Q. I expect my tax rate will be lower in retirement than when working, why I should still invest in Roth IRA?

A. If you know for sure your future tax rate will be lower, then invest in traditional IRA.

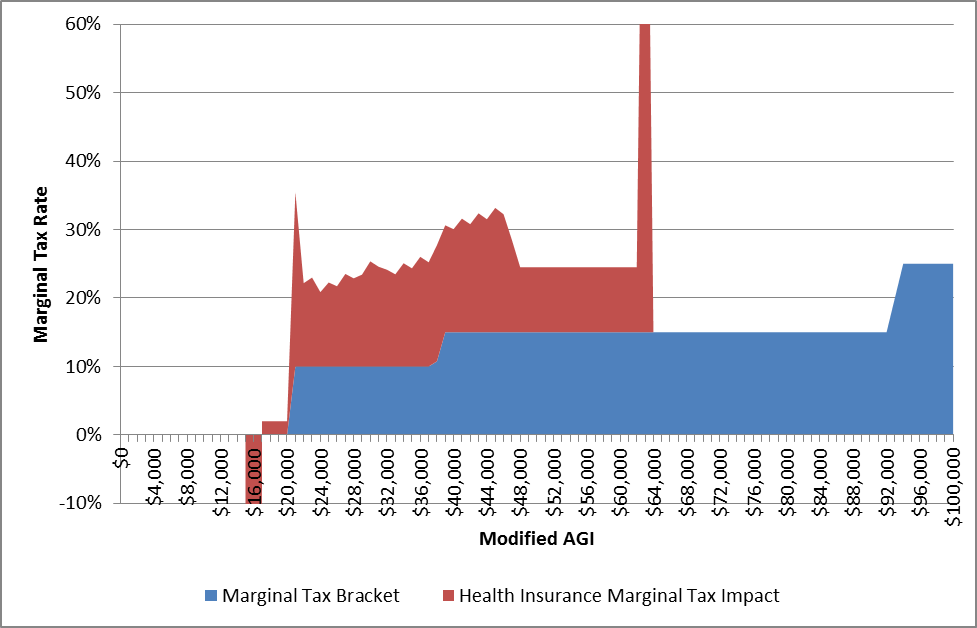

However, tax rates are hovering around historical lows and can only go up in the future.

In addition, Roth IRA has several advantages the Traditional IRA doesn't have:

A. If you know for sure your future tax rate will be lower, then invest in traditional IRA.

However, tax rates are hovering around historical lows and can only go up in the future.

In addition, Roth IRA has several advantages the Traditional IRA doesn't have:

- It's like an emergency fund. You can always withdraw money you have contributed to a Roth without any tax or penalty. For traditional IRA, any withdrawals made before age 59 and half will be hit with a 10% early withdrawal penalty.

- No required minimum distribution (RMD). Roth IRA gives you a lot more flexibility in retirement. For traditional IRA, you have to take an RMD beginning with the year you turn 70 and half. The RMD becomes part of your adjusted gross income for the year. Even if you don't need that money, you still have to take the distribution.

RSS Feed

RSS Feed