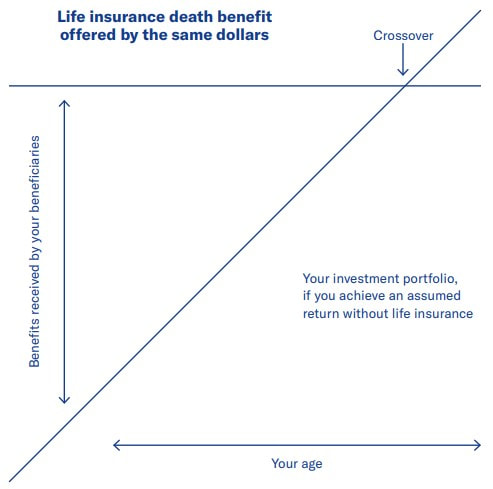

A hypothetical example of how the strategy works can be seen in the chart below. It shows what you might expect from the same dollars if they were paid into a life insurance policy as premiums, or if they were placed in a hypothetical investment account.

In the early years, life insurance death benefits typically offer substantially more than the hypothetical investment. As time goes on, the leverage offered by life insurance may be reduced as the non-life insurance assets grow and compound. At some point there is a crossover, where the growth in the investment account outweighs the benefit provided by the life insurance policy. Of course, it’s hard to know which strategy is more beneficial unless someone knows their precise life expectancy, and whether it is before or after this crossover point.

However, this is a conversation you can have with your financial professional. They can run numbers for you and estimate the internal rate of return in the years before and after your life expectancy.

For you to get the most out of your policy’s life insurance benefit, it has to stay inforce until you pass away. If your policy ends or terminates, or if you otherwise dispose of your policy before your death, your beneficiaries would receive a substantially reduced benefit, and any proceeds they would receive above the premiums paid into the contract could be subject to income taxation.

Many people think of life insurance only as a way to provide for a family after the loss of a breadwinner. But some families are also using life insurance as an asset to ensure that an inheritance can be passed on to their family, regardless of how their other assets perform. This is increasingly important to many families who are still uneasy after the 2008 market crash and unsure of where the market is headed. A badly timed down market can devastate a planned legacy for years. The chart below shows market fluctuations in recent years, based on the 5-year S&P 500® Index, without dividends.

By taking a portion of your assets each year to cover the cost of life insurance premiums, you may be able to hedge a portion of your portfolio against fluctuations in the marketplace, because payment comes from the life insurance company, not your assets directly. Knowing that your beneficiaries will be cared for may also allow you to make other choices with your remaining assets — perhaps a more aggressive, growth-oriented strategy, or you might invest more conservatively, knowing you don’t need as much growth.

How the strategy works

A hypothetical example of how the strategy works can be seen in the chart below. It shows what you might expect from the same dollars if they were paid into a life insurance policy as premiums, or if they were placed in a hypothetical investment account.

In the early years, life insurance death benefits typically offer substantially more than the hypothetical investment. As time goes on, the leverage offered by life insurance may be reduced as the non-life insurance assets grow and compound. At some point there is a crossover, where the growth in the investment account outweighs the benefit provided by the life insurance policy. Of course, it’s hard to know which strategy is more beneficial unless someone knows their precise life expectancy, and whether it is before or after this crossover point.

However, this is a conversation you can have with your financial professional. They can run numbers for you and estimate the internal rate of return in the years before and after your life expectancy.

For you to get the most out of your policy’s life insurance benefit, it has to stay inforce until you pass away. If your policy ends or terminates, or if you otherwise dispose of your policy before your death, your beneficiaries would receive a substantially reduced benefit, and any proceeds they would receive above the premiums paid into the contract could be subject to income taxation.

In next blogpost, we will show a case study to illustrate life insurance as an asset in action.

RSS Feed

RSS Feed