RMD Factors Revised for 2022

IRS regulations have updated the life expectancy tables used in calculating required minimum distributions (RMDs). The new tables are effective for distribution years beginning on or after January 1, 2022. They replace old tables that were last updated in 2002.

Need to Know: Taxpayers turning 72 in 2021 and having a required beginning date of April 1, 2022, cannot use the new tables to calculate their RMD for 2021 (even though they have until April 1, 2022 to take that first distribution).

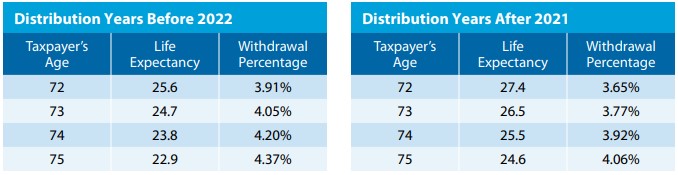

The Effect: RMDs Reduced The new tables contain updated distribution periods that reflect increased life expectancies since the last tables were issued. The differences in the tables are not huge. However, use of the new tables will result in smaller RMDs. The below compares a small portion of the Uniform Lifetime Table.

The new tables are easy to use for lifetime RMDs. Taxpayers simply use the new table to calculate their RMDs for their 2022 distribution year.

For Example: IRA Owner, Age 75 Patty turns 75 in 2022. Her one IRA had a value of $550,000 as of 12/31/21. She must distribute a minimum of $22,357.72 ($550,000/24.6) before 12/31/22. This is $1,659.75 less than the $24,017.47 that would have been required under the old table ($550,000/22.9).

IRS regulations have updated the life expectancy tables used in calculating required minimum distributions (RMDs). The new tables are effective for distribution years beginning on or after January 1, 2022. They replace old tables that were last updated in 2002.

Need to Know: Taxpayers turning 72 in 2021 and having a required beginning date of April 1, 2022, cannot use the new tables to calculate their RMD for 2021 (even though they have until April 1, 2022 to take that first distribution).

The Effect: RMDs Reduced The new tables contain updated distribution periods that reflect increased life expectancies since the last tables were issued. The differences in the tables are not huge. However, use of the new tables will result in smaller RMDs. The below compares a small portion of the Uniform Lifetime Table.

The new tables are easy to use for lifetime RMDs. Taxpayers simply use the new table to calculate their RMDs for their 2022 distribution year.

For Example: IRA Owner, Age 75 Patty turns 75 in 2022. Her one IRA had a value of $550,000 as of 12/31/21. She must distribute a minimum of $22,357.72 ($550,000/24.6) before 12/31/22. This is $1,659.75 less than the $24,017.47 that would have been required under the old table ($550,000/22.9).

RSS Feed

RSS Feed