1. People => Problems => Solutions => Impact => More People

2. Product => Prospects => Persuasion => Sale => More Products

Which one is better?

2. Product => Prospects => Persuasion => Sale => More Products

Which one is better?

|

|

|

1. People => Problems => Solutions => Impact => More People

2. Product => Prospects => Persuasion => Sale => More Products Which one is better?

0 Comments

Q. I won the court eviction and the tenant moved out, now the hard part, how can I collect the money owed by him?

A. If you are an individual real estate investor, usually your chance of recovering that owed money is nil. No lawyer is willing to take it on a success-basis. You can certainly pay the debt collectors upfront a fee to collect, but there is no guarantee assured, assume you can find one who is willing to take your case. Now there is a new start up that has developed an automated debt recovery platform that bridges the gap between the creditor and those in debt - Trueaccord.com It works with large and small businesses to recover lost money, on a success-basis, with 1/3 of the recovered money as its reward. Sounds fair? Give Trueaccord a try! Q. Which is better: actively managed funds or passively run funds?

A. Based on a recent study, it appears passively run index funds are winning over actively managed funds, largely due to the lower fees. The study compared the 5-year performance results from June 30 2009 to June 30 2014, in the following categories: Fund Category Actively Managed Index Large-cap 17.3% 18.8% Small-cap 19.8% 22.0% Global 14.3% 15.5% Real Estate 20.1% 23.8% In Part A, we discussed why fixed lifetime income annuity, in Part B, we discussed what is a fixed lifetime income annuity, in Part C, we discussed the four major options of fixed lifetime income annuity payments.

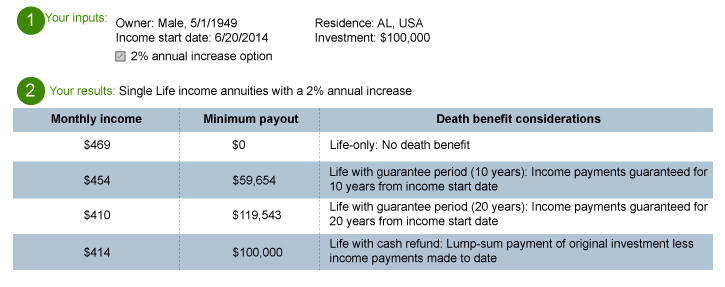

Now, how does Fixed Lifetime Income Annuity fit into your retirement portfolio? Diversification In retirement time, spreading your sources of retirement income across different types of investment products can help you balance your risks and maintain some liquidity and opportunity for potential growth over the long term. A fixed lifetime income annuity can help diversify your retirement income portfolio so a portion of your income is shielded from market volatility. However, your assets allocated to the purchase of fixed income annuities should represent not more than 50% of your liquid net assets, because even though these products provide guaranteed income for life, they also require that you give up liquidity and access to that part of your portfolio. In Part A, we discussed why fixed lifetime income annuity, and in Part B, we discussed what is a fixed lifetime income annuity. Now, the Payment Options and Features of a fixed lifetime income annuity. Fixed lifetime income annuities offer various options that pay different amounts of income, based on the types of guarantees they provide and the date you plan to begin receiving income. The three most common payment options include: 1. Life Only. You’ll receive income payments over either your lifetime alone or the joint lifetimes of you and your spouse (which would decrease the amount of the payment because it would be based on two lifetimes). The “life only” option offers the highest possible income payment because it’s only for as long as you or you and your spouse live; no money goes to your heirs. This option typically works well for those in good health and who anticipate a long life. 2. Life with a Guaranteed Period. You’ll receive income payments for the rest of your life. However, if you pass away before the guarantee period ends, any remaining income payments will continue to your beneficiary(ies) until the end of the guarantee period. Here, you get a somewhat lower payment than life only, because the insurance company is guaranteeing to make payments for a minimum number of years. 3. Life with a Cash Refund. With this option, the priority is ensuring that you never get back less in payments than your original investment. As with many income annuities, you get a lifetime income payment (but typically lower than a life-only option). If you pass away before receiving payments that total your original investment, the remaining value will be paid to your beneficiary(ies). This means, for example, that if you are paid only $10,000 of a $100,000 policy during your lifetime, the remaining $90,000 is paid to your heirs. Annual Increase Feature In addition to different payment options, annuities can include different features. One of the more popular features is an annual increase option. This feature provides for annual increases in the payment amount beginning on the anniversary following your initial payment. The annual increase can be based on a fixed percentage or linked to changes in the Consumer Price Index (CPI). Note that the initial payment amount for an annuity with this option may be lower than an identical annuity without the option. Let’s take a look at how these payment options might differ. Shown below are the actual results for a hypothetical 65-year-old man who invests $100,000 in a lifetime income annuity starting today. We assume he was born on May 1, 1949, and started receiving income on June 20, 2014, with a 2% annual increase. Compare Four Fixed Lifetime Income Annuity Options  In our next post, we will discuss how does Fixed Lifetime Annuity fit into your retirement portfolio.

In Part A, we discussed why do you need lifetime income and fixed lifetime income annuity as a solution.

Now, what is a Fixed Lifetime Income Annuity? A fixed lifetime income annuity represents a contract with an insurance company whose purpose is to convert part of your retirement savings (an amount you choose) into a predictable lifetime income stream. In return for a lump sum investment, the insurance company guarantees to pay you (or you and your spouse) a set rate of income for life. You can also have the option of starting your income immediately or sometime in the future. Having the backing of an insurance company can help mitigate three key retirement risks that, generally, can be very challenging to manage by yourself:

The Trade-off The trade-off with an income annuity is that you must give up control of the portion of the savings you use to purchase one. In return, you don’t have to manage your account to generate income, and you can secure a predictable income that lasts the rest of your life. What’s more, fixed lifetime income annuities are often able to provide higher income payments than other products, such as bonds, CDs, or money market funds, due to the “longevity bonus” they can provide. While the payments from traditional income solutions are limited to return of principal and interest from an investment, fixed lifetime income annuities also make available the ability to share in the longevity benefits of a “mortality pool.” Effectively, assets from annuitants with a shorter life span remain in the mortality pool to support the payouts collected by those with a longer life span. Put simply, the longer you live, the more money you will receive. Part C - What are Fixed Income Annuity's Payments and Features? Part A. Why do you need to create income that can last lifetime?

There are 3 major concerns people face in retirement time: 1. People are living longer 2. Pensions are increasingly rare 3. Market volatility persists Is there a plan that can give you a regular “retirement paycheck” to fund your retirement life and can deal with the above 3 concerns at the same time? The answer is Yes, fixed life income annuity is one such product. In a Nutshell A Fixed Life Income Annuity is just like a traditional pension plan that can provide a guaranteed stream of income that lasts a lifetime and is not vulnerable to the inevitable ups and downs of the market. An added benefit is that by locking in some guaranteed income, you will have more freedom to invest the remainder of your retirement assets for growth potential as part of a diversified income plan. The Best Practice Use an income annuity to cover the portion of essential expenses not covered by other guaranteed income sources like Social Security or a pension. When you know that your essential expenses, your day-to-day needs, are covered for the rest of your life by a guaranteed source of income, you gain the peace of mind and financial confidence to pursue those things you want to do in retirement. Part B - Details of a Fixed Lifetime Income Annuity In our previous blog posts, we showed 3 options for retirees to spend down assets, and the trade-offs of the first two options.

Now we will discuss the RMD-based spend option. First, what is RMD? RMD refers to required minimum distributions, it is the amount that the US government requires you to withdraw annually from traditional IRAs and employer-sponsored retirement plans. The RMD is calculated by dividing the year-end balance by a life expectancy factor listed in IRS publication 590. What is the RMD-based spend strategy? It borrows the RMD calculations by simply dividing your total year-end portfolio balance by the life expectancy factor listed for your age. Some academic studies have shown that the RMD strategy outperformed the spend the interest & dividend and the 4% rule, given a typical retiree's asset allocation. It is responsive to investment returns, and the withdrawal percentages increases with age, allowing retirees to use more of the portfolio as the life expectancy decreases. Drawback of the RMD-spend strategy It may result in withdrawal rates too low, particularly in early retirement time, so you might spend less you should during that time. Also, no rule fits all. A 2010 Vanguard study found that combining a) an immediate inflation-adjusted annuity with b) an RMD approach produced stable cash flows that grew at a faster rate than those of other rules of thumb. Q. Which investments are taxable, tax-free, and tax-deferred?

A. Here is a list for your reference: Taxable investments: checking accounts, saving accounts, CD, brokerage accounts, real estate Tax-free investments: Roth 401k, Roth 403b, Roth IRA, Municipal bond interest, Cash value life insurance Tax-deferred: 401k, 403b, 457 plan, Traditional IRA, Simple/SEP IRA, Annuities, Saving bonds, HSA In our previous blog post, we introduced 3 popular options a retiree to best spend down assets.

The first two options are quite well known, so we will briefly analyze their trade-offs in this blog post. First, the 4% withdrawal option. While this rule of thumb sounds simple to follow, unfortunately it doesn't respond well to the actual asset performances. For example, if the portfolio sinks in a few bad years, withdrawing 4% out of it won't be enough, so you will have to take more out of the assets, the risk of running out of money will be very high. Now, for the use the dividends and interests only option. This option basically scarifies the retiree's life by trying to leave a large sum to the heirs. But the need for income will influence the asset allocation and could lead to not optimal results, for example, the portfolio could be concentrated in a few high risk bank stocks. Recent academic studies more favor the third option - applying the RMD rule to retirement assets. We will discuss it in the RMD-based spend post. Q. How best to spend down my assets in retirement time?

A. This is a question every new retiree asks. Unfortunately there is no set answer that fits all. Generally there are three popular options one can consider: 1) Withdraw 4% of the initial assets, then adjust the dollar amount to keep pace with inflation 2) Spend only the dividends and interests generated by the assets each year 3) Apply the RMD rule to all the assets each year We will use a few blog posts to discuss the three options' pros and cons. Q. I have had a great performance this year. Should I let my profit run instead of rebalancing my portfolio?

A. Rebalancing means buy low and sell high, which most investors fail to do so, think about it as a disciplined approach to investment, with the main purpose to maintain a portfolio that is consistent with your original target. When you let profit run, you are increasing your risk of falling. Think about a target portfolio 50/50, when you let the winners keep running, soon you might see your portfolio becomes 40/60, 30/70, ... in other words, it gets increasingly concentrated in a few winners, and deviates from your target portfolio structure. We all know what happens for a 10/90 portfolio in 2008. In our last blog post, we discussed the importance to insurer your cash flow.

The key here is to understand what we need to protect, and that requires us to know what we’re spending. Disability Insurance - How much? For a household making $100,000, saving 20%, paying taxes with 30% and spending 50%, they would need to replace about $50,000 annually if they were to have their primary bread-winner be disabled and unable to work for a significant period of time. To simplify this process, most individual disability policies will replace 60% of your income. If it’s an individually owned policy and you are paying the premiums with after-tax dollars, then the monthly benefit comes to you tax-free, so the monthly budget is now protected. That is a simple example and the reality is disability policies can be very complex. It’s important to consult an independent insurance advisor who is licensed with different insurance carriers, and is able to present and explain the many different intricacies of each contract. Life Insurance - How much? Life insurance is not too different. The goal is to provide financial means in the event of loss of a wage earner. There are two common ways to decide how much insurance to put in place; one is income replacement, and the other is liability pay down. While there is no right or wrong way to go about putting coverage in place, we’re going to focus on income replacement. In a similar exercise as discussed before, it’s important to decide how much monthly cash flow needs to be replaced. Using the example above, let’s say we want to replace $50,000 per year. What amount of insurance would we need to be in-force to safely generate the cash flow back into the household? Using a 5% rate of return, which over a long period of time is reasonable for a balanced portfolio, we would need to put $1 million dollars of insurance in place. Similar to the tax treatment of disability insurance, life insurance proceeds are generally paid to the beneficiaries free of federal and state tax. The reality is simple. Insurance, when used properly, is a very powerful financial tool. The issue is, the way insurance is bought and sold. Insurance companies pay their agents’ commissions for selling their policies. Inherently there is nothing wrong with this, however this compensation structure can often drive an agent to be “pushy” and “over sell” the consumer which creates a frustrating and negative experience. Remember, though, not all agents are created equal, and it’s important to develop a relationship with someone you trust. Someone who will shoot you straight, explain the pros and cons of various policies and present you with several options from which you as the consumer can choose between. As an independent firm, PFwise is that special someone, we can find the best insurance product for you! Please feel free to contact us with any question on your mind. Insurance is the financial product you don’t need until you do. Unfortunately all insurance companies know this, so they go to great lengths to properly protect themselves. Well, so should we! Let’s be honest, nobody likes to discuss the possibility (or probability) of bad things happening but we all know they do. We also know that nobody likes to deal with insurance companies. Whatever the case may be, there always seems to be a “loophole” where they get off the hook. However, they are legally and contractually bound to the provisions outlined in the contract as long as you (the policy holder) hold up your end of the bargain…which generally just entails paying your premiums on time.

In the most basic of terms, we buy insurance to protect things of great value. It’s important to be educated on the topic and knowledgeable of what your policy stipulates. You can buy insurance for just about anything…cars, homes, income, TVs, the Vegas dealer drawing Blackjack…the list goes on and on. Let’s start with some insurance basics. To simplify as much as possible, there are a few key items and definitions to be familiar with: Premium – What you pay for the insurance coverage. Coverage Amounts – What the insurance company is on the hook for after your deductible has been satisfied. Coverage Term - How long the contractual relationship between you and the insurance company lasts. In general their relationship to one another is as follows: The higher the coverage amount, the higher the premium and vice versa. The longer the coverage term, the higher the premium and vice versa. Okay, so now that you know the basic principles of insurance, where do we go from here? Let’s look at some of your most valuable possessions; car, house, baseball cards, grandfather’s watch, golf clubs, Mac Book? All of these are valuable and can be insured, but arguably the most valuable possession you have is your ability to generate an income, which can be insured in a couple of ways. So how do we prioritize where we devote our protection dollars? Of course we all know that cash flow is king. From bills to savings to vacation money, it all hinges on generating cash flow. Undoubtedly, the most devastating loss to a household is the loss of income, either due to death or disability of the primary wage earner. Consider this: 70% of U.S. households with children under 18 would have trouble meeting everyday living expenses within a few months if a primary wage earner were to die today. 40% of U.S. households with children under 18 say they would immediately have trouble meeting everyday living expenses. With those startling figures one would assume that, given its significance, income would be protected with insurance. However, less than 45% of individuals owned life insurance, and less than 40% owned disability insurance. On top of this, there’s a good chance that even the ones who are insuring their income, are most likely under-insuring. Now, how do we go about putting this protection in place? Please read our next blog post. Q. I have a student loan needs to pay back, want to buy a house as soon as possible, and also want to save for retirement as early as possible. How should I prioritize them?

A. Of the three, saving for retirement should be your number 1 goal, unless you have a student loan with a very high interest rate. The right way to prioritize these three saving goals is: a. Retirement saving first Save a minimum amount of 401K to at least get your employer's match. If you can set aside 10%, that will be better. b. Budget for student loan payment Estimate how much student loan you need to pay back each month. While you want to pay back all of the student loans asap, but it's more important to develop a pay back plan that factors in your other saving goals. c. Prepare a rainy day fund Save a few months' emergency fund that can last at least 3 months. d. Save for down payment Start saving for your down payment, aim for 20% down payment saving, plus closing costs. What's the next thing you will do?

Is it the most important thing? Or just the easiest thing? Or maybe the most urgent thing? Did you ever spend time thinking what's the most important thing to do next? Q. What can I do in a short period of time to improve my credit score?

A. There are many factors that influence your credit score, but there is only one factor that is truly under the control of you - your Credit Utilization Rate. Credit Utilization rate is calculated with total amount of credit used divided by total amount of credit allowed. Here are 4 tips you can use to improve your credit score, they are all related to improving your credit utilization rate:

Q. My 401k plan has many fund options, how to pick the right funds for my 401k plan?

A. Compared with some plans with very limited choices, it's a nice problem to have when you have too many choices in your 401k or 403b plan. There are two decisions you need to make in order to pick the right funds: a. Determine your risk tolerance level In stock market, risk and reward always go together. The higher the potential reward, the higher the potential risk. This means that historically, stocks funds have the record to delivering higher average return over time, but also have frequent, sudden, and sometimes huge declines. Short-term or intermediate-term bonds and money market funds are stable, in both return and risk. Your first task is to determine what kind of balance you want to achieve in your portfolio that fits your risk tolerance level. We have developed an online tool to help you assess your risk tolerance level. b. Decide which funds to pick Once you know how much weight you want to give to stock funds and bond funds, your next step is to pick the best available funds in each category. The principle is to pick low cost index funds with broad market exposures, because nobody has the crystal ball to tell you which sectors of the market will go up or down next. Over the long term, when the market goes up, you will grow with it. Remember, most actively managed funds can not even beat the market. Q. Does pregnancy negatively affect my life insurance application?

A. Pregnancy itself is not a problem for most insurance carriers, as long as there are no complications now or in previous pregnancies. However, during the medical exam, you will be taken at your current height and weight, which might or might not be a problem. Q. I want to improve my child's chance of getting financial aid, will HELOC help?

A. Not likely. If you open a HELOC but don't use it, it won't matter at all for FAFAA. If you actually take money out of HELOC but not using it (e.g. put into a bank account), it will increase your reportable assets and hurt your chance of getting financial aid. In one scenario a HELOC might help, that is you have a sizable saving balance, it will be your assets and hurt the financial aid chance. You can use that asset to pay down mortgage, then open a HELOC for emergency use. This will help your chance of getting financial aid, but of course comes with risks if your home value decreases, you lose your job, etc. Q. Is there a rule of thumb I could use to determine how much do I need to retire?

A. Yes, the rule of thumb is you need 25 times of the amount you need to spend in your retirement time. For example, you figured out you will need $100,000 per year to live a comfortable retirement life. Your annual social security income is $60,000. So you will need 25*$40,000 = $1,000,000 to retire. In other words, you can withdraw 4% per year from it to support your retirement life without incurring the risk of running out of money when you are still alive. Q. What are the ways for me to save on college textbook expenses?

A. The College Board estimates each year a college student spends around $1,200 on textbooks. Here are some good ways to save on college textbook expenses: Shop around BigWords.com: compare all the textbook stores all at once Rent Textbooks Chegg.com eCampus.com Bookbyte.com BookRenter.com CampusBookRentals.com Download Textbooks OpenStaxCollegecom: free download books in PDF format Buy Second Hand Textbooks Amazon: save up to 90% Barnesandnoble.com Half.com AbeBooks.com CengageBrain.com Sell Used Textbooks Valorbooks.com: a guide to sell used textbooks Amazon: a few books to guide you how to profit from selling textbooks Q. Other than tuition, room and board expenses, what else I need to budget for my child's college expenses?

A. There are many hidden costs of college! Other than tuition, room and board, here are some other expenses to budget for:

Q. I'm in early 40's and want to know the best way to plan my retirement, do you have any book to recommend?

A. Yes, currently the #1 best selling retirement planning book at Amazon is "The Charles Schwab Guide to Finances After Fifty: Answers to Your Most Important Questions". This books is not just for people over 50, it is for everyone. It starts with the top 10 financial recommendations for every age. Part one of the book addresses people who are at least 10 years from retiring. The second part addresses questions people likely to ask when get closer to retirement. What makes this book outstanding is it's written and organized in the Q&A format, you will surely find some retirement questions you may not even have known you should ask, here they are, with easy to understand answers. In this Estate Planning 101 series, we have discussed Wills, Living Will and Healthcare Power of Attorney, Financial Power of Attorney, now the last part - Trust.

Trust What is it: A trust is a legal entity that can own your assets (while living or at death) and be controlled based on your wishes outlined in the legal document that created the entity. For example, a trust might be useful if your 2-year-old daughter survived you and your spouse and was now the rightful owner of all your assets (house, bank accounts, retirement accounts, insurance proceeds, etc.). A trust would allow you to dictate how you wanted your child to benefit from your assets throughout her life. It is a way to protect assets from being used in a way that you would not see fit if you were in control of them. When to get it: You only need this if you are worried about the oversight or care of the assets that may be provided at your passing. Ultimately, you are trusting your heirs to manage and use your assets properly should you pass away. If you have a sizeable insurance policy or estate and/or children a trust is worth discussing with an attorney. Where to get: Do not do generic trusts online. Talk to an attorney to determine the right parameters and language for your situation. How much: $500-$800 per trust created. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed