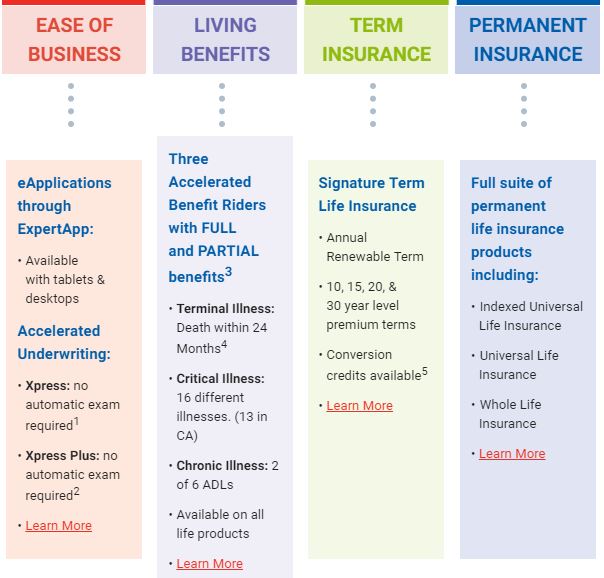

Below is a marketing flyer from American National that introduces many benefits of choosing American National for your life insurance needs - accelerated underwriting and 3 free living benefits riders are very attractive and unique among all life insurance carriers:

RSS Feed

RSS Feed