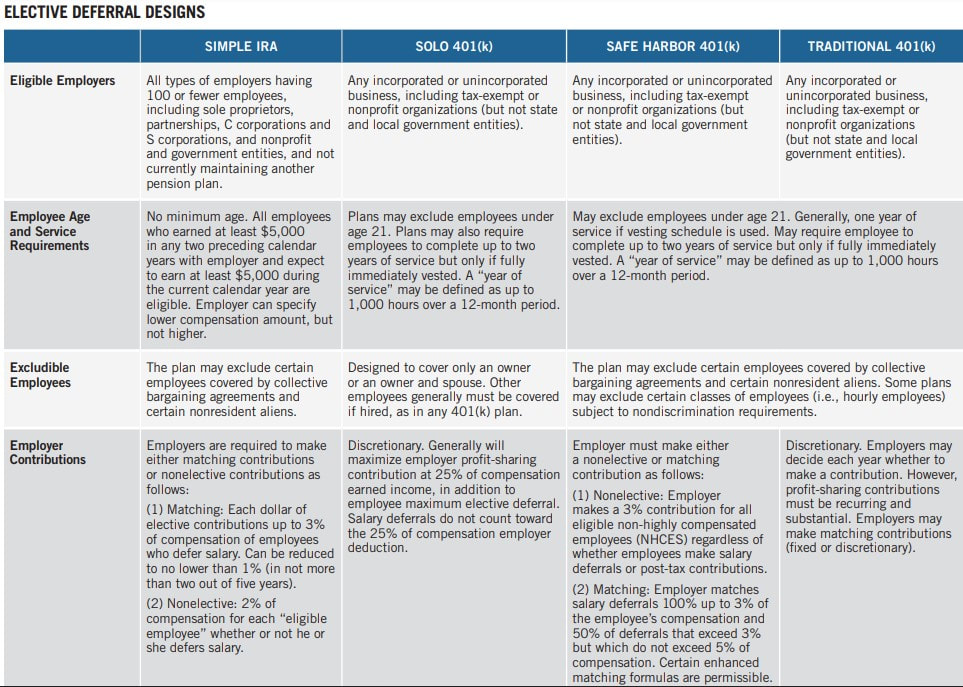

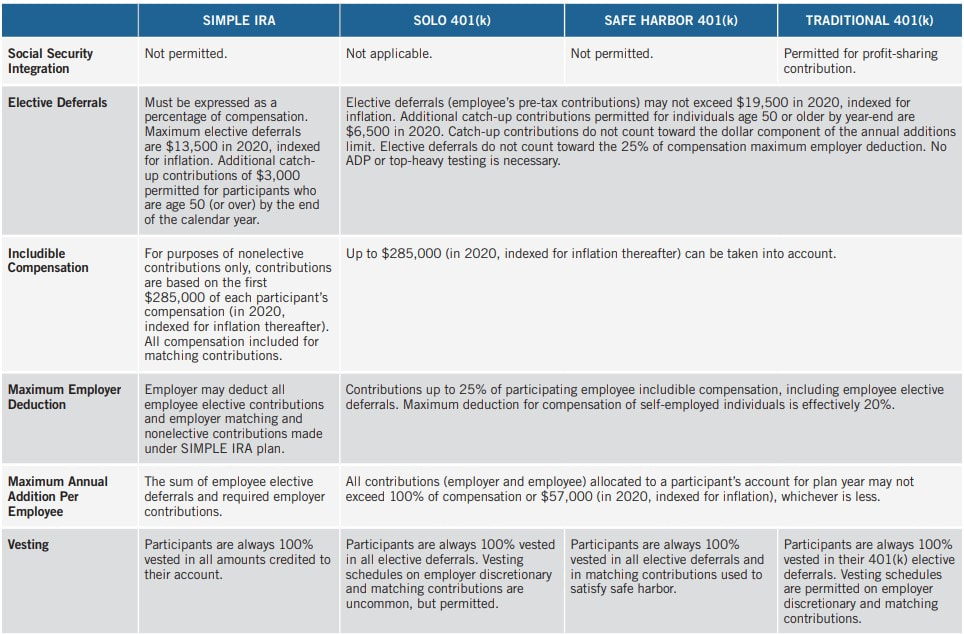

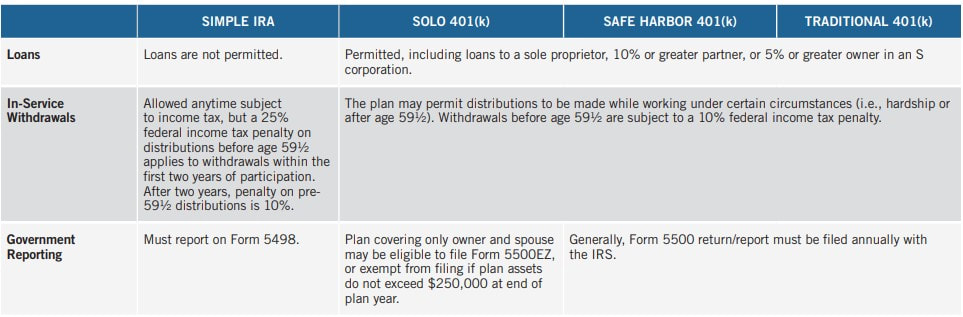

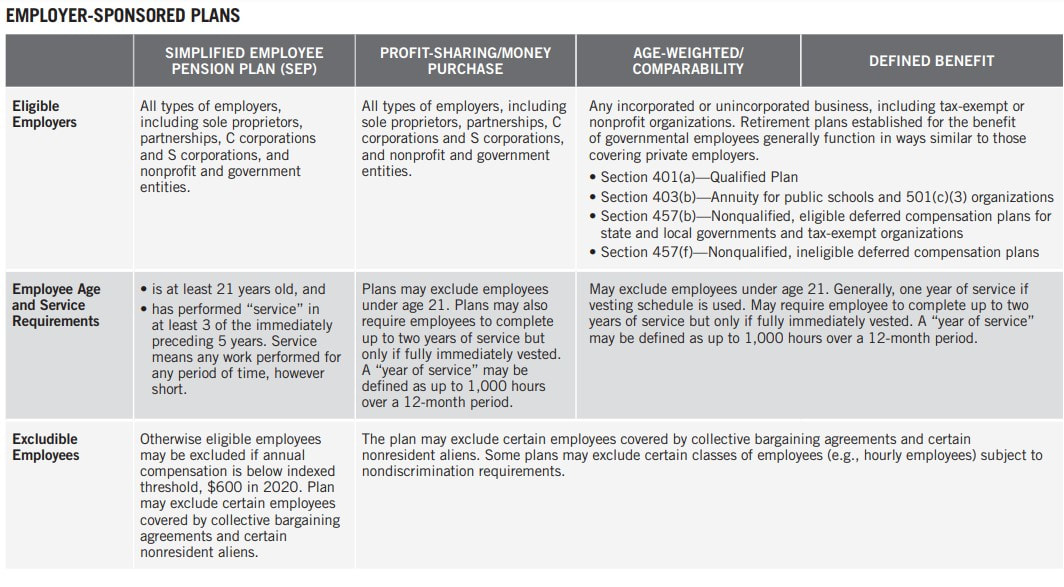

In last blogpost, we discussed employer-sponsored plans for business owners. Now we will discuss Elective Deferral Designs.

|

|

|

In last blogpost, we discussed employer-sponsored plans for business owners. Now we will discuss Elective Deferral Designs.

0 Comments

In next blogpost, we will compare ELECTIVE DEFERRAL DESIGNS.

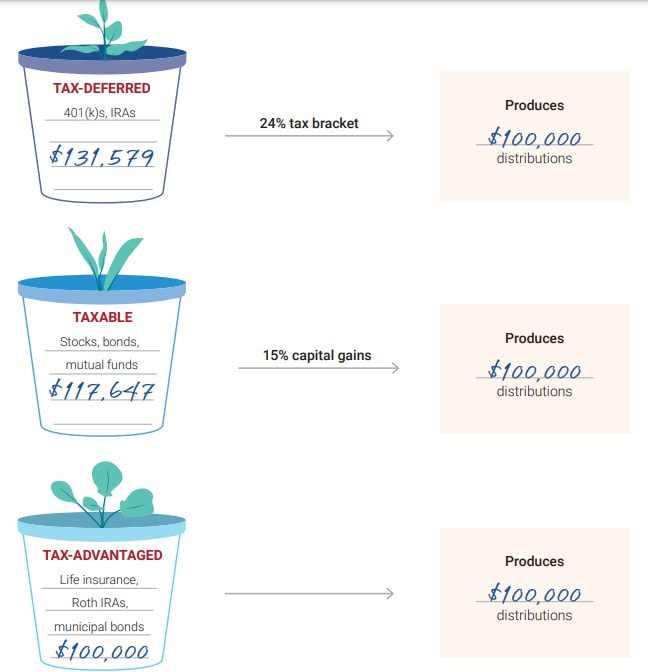

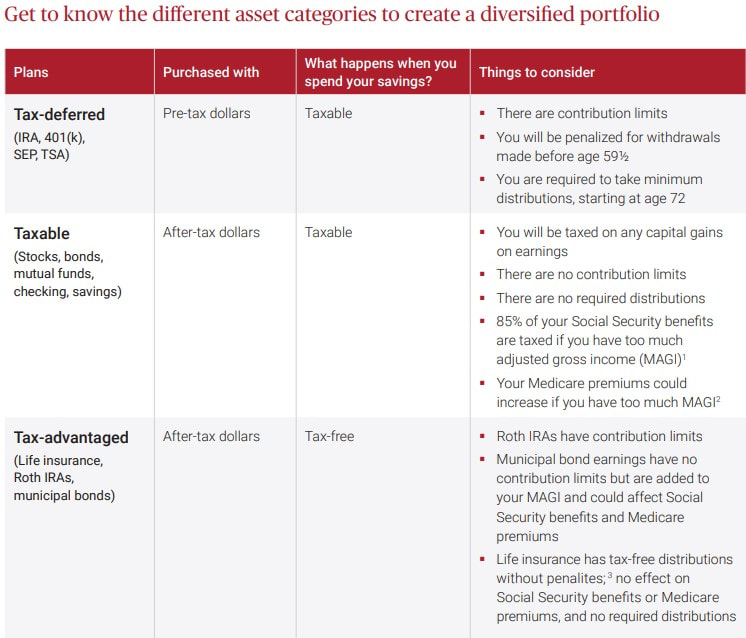

As you plant the seeds for retirement, now is the time to consider how taxes will affect you when you begin spending your savings. The following illustration will help you understand how taxes affect your retirement plan and how to diversify assets, so you can keep more income and pay less in taxes when you begin distributions. As you understand how taxes impact the money you use to invest in the different options and how taxes impact your distributions, you will see that diversification is not only important for growth but distribution.   In last blogpost, we discussed Conduit trust. Now we will discuss Accumulation trust.

With an accumulation trust, the trustee has broad discretionary authority to either pay out or accumulate retirement plan distributions during the lifetime of the primary beneficiary for possible distribution to another beneficiary, at a later date. However, after SECURE, even an accumulation trust isn’t the perfect solution. It has its tradeoffs. An accumulation trust may resolve someone's concerns about the beneficiary receiving too much too quickly, but at a prohibitively expensive income tax hit. SECURE requires that all retirement benefits be paid to the accumulation trust within 10 years, following the year of the death. To the extent the trustee accumulates retirement plan benefits in the trust, they will be taxed at the highest trust rates due to its compressed tax brackets. Yet, a strategy that combines an accumulation trust with the purchase of a life insurance policy may be the right solution to help offset the accelerated tax liability with an income-tax free death benefit at the death. Aimed at increasing access to tax-advantaged accounts and preventing older Americans from outliving their assets, the Setting Every Community Up for Retirement Enhancement Act (SECURE Act) is far-reaching retirement savings legislation that took effect in January. One significant provision eliminated stretch IRAs as an estate planning tool by requiring full distribution of an IRA to beneficiaries within 10 years, following the year of the employee or IRA owner’s death. Now is the time to identify new options to pass legacy to beneficiaries without also passing a big tax bill.

Conduit trust The new legislation may be most problematic for people with conduit trusts because the conduit trust will no longer operate the way originally expected it to work. Under a conduit trust, the trustee immediately pays all retirement plan distributions to the primary or lifetime trust beneficiary (“conduit” beneficiary). All retirement plan distributions paid to the trust are forced out to the conduit beneficiary and nothing accumulates in the trust. Historically, conduit trusts regulated and controlled the systematic and gradual payout of someone's sizeable retirement plan over the beneficiary’s lifetime. They were used to address the fears regarding the beneficiary’s potentially questionable financial judgment, discipline and restraint as well as concerns about creditors’ and other claimants’ (ex-spouses) attempts to access those assets, if otherwise, left outright the beneficiary. SECURE mandates the trustee accelerate distributions under the 10-year payout rule to the conduit beneficiary rather than make small incremental distributions over the beneficiary’s lifetime unless the beneficiary is an “eligible designated beneficiary” (EDB). An EDB is a surviving spouse, a disabled or chronically ill individual, minor child of client, or an individual who is not more than 10 years younger than the client. As a result, SECURE may expose a conduit beneficiary to an increased income tax burden and undermine the intent, purpose and utility of the trust if the designated beneficiary is not an EDB. At a minimum, people should have their conduit trusts reviewed and either modified to name an EDB, if appropriate for their circumstances, or potentially switch to an accumulation trust. In next blogpost, we will discuss Accumulation trust. Wealthy clients should invest more in private equity, a study says. Read the article from Financial-Planning.com if you are interested in this topic.

One of the major fears your clients face is outliving their income. A Palladium® Single Premium Immediate Annuity (SPIA) could help you shield you from this risk . SPIA allows a lump sum to be converted into a steady stream of guaranteed annuity payments, providing a guaranteed income for as long as it's needed. These 5 Internal Revenue Tax Code sections put the power of life insurance to work helping you reach your financial goals:  United States

Many families use 529 plans as a way to save for future education costs due to its tax benefits, as funds in a 529 account grow tax-deferred, and that growth can subsequently be withdrawn tax-free if used for qualifying educational expenses. In addition, many states offer a tax deduction for 529 plan contributions, making these accounts even more attractive.

And while many families might not have the means to contribute more than the annual gift tax limits ($16,000 per individual, per recipient, in 2022), wealthier families have the option of ‘superfunding’ these accounts beyond this limit without using their gift tax exemption. The superfunding exception allows individuals to fund up to five years’ worth of 529 contributions to a given beneficiary in a single year, without triggering gift taxes when the contribution is made to the child’s 529 plan. For example, a parent could contribute $80,000 into a 529 for their child in 2022, and not have to use any of their gift tax exemption… as long as they do not make additional gifts to that child for five years. Given the additional years of potential compounding (with tax-free growth potential), superfunding a 529 could lead to a larger account balance by the time the student goes to college compared to making smaller annual contributions. At the same time, there are limits on how much someone might want to contribute to a 529 account. For example, because of the limited tax-free uses of funds in a 529, a parent or other contributor might not want to ‘overfund’ an account beyond what the account’s beneficiary is likely to need for college or graduate school expenses (especially if the parent has other financial priorities of their own!). On the other hand, the parent can choose to fund more and plan to change the beneficiary to a sibling or another individual who will have education expenses. And some families might even consider contributing so much into 529 accounts that it funds not only college for their children, but has enough left over to benefit further generations down the line. These ‘Dynasty 529’ plans have the potential benefit of perpetual tax-free growth, but come with several potential pitfalls to navigate (e.g., gift tax and Generation-Skipping Transfer Tax implications, as well as the possibility that a future beneficiary will use the funds for something other than education and pay the associated taxes and penalties). First introduced in the 1970s, index funds have grown in popularity over time thanks to their ability to provide broad-based diversification at (typically) very low costs, making their benefits available to investors of any level of wealth. And while mutual funds and Exchange-Traded Funds (ETFs) have been the dominant way for investors to get index exposure, thanks to improved technological capabilities and reduced trading costs, direct indexing – buying the individual component stocks within an index – has emerged as an alternative tool with a range of potential use cases.

Historically, direct indexing was developed as a means to unlock the tax losses of individual stocks in an index – even if the index itself was up – and was primarily used only by the most affluent investors (who had the highest tax rates and benefitted the most from the available loss harvesting). However, direct indexing can be used not only to harvest tax losses but also to harvest capital gains (particularly for those taxpayers in the 10% and 12% tax brackets). In addition, direct indexing can provide tax benefits to investors who are charitably inclined by allowing them to donate the underlying shares within an index that have the largest gains, thereby helping them to maximize their tax savings. For those whose primary goal is to benefit from a more personalized indexing strategy that still gains broad market exposure while specifically adjusting for personal preferences, using a personalized index can ensure the investor’s capital will support the exact industries or companies they wish to support (while also saving on the management fees otherwise charged by more packaged ESG/SRI mutual funds and ETFs). This article from Kitches.com discusses in great details of 4 types of direct indexing -

Attached here is a case study from AIG on the new Lifetime Income Choice’s Max Income Option. Max Income Option Provides:

Fidelity provides a valuable service for its customer - the Equity Summary Score for most of the large cap stocks, and many smaller cap stocks. Below is a high level description, more detailed description in the attached document below. The Equity Summary Score provides a consolidated view of the ratings from a number of independent research providers on Fidelity.com. Historically, the maximum number of providers has been between 10 and 12. However, some stocks are not rated by all research providers. Since the model uses a number of ratings to arrive at an Equity Summary Score, only stocks that have four or more firms rating them have an Equity Summary Score. It uses the providers’ relative, historical, recommendation performance along with other factors to give you an aggregate, historical accuracy‐weighted indication of the independent research firms’ stock sentiment. Principal® market research shows business owners rank income protection as their #3 priority for business solutions, yet only 42% have disability income insurance.

Helping business owners get the income protection they need can be easy with Principal's 3-3-3 program. With this program, business owners can get pre-approved for a 3A occupation class quote when they meet these simple eligibility guidelines: • 3+ years as owner of their business • 3+ employees (in addition to themselves) or sub-contract manual labor • $30,000+ net income in each of the previous two years Here is how this program works:

The American National Signature IUL is a good insurance product with multiple benefits:

Momentum has been building for several years, driven in large part by increasing demand for EVs like Tesla's (TSLA) Model 3 (the top-selling EV worldwide in 2021) and Model Y, Wuling Motors' (WLMTF) Mini EV, Volkswagen's (VLKAF) ID.4, BYD's (BYDDY) Qin Plus DM, Ford's (F) Mustang Mach-E, General Motors' (GM) Bolt, and Nissan's (NSANF) Leaf.

Here are the 10 largest automakers by market cap who produce only electric vehicles:

In last blogpost ,we showed 4 insurance options to protect against chronic illnesses.  Being chronically ill means you’re unable to perform at least two of the Activities of Daily Living (eating, bathing, etc.) for at least 90 days; or you suffer from a severe cognitive impairment. Here’s a quick snapshot of four common insurance options that people may consider for financial protection in the event of a chronic illness.  In next blogpost, we will compare the pros and cons of each option. The following AIG flyer shows a scenario where one could use a combination of Term and GUL to protect from both pre- and post-retirement risks! The US Index of Leading Indicators is a composite of 10 indicators ranging from measuring unemployment to stock market performance. Proponents of this index believe that it captures a wide dispersion of information and can help forecast shifts in the economy. After rapidly plunging into negative territory in the wake of the spread of COVID-19 around the globe, this index took roughly a year to rebound to a positive reading—and actually surged to a multidecade high in 2021, reflecting the economic reopening. Over the past several months, it has begun to recede from those peak levels, but has been strongly positive and near historically high levels.  In The 2022 Policygenius Life Insurance Trend Report, 3 trends are noted.

Growth in no-medical-exam life insurance The COVID-19 pandemic has accelerated changes in consumer shopping habits, with shoppers demanding convenience and more no-medical-exam policies that allow consumers to apply for term life insurance using digital health information. According to Kartik Sakthivel, vice president and chief information officer at LIMRA, nine in 10 insurance executives surveyed in 2020 reported that their customers “have an increased appetite for the digital shopping experience,” a trend that continued into 2021. Internal Policygenius data corroborates this trend. From October to December 2021, roughly 56% of life insurance applications submitted through Policygenius were for no-medical-exam policies, compared to 26% in January to March 2021. In addition to providing convenience, accelerated underwriting policies can be more affordable options for shoppers. Policygenius Life Insurance Price Index data from the last year shows that no-medical-exam term insurance policies are competitively priced compared to term policies requiring a full medical exam — and some applicants even paid less for no-medical-exam term coverage. For example, 25-year-old females buying $250,000 in coverage paid 1.6% less in 2021 for no-medical-exam term policies than they did for traditional policies. Strong demand from younger age groups According to Mark Friedlander, director of corporate communications at the Insurance Information Institute, 2020 life insurance sales “were largely driven by younger age groups” and there was a year-over-year increase of 7.9% in life insurance sales for policyholders 44 and under from 2019 to 2020, the last year for which he has complete data. In terms of the amount of coverage purchased through Policygenius in 2021, people 18-44 bought the vast majority (84%) of policies exceeding $1 million in coverage, and 81% of policies from $750,001 to $1 million. Older Gen Xers and Baby Boomers — people age 45 to 64 — bought only 16% of policies over $1 million in coverage, and those 65 and up didn’t buy any of these policies. Compared to other demographics, Gen Xers and Baby Boomers also bought less coverage overall through Policygenius in 2021: 85% of policies bought by people over 65 and 87% of the policies bought by people age 45 to 64 were for under $250,000. Stability in life insurance pricing The life insurance industry saw a significant increase in death claims due to COVID-19 in 2020. “Death benefits paid in 2020 jumped to $87.5 billion, up 15% from $76 billion in 2019, the largest increase in nearly 25 years,” according to Friedlander. One carrier on the Policygenius platform saw a similar rise in death claims in 2020 — and an even bigger increase in 2021. Legal & General America, the parent organization of the Banner Life and William Penn life insurance companies, saw a 12% increase in death claims, measured by dollars paid, from 2019 to 2020. Death claims rose again last year, increasing 17% from 2020 to 2021. Despite this increase, as well as inflation, life insurance prices stayed consistent throughout 2021, with only nominal changes. Based on Policygenius data from April 2020 to April 2021, older smokers saw a surge in life insurance pricing, but pricing adjustments in May 2021 and the following months brought prices back to April 2020 levels. Consumers will likely continue to see price stability as insurers gather long-term data on COVID-19’s impact on mortality rates. If you had a withdrawal from your Virginia529 account(s) during 2021, a 1099-Q form was issued for tax purposes.

If a withdrawal was made payable to an account owner, a 1099-Q will be mailed to the account owner and is available online at Virginia529.com. Simply log in to your account, locate the “View My Account” tab, and select “Tax Information (1099-Q Form)” from the dropdown menu. If a withdrawal was made directly to the student beneficiary, to a K-12 school or eligible educational institution, the student will receive the Form 1099-Q in the mail. Students can log in to their Virginia529 account to review a digital copy or create a login ID if they do not already have account access. It's important to note that the account owner will not be able to view this document. Reporting 1099-Q Amounts on Your Tax Return Virginia529 is required to report withdrawals to the IRS with Form 1099-Q. Qualified education expenses include tuition, fees, books, computers and related technology, and some room and board costs for students attending an eligible college or university. Families can also take a tax-free withdrawal to pay for tuition expenses at private, public and religious elementary and high schools. This amount is limited to $10,000 per year, per student. The SECURE Act of 2019 expanded the definition of qualified 529 plan expenses to include costs of apprenticeship programs and qualified student loan repayments. Qualified distributions for student loan repayments have a lifetime limit of $10,000 per beneficiary and each of their siblings. 529 withdrawals spent on other purchases, such as transportation costs or health insurance coverage are generally considered non-qualified. If the withdrawal(s) taken on your account did not exceed the total amount of 2021 qualified higher education expenses incurred, you should not need to report the withdrawal(s) on your tax return. If, however, the withdrawal(s) exceeded your total qualified higher education expenses, consult a tax professional for more information as you may have income tax consequences. Reporting Contributions on Your Tax Return If you’ve simply been contributing to an existing 529 account you may not have to report anything on your federal income tax return. Contributions to a 529 plan are not deductible and therefore do not have to be reported on federal income tax returns. What’s more, the investment earnings in your account are not reportable until the year they are withdrawn. As for state income tax filings, Virginia529 account owners who are Virginia taxpayers may deduct contributions up to $4,000 per account per year with an unlimited carryforward to future tax years, subject to certain restrictions. Those account owners who are Virginia taxpayers age 70 and above may deduct the entire amount contributed to their Virginia529 account in one year. In addition, contributions to Virginia529 accounts are treated as a completed gift by the account owner to the student beneficiary. This means contributions up to $16,000 a year, or up to $32,000 if married, may be gift tax free. You should consult your tax advisor regarding the specific tax consequences of contributions. If you’re expecting a tax refund check this year, consider transforming it into a contribution toward your Vigrinia529 account. Tax season is upon us, but before you file, take the time to help make sure you’re not paying more than you owe. If you’re among the Americans who typically only take the standard IRS deductions instead of itemizing on your 1040, you may be missing out on some money-saving tax deductions or credits that you’re eligible for. Keep these three factors in mind that may help you save.

Charitable contributions You already know that you can deduct donations of money or goods, but most taxpayers often don't deduct enough. That's because many of us fail to keep detailed records tracking our donations throughout the year. Whether you dropped off a bag of clothing at a local charity or donated $5 at the register of your grocery store, you should be tracking all of these contributions to ensure that you get the highest tax benefit. If you didn't track this last year, sit down now and do your best to account for as much as possible. And don't forget, you may be able to include transportation costs in service to a charitable organization (like dropping off those donations or getting to and from a charity event or volunteer day). Then pay closer attention to donations this year. Reinvested dividends Reinvested dividends in a taxable investment account are treated as current income, the same as though you received them in cash. Qualified dividends, which are those held for a specific time, are taxed at a lower capital-gains tax rate (visit irs.gov to find out what qualifies as a dividend). This isn't exactly a deduction, but you may be able to cut down on your tax bill through good record keeping. When reinvesting dividends, add this amount to your basis in the security. By tracking the basis, you can reduce your capital-gains tax if you sell the security at a higher price. Earned income tax credit The Earned Income Tax Credit (EITC), designed to supplement wages for low-to-moderate income workers, may or may not be on your radar. Although tens of millions of people previously classified as “middle class” — including traditional white-collar workers — now fall into the “low income” bracket because they lost a job, took a pay cut, or worked fewer hours during the year. Given the interruptions and changes in employment affecting millions of workers from the widespread efforts to help control the pandemic, it may be worth talking to your tax advisor to see if you’re eligible this year. Tax-advantaged product solutions can help clients save more for retirement and potentially grow their savings faster. Most clients may be familiar with 401(k)s and IRAs, but there's another tax-advantaged vehicle to consider for retirement planning: fixed indexed annuities (FIAs).

FIAs are insurance products that offer growth potential and guaranteed income for retirement. Funds in an FIA earn interest credits based in part on the upward movement, if any, of a reference stock market index, such as the S&P 500®. Since money in an FIA is not directly exposed to stock market risk, FIAs also provide protection from loss due to market downturns. What's more, this combination of growth potential and protection comes with tax advantages that can complement other savings and investment vehicles in your clients' retirement portfolios. Here is a look at three key tax benefits of FIAs and how they can contribute to a tax-smart approach to retirement planning.

The big picture With their tax benefits and ability to provide growth potential and protection, FIAs can play an important role managing taxes within a retirement savings plan. They may complement other sources of growth potential and retirement income, including stocks, bonds and mutual funds held in taxable brokerage accounts; savings in tax-deferred accounts like 401(k)s; and other tax-advantaged vehicles such as Roth IRAs. Using a mix of these tools can be vital to helping clients minimize the effect of taxes, manage risk and provide growth potential before and after retirement. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed