Q. Which term life products have chronic illness rider included?

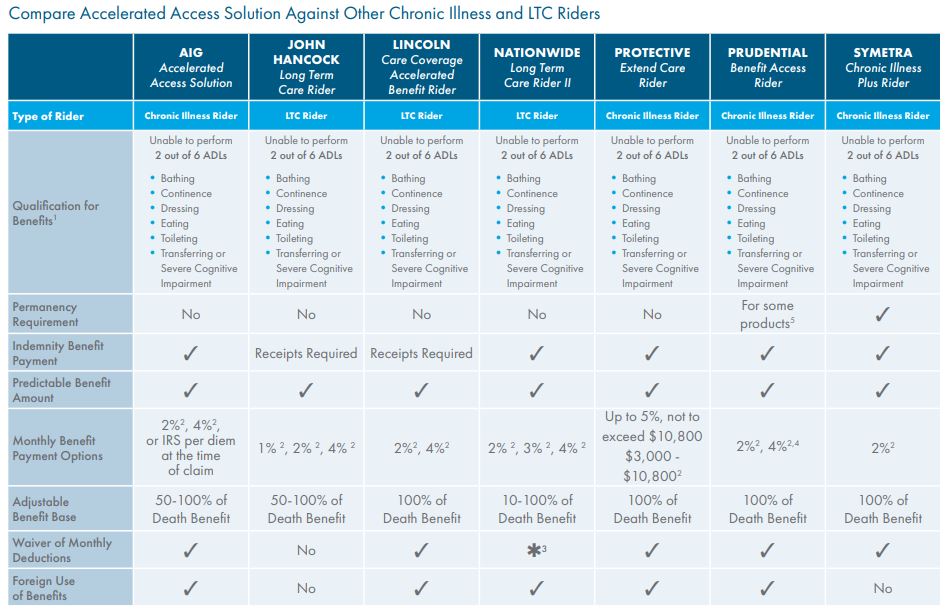

A. There is a new trend in term life product offerings - accelerated access solution that is innovative and flexible that allows policy owners to customize their chronic illness coverage and monthly payout according to their financial needs. It helps with unexpected healthcare costs as well as other expenses due to chronic illness if it not a permanent condition. Besides, it pays benefit on an indemnity basis - no receipts required and family care is covered!

Below is a comparison of some current offerings on the marketplace:

A. There is a new trend in term life product offerings - accelerated access solution that is innovative and flexible that allows policy owners to customize their chronic illness coverage and monthly payout according to their financial needs. It helps with unexpected healthcare costs as well as other expenses due to chronic illness if it not a permanent condition. Besides, it pays benefit on an indemnity basis - no receipts required and family care is covered!

Below is a comparison of some current offerings on the marketplace:

If you are interested in any term life products with living benefits riders, please contact us.

RSS Feed

RSS Feed