In our last blog post, we showed that the large cap U.S. stocks portfolio had a better return than a diversified 7-asset portfolio over 46 years time period. Now we will compare risks of the two portfolios, because the better return could be due to taking higher risk, it's important to understand what's an investment's risk.

But how to measure the risk of a portfolio? There are actually a few different ways to measure the risk.

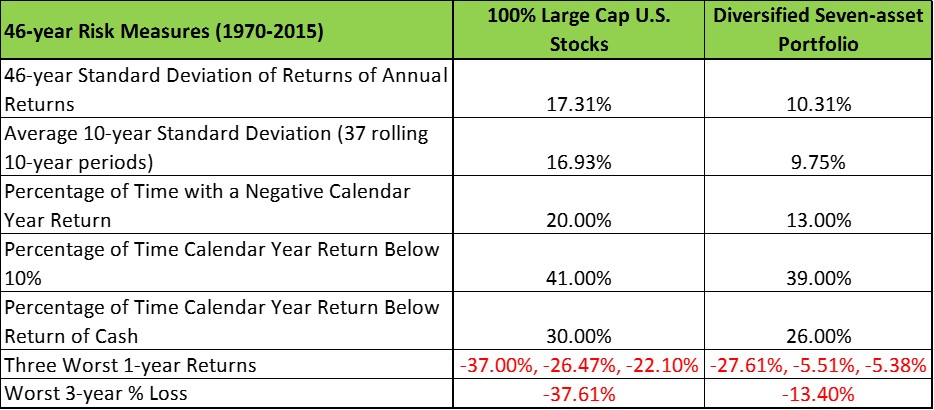

1. Standard Deviation of Return

This is a measure many investor find hard to understand, but intuitively low standard deviation means low risk. The standard deviation of the large cap US stocks portfolio is 17.31% over the 46-year period, a lot higher than the standard deviation of 10.31% of the 7-asset diversified portfolio.

If we measure the standard deviation of the 37 rolling 10-year periods' annual returns, we would get similar results - the large cap US stocks portfolio had 16.93% standard deviation of the rolling 10-year annual return, versus the 9.75% of the diversified portfolio.

2. Percentage of Time Had Negative Annual Returns

This is a measure easy to accept, no investor likes to lose money in any calendar year. The large cap US stocks portfolio had 20% of time over the 46 years had negative returns, again, a lot higher than the 13% of time the diversified portfolio had negative calendar year returns.

We can also look at the percentage of time had returns less than 10% and less than the return of cash, respectively. The answers are the same - the large cap US stocks portfolio had higher percentage of time with lower than 10% return and lower than cash returns!

3. Three Worst Annual Returns

For many investors who tried to time the market with their investment, a shorter term horizon and the associated return are good metrics to pay attention to. We will look at the worst 3 1-year return during the 46 years for the two portfolios, unfortunately here the large cap US stocks portfolio looks pretty risky: its 3 worst one-year returns were -37% (2008), -26.47% (1974), and -22.10% (2002). The three worst one-year returns for the diversified portfolio were a lot better: -27.61% (2008), -5.51% (2001), and -5.38% (1974).

4. 3-year Maximum Drawdown

This measure looks at the worst-case 3-year return. Of the 44 3-year rolling periods, the large cap US stocks portfolio had a worst 3-year loss of -37.61%, which should be very scary to any investor. As a comparison, the diversified portfolio's worst 3-year return was -13.40%.

The conclusion: a diversified portfolio is less risky than a portfolio consisting of only large-cap U.S. stock.

But how to measure the risk of a portfolio? There are actually a few different ways to measure the risk.

1. Standard Deviation of Return

This is a measure many investor find hard to understand, but intuitively low standard deviation means low risk. The standard deviation of the large cap US stocks portfolio is 17.31% over the 46-year period, a lot higher than the standard deviation of 10.31% of the 7-asset diversified portfolio.

If we measure the standard deviation of the 37 rolling 10-year periods' annual returns, we would get similar results - the large cap US stocks portfolio had 16.93% standard deviation of the rolling 10-year annual return, versus the 9.75% of the diversified portfolio.

2. Percentage of Time Had Negative Annual Returns

This is a measure easy to accept, no investor likes to lose money in any calendar year. The large cap US stocks portfolio had 20% of time over the 46 years had negative returns, again, a lot higher than the 13% of time the diversified portfolio had negative calendar year returns.

We can also look at the percentage of time had returns less than 10% and less than the return of cash, respectively. The answers are the same - the large cap US stocks portfolio had higher percentage of time with lower than 10% return and lower than cash returns!

3. Three Worst Annual Returns

For many investors who tried to time the market with their investment, a shorter term horizon and the associated return are good metrics to pay attention to. We will look at the worst 3 1-year return during the 46 years for the two portfolios, unfortunately here the large cap US stocks portfolio looks pretty risky: its 3 worst one-year returns were -37% (2008), -26.47% (1974), and -22.10% (2002). The three worst one-year returns for the diversified portfolio were a lot better: -27.61% (2008), -5.51% (2001), and -5.38% (1974).

4. 3-year Maximum Drawdown

This measure looks at the worst-case 3-year return. Of the 44 3-year rolling periods, the large cap US stocks portfolio had a worst 3-year loss of -37.61%, which should be very scary to any investor. As a comparison, the diversified portfolio's worst 3-year return was -13.40%.

The conclusion: a diversified portfolio is less risky than a portfolio consisting of only large-cap U.S. stock.

In our next blog post, we will put together our return and risk analysis of the two portfolios and draw some final conclusions.

RSS Feed

RSS Feed