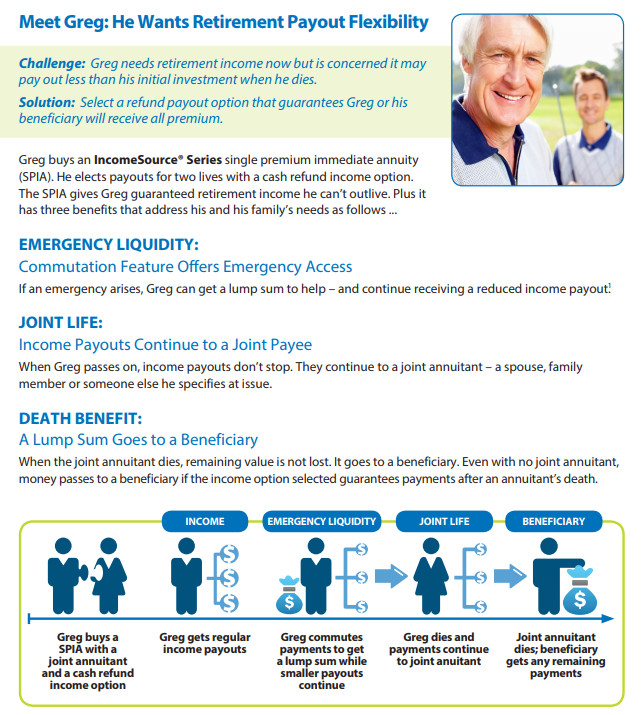

Challenge: Greg needs retirement income now but is concerned it may pay out less than his initial investment when he dies.

Solution: Select a refund payout option that guarantees Greg or his beneficiary will receive all premium.

Solution: Select a refund payout option that guarantees Greg or his beneficiary will receive all premium.

RSS Feed

RSS Feed