Q. How much can I safely withdraw from my retirement portfolio?”

A. While there are so many personal variables to factor in, you can actually determine the best annual withdrawal rate, based on the analysis below.

The analysis below is based on a portfolio composed of four primary asset classes with annual rebalancing:

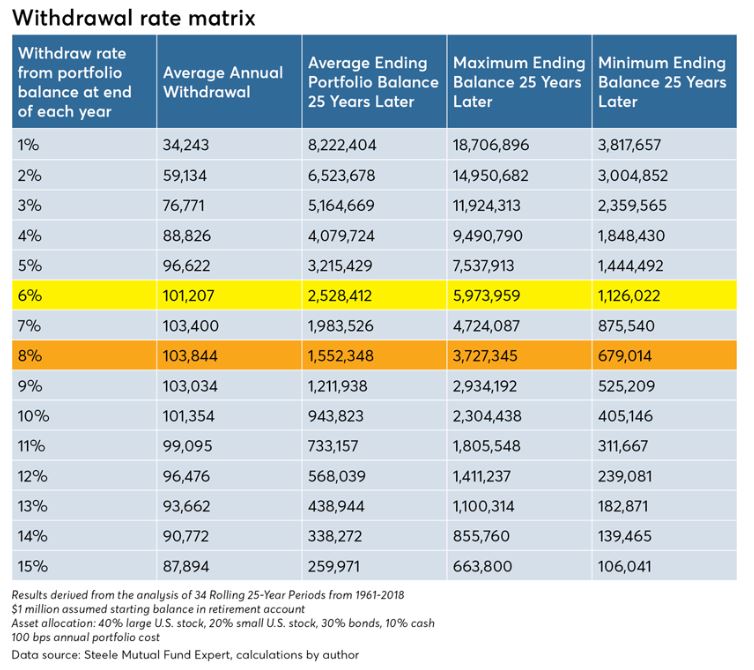

A starting balance of $1 million was assumed at age 70. The four-asset retirement portfolio was tested using 15 different withdrawal rates ranging from 1% to 15% for each of the 34 rolling 25-year periods.

The results were compiled and averages computed. The impact of taxes was not accounted for. This analysis also assumes the retirement portfolio was not subject to the RMD, which would be the case for a Roth IRA account.

A. While there are so many personal variables to factor in, you can actually determine the best annual withdrawal rate, based on the analysis below.

The analysis below is based on a portfolio composed of four primary asset classes with annual rebalancing:

- large U.S. stock (40%)

- small U.S. stock (20%)

- U.S. aggregate bonds (30%)

- U.S. cash (10%)

A starting balance of $1 million was assumed at age 70. The four-asset retirement portfolio was tested using 15 different withdrawal rates ranging from 1% to 15% for each of the 34 rolling 25-year periods.

The results were compiled and averages computed. The impact of taxes was not accounted for. This analysis also assumes the retirement portfolio was not subject to the RMD, which would be the case for a Roth IRA account.

A 6% withdrawal rate is highlighted because it represents the highest withdrawal rate that never produced an ending balance lower than the starting balance of $1 million.

The withdrawal rate of 8% is highlighted because it represents the withdrawal rate that maximized the average annual withdrawal. In this case, it was $103,844.

The withdrawal rate of 8% is highlighted because it represents the withdrawal rate that maximized the average annual withdrawal. In this case, it was $103,844.

RSS Feed

RSS Feed