|

Q. When may rollover contributions be made from an IRA to a tax-sheltered annuity?

A. An individual may receive a distribution from his or her traditional IRA and within 60 days roll it over into a tax-sheltered annuity to the extent that the distribution would be includable in income if not rolled over. After-tax contributions, including nondeductible contributions to a traditional IRA, may not be rolled over from a traditional IRA into a Section 403(b) tax-sheltered annuity. Q. May an individual who has turned 70½ make a rollover?

A. Yes. The Secure Act now permits taxpayers to make contributions to traditional IRAs at any age. Although there was considerable confusion on this issue at one time, it now seems clear that rollovers may be made to traditional IRAs as long as the minimum distribution requirements are met. Rollovers, as well as contributions, may be made to Roth IRAs by individuals at any age. It appears that the same rationale also permits rollovers to qualified plans and Section 403(b) tax-sheltered annuities after age 72 if minimum distribution requirements are met. Sizing up your retirement readiness can be simplified. Just use the following list to evaluate your expected expense -  What Do Medicare and Medicaid Cover?

Both programs generally help people with improving or correcting specific medical or health problems, but not with day-to-day custodial care, or what are known as Activities of Daily Living (ADLs). Medicare will only cover rehabilitative care following a hospital stay which limits the availability of benefits. On the other hand, Medicaid is a program for individuals with limited resources and income which means most people won’t qualify for these benefits. So, if you eventually need help with ADLs like eating, bathing, getting dressed, getting around or personal hygiene, those services wouldn’t be covered by Medicare or Medicaid. You would need private long-term care insurance to help pay for that. Advantages of a private LTCi policy over Medicare and Medicaid

If you are healthy at age 65, Medicare Advantage (MA) may look like the better deal with lower upfront monthly costs than Original Medicare. However, you need to consider two important factors before making your final decision:

1. Original Medicare offers access to all of the doctors anywhere in the country who accept Medicare (most do), while most MA plans have only limited regional network of doctors and facilities (much like an HMO). 2. If you enroll in MA then become ill, in the majority of states you likely won't be able to switch back to Original Medicare, that's because it's imperative to add a supplemental private insurance policy to Original Medicare (Medigap) to cover expenses that Medicare does not pick up, and there is only one window - when you first sign up for Medicare - for getting a Medigap policy that covers any preexisting conditions and doesn't charge you extra for the coverage. There are four retirement strategies: total return, risk wrap, time segmentation and protected income.

In this article from ThinkAdvisor.com, professor Wade Pfau, also director of the Retirement Income Certified Professional program at The American College of Financial Services discusses these strategies and why Annuities deserve an equal seat at the table with any other retirement income strategy. For many people that are considering a $1MM ticket, they plan on spending some of their portfolio above and beyond what Social Security, their pension and annuity purchase will provide. The first step in becoming income savvy is to complete your Income Planning Worksheet, this will help assist you in considering your retirement income needs. In last blogpost, we discussed Same-sex couples.

Multigenerational families In a multigenerational family, two middle-aged adults might find that their dependents include not just children, but also an aging or disabled parent. Financial hurdles for multigenerational families include loss of income and retirement assets due to providing assistance to a parent. When you have an aging parent living with you, just the normal day-to-day living costs can start to add up, which can affect the couple’s cash flow and savings. While any income the parent receives can help offset the additional living costs, often that income is used to pay for medical and health care expenses for that parent. Further, that parent may need around-the-clock assistance at some point, which will put further stress on the family. Considering paying for full-time care is extremely expensive. Some families have elected to have one spouse stay at home and be the caregiver. The decision to quit your job to stay at home with Mom or Dad has an impact on your current financial situation and a lasting impact on your future retirement. Leaving work means losing not just current income but also future Social Security or pension income, as well as employer benefits such as health insurance and 401(k) contributions. If you do not take care of your own physical, mental, and financial health, then ultimately no one will benefit from this arrangement. In last blogpost, we discussed Single person, living alone, with no children.

Same-sex couples Thanks to the Supreme Court decision legalizing same-sex marriage nationwide on June 26, 2015, same-sex couples now face simpler financial planning that makes it easier to jointly own assets, inherit assets, and file taxes. Their notion of a dependent is no longer unique. Nonetheless, establishing trusts and making an estate plan provide extra protection through clear legal documentation, especially in states that are still fighting against the law. And same-sex couples that consist of two high-earning professionals may need extra help investing their money wisely. What else is still different about financial planning for same-sex couples? Because they are not guided by the traditional relationship mores, they have to make big decisions about how intertwined they want to be with one another from a financial perspective. Even life partners can have a hard time comingling their finances because some people are very protective about their money. One partner might want to plan as if their money is one, and the other might want to approach assets as being individually owned. One of the most common pieces of advice is that aren’t married is to consider marriage for the sake of love, and nothing else. When finances become a part of the marriage decision-making factor, it almost never works. In fact, if love wasn’t a part of marriage, the advice would generally be to stay unmarried for the sake of finances. Managing individual investment portfolios simplifies tax implications, investment decisions, income distributions, et cetera. In next blogpost, we will discuss Multigenerational families. In last blogpost, we discussed Single-parent households.

Single person, living alone, with no children For singles living alone with no children, your primary dependent is yourself. And single-person households make up more than a fourth of all U.S. households nowadays. Not having a partner can make it harder to save — you don’t have two incomes and you don’t have the economies of scale that you get from sharing housing, utility, and food costs. In expensive parts of the country, home ownership can be out of reach for singles. On the plus side, not having children means incredible savings. There may be less of a need to purchase life insurance since, depending on circumstances, no one directly depends on your income. On the other hand, some single situations may contradict that thinking. While everyone should plan to be financially self-sufficient, considering long-term care insurance options is extra important for this group, who can’t count on children to help care for them in old age. Planning for unemployment and disability is also essential for singles, since there’s no second income to fall back on. Saving a substantial emergency fund to cover several months’ worth of expenses, purchasing disability income insurance, and starting a side job or piece work to diversify your income stream can make things less precarious. It’s also important to have a will and a trust to spell out what should happen to your assets when you die and keep the process out of probate court. In next blogpost, we will discuss Same-sex couples. In last blogpost, we discussed blended families.

Single-parent households In 2020, there were about 15.31 million children living with a single mother in the United States, and about 3.27 million children living with a single father, according to one analysis. In these families, caring for a dependent can be especially tough, because divorce often slashes a family’s income and assets, as does never partnering up in the first place. Single parents are less likely to be saving enough for their own retirement and may be extra stressed by trying to save for themselves while wanting to help children pay for college. Alimony and child support may be insufficient to pay for major expenses like childcare during work hours, extracurricular activities, braces, and college because the original arrangements were made without the child’s long-term needs in mind. What will happen to the child if the single parent becomes ill or passes away is the primary concern for single-parent households. So, a sole breadwinner should focus on disability planning and insurance. To that end, the parent should establish an emergency fund and secure disability income insurance. The emergency fund is key because disability income insurance policies typically have a waiting period before making payments on a claim. The emergency fund can provide for living expenses before the disability income insurance policy’s waiting period is up and even while it’s paying benefits, since the insurance typically will only replace 50 percent to 70 percent of monthly income. Life insurance is also a priority to help ensure children’s financial needs will be met if the parent passes away before they become financially self-sufficient. Single parents must resist the urge to put saving for their children above saving for their own retirement because they have no spouse to help with retirement savings or retirement expenses and since the division of assets in a divorce may have taken a bite out of their retirement savings. Further, federal financial aid doesn’t count a parent’s retirement assets against a child’s college financial aid package. One simple thing single parents can do to improve their finances is to file as head of household on their annual tax returns. This status will result in a lower tax rate and higher standard deduction than filing single. If you feel as though things are particularly precarious as a single parent, keep this in mind: no family style is guaranteed to be stable. All families must create their own stability and recognize what they can and cannot count on. Next, we will discuss Single person, living alone, with no children. Q. For estate taxes, does it matter what types of accounts I'm leaving to heirs? What if all my money is in a retirement account, like a 401(k), or it's all in a brokerage account or some other type of account? Do I need to start reorganizing how my money is held given the changes ahead?

A. The federal estate tax applies to the value of all assets that a decedent owns or controls at death, regardless of the type of account in which the asset is held. You might want to consider, though, that only assets held in certain types of accounts can be efficiently transferred. For example, retirement accounts, such as 401(k)s or traditional IRAs, cannot be transferred to a third party during the account holder's lifetime without triggering income taxes and possibly penalties. For this reason, most gifting strategies focus on transferring nonqualified, or taxable, assets, such as assets in a brokerage account or real estate. For people with a disproportionate amount of their wealth in retirement accounts, planning strategies shift to improving the income tax efficiency of the transferred accounts to reduce the beneficiary's income tax burden. Roth conversions, for example, may be an effective strategy to accomplish this goal. But, for estate tax purposes, the entire value of the converted Roth account will be included in the owner's estate. Financial-planning.com has an article that details why the proposed tax plan upends estate planning using trusts with life insurance.

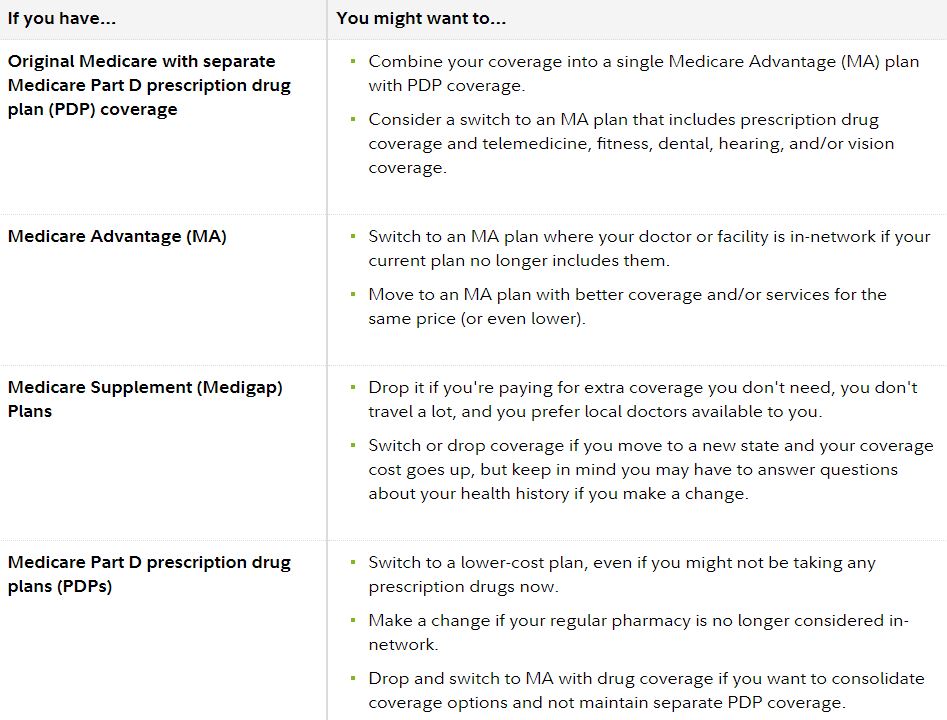

‘Crisis stage’ The blow to life insurance in trusts, a bread-and-butter wealth preservation strategy of the rich for decades, is one of many proposals in the emerging tax bill that take aim at the wealthy to finance President Joe Biden’s $3.5 trillion social spending plan. The draft bill would raise the top individual rate to 39.8% from 37% and bump up the top capital gains rate to 28.8% from 23.8%. It would tax capital gains at the top ordinary rate once income hits $1 million, crack down on large retirement accounts and end backdoor Roth conversions, a favorite strategy of high-income earners to create tax-free profits. And it would kill the use of grantor trusts, the workhorse of estate planning, whether or not they contain life insurance. It's easy to see what the tax perk has been. Say a person dies owning a $3 million home, $7 million in retirement accounts and $4 million of life insurance not held in a trust. With the current estate tax exemption at $11.7 million, $2.3 million of that $14 million estate would incur the 40% estate tax — a bill of $920,000. Now assume instead that the insurance policy is in a grantor trust. It wouldn’t go into the person’s estate, leaving nearly $1 million more for heirs. Such savings would no longer be possible under the proposal. In any case, the historically high level at which estate taxes kick in would fall by nearly half to under $6 million in the House plan. Under the House bill, “the life insurance issue has moved things to crisis stage,” said Steve Parrish, who co-directs the Center for Retirement Income at The American College of Financial Services. “Right now, webinars, emails and panicked calls are circulating among estate planning professionals.” One particularly hairy element, he said: Advisors are “trying to draft answers to their clients that avoid professional liability if they’re wrong.” ‘A major impediment’ The legislative proposal has upset financial advisors and estate lawyers because it’s common for life insurance to be held in a widely used type of trust called a grantor trust. “This problem with insurance is really buried in the legislation,” said Warren Racusin, the head of the trusts and estates group at law firm Lowenstein Sandler in New York. A grantor trust is a type of trust over which the owner, meaning the grantor, retains control and pays income tax on its gains. It comes in many flavors, including intentionally defective grantor trusts, or IDGTs, and grantor retained annuity trusts, or GRATs — all alphabet soup names well known to estate planners for the rich. Advisors say that most irrevocable life insurance trusts, or ILITs, are set up as grantor trusts, so they’d be hit by the curb, too. The proposal says, in obscure language, that any assets contributed to grantor trusts come 2022 would become part of the grantor’s estate for estate tax purposes. The issue is that under the plan, a policyholder who pays her annual premiums for a policy that’s held in a trust would be “contributing assets,” thus making the trust subject to the 40% estate levy. While the proposal would “grandfather” existing grantor trusts, that’s small comfort for those with life insurance. According to Mari Galvin, the chair of the trusts and estates group at law firm Cassin & Cassin in New York, it’s not clear from the proposal whether all of a trust could be shunted into the owner’s taxable estate if premiums are paid after this year, or just the portion related to the premium payments starting next year. “Time will tell,” Galvin said. In any case, the grandpa safety net could be mighty small. Trusts that already exist and whose policies are fully paid would “most likely” remain grandfathered, according to Andrew Bass, the chief wealth officer of Telemus Capital, an independent advisor with brokerage services in Southfield, Michigan, that manages nearly $2.2 billion for high net worth investors. But only, Bass added, if the terms of the trust prohibit it from using its own income to pay premiums. The problem, he said, is that “most trusts were written with language that allowed trust income to be used for payment of premiums, thus forcing a loss of grandfathered status.” In any case, wealthy individuals who want to create a future trust for their life insurance couldn’t make their spouse a beneficiary without subjecting the trust to estate tax. That’s because such a trust is automatically a grantor trust and thus would have to pay estate tax under the proposal. “That is a major impediment, as insurance is typically needed by a surviving spouse,” Bass said. The solution becomes the problem The proposal has the potential to upend retirement planning. “Life insurance is used by the well-heeled to both conserve and create an estate,” Parrish said. But if a policy’s death benefit gets hit with a 40% tax at death, “the insurance becomes the problem rather than the solution.” The idea of pre-paying premiums revolves around using outside funds, not money inside the trust, as the latter would get caught by the proposed curb. “We are advising clients to pre-fund their premiums now” by contributing cash or other assets before the new law passes so that no additional outlays are required to pay future premiums, said David Handler, a partner in the trusts and estates group at law firm Kirkland & Ellis in Chicago. That’s easier said than done. Ponying up early premiums for a large “permanent” policy that lasts for life can cost millions of dollars. Where to find those dollars between now and New Year’s Eve? Individuals might have cash on hand, or they might contribute securities to the trust which can be sold over time to pay the premiums, Racusin said. Handler said that others "might borrow from banks.” But Parrish said many investors would be left out in the cold, because “in many cases, these policies are financed through loans, so it’s impractical to pre-pay the premiums.” Flying blind The proposed curb would hit not just the very rich. People of more middling wealth, for whom a life insurance policy is often their trust’s single largest asset, would also feel pain. For example, a person might have a net worth under the estate tax threshold but also a large life insurance policy to care for their family if they die prematurely and their income grinds to a halt, Handler said. Which means that when the insurance death benefit is paid, the decedent’s total assets can exceed the estate tax exemption. Wealth advisors and estate planners say they're flying by the seat of their tax pants. Advisors, Parrish said, “are feeling damned if they do” (pre-paying or taking other moves) and “damned if they don’t" (adopting a wait-and-see approach to whether the proposal becomes law). Bass said one solution might involve “decanting” a grantor trust, like a fine wine. That strategy involves “pouring” a trust’s assets into a new trust. Or a trust could pay the insurance premiums through so-called split dollar arrangements, which are common with wealthy executives. Or it could be set up so that beneficiaries other than a spouse would have to approve any distributions out of the trust to the spouse, “but that could cause family rifts and may have gift tax implications for the kids,” Handler said. Racusin likened the tax contortions to navigating wealth planning with blinders on. “It’s kind of like an architect telling a builder, ‘hey, I need you to build this house right now, but I don’t have the plan, but you need to start building it right away.’” The good news for individuals enrolled in Medicare: If you're not satisfied with your current Medicare coverage, you can make changes during the Medicare Annual Enrollment Period (AEP), which runs every year from October 15 to December 7.

Generally, there are 5 reasons why you might consider making changes to Medicare coverage:

Tip: Keep in mind, any changes you make take effect on January 1 of the upcoming year. Q. I am retired and covered under my wife's work insurance. Do I need to enroll in Medicare when I turn 65?

A. As long as your spouse is actively employed and insured, you can remain on her policy until she leaves the job or retires. After that, you can sign up for Medicare Part B (covers doctor visits and outpatient services) and Part D (covers prescription drugs) without paying any late sign up penalties. In the meantime, when you turn 65, you can still enroll in Medicare Part A (covers hospital bills), there is no cost for that and it gets you into the system. The caveat, if your spouse works for a business with fewer than 20 employees, you may have to enroll in both Parts A and B.

There are three Social Security “do-over” strategies for people who have already claimed benefits.

First, any individual who has claimed Social Security retirement benefits can withdraw their application within 12 months of doing so. This allows the individual’s monthly benefit to continue to grow, but they (and any family members receiving benefits based on the worker’s earnings record!) must pay back any benefits already received. This strategy could be useful for individuals who decide to go back to work within a year of claiming their benefits. Second, going in the opposite direction (for those who wish they had claimed earlier) is to elect to receive a lump sum payout of six months of retroactive benefits, which is available to (only) those individuals who have reached their Full Retirement Age (FRA). Thus, a retiree in need of a short-term cash infusion could retroactively start their benefits if they wish they had started earlier (and take the lump sum for what they missed!). The third strategy for recipients who have reached their FRA is to suspend retirement benefits in order to get delayed retirement credits until age 70, at the latest. This option is potentially useful for married couples because, if the higher-earning spouse had originally started benefits early (reducing their payments), subsequently suspending their benefits can increase their benefits again, such that if the higher-earning spouse dies first, the survivor will get the larger benefit amount. Notably, those who claim a retroactive 6-month payment for delaying can do so and then also suspend their benefit after taking the lump sum, receiving the lump sum (for a small infusion of cash) and still earning delayed credits up to age 70! This excellent article from Fidelity.com discusses how to delay Social Security, boost benefits, and build an income bridge to get there.

It answers or helps you think several questions:

Despite the advancements in measuring risk tolerance, Pfau and Murguía argue that risk tolerance questionnaires are more valuable during a client’s accumulation years, and are less useful when assessing risk tolerance in their decumulation years in retirement when sequence-of-return risk becomes a serious issue.

Accordingly, Pfau and Murguía suggest advisors and clients first need to decide on a retirement income strategy, and only then consider a (risk-tolerance-appropriate) asset allocation in retirement. Potential retirement income approaches include:

Once a strategy is selected, Pfau and Murguía propose a tool that uses two scales to determine the client’s risk tolerance in the decumulation period: probability-based income sources (e.g., from market growth) versus safety-first income sources (e.g., from contractual obligations), and optionality (degree of flexibility) versus commitment (adherence to a single solution) with respect to how much a client is willing to change their approach in response to economic or personal developments. The results of this exercise can then be used to select appropriate investment products to meet the client’s needs. The key point is that selecting an appropriate allocation of assets in retirement isn’t just a function of the retiree’s tolerance for market volatility… instead, it starts with their preferences for even taking a risk-based investment (versus a more guaranteed-income) approach in the first place, and how much spending flexibility they have (or want or need) along the way! Mathematically, the Roth-versus-traditional IRA decision will actually be the same, regardless of growth rates and time horizon, as long as both accounts remain intact and tax rates don’t change.

If future tax rates do change, though, the Roth IRA will result in more wealth when tax rates rise in the future, while the traditional IRA will benefit when tax rates are lower in the future. Though in practice, because the tax burden for a Roth IRA is paid upfront – when the (after-tax) contribution is made – there is no future uncertainty with respect to its future tax rate; instead, changes in tax rates primarily impact the future value of a traditional IRA, in particular, making it better or worse off depending on whether or how tax rates change. To cope with this uncertainty, one popular approach is to ‘tax-diversify’ between the two types of accounts, splitting contributions between traditional and Roth IRAs so that there is at least ‘some’ benefit regardless of which direction tax rates go (as higher tax rates benefit the portion of dollars in the Roth, and lower tax rates would benefit the traditional IRA dollars instead). However, the reality is that splitting dollars between traditional and Roth retirement accounts isn’t just a form of diversification; because the outcomes are correlated to each other, the net result is that tax diversification doesn’t actually diversify the risk, it simply neutralizes the opportunity altogether. Or viewed another way, splitting between traditional and Roth IRAs is more akin to just bailing out of stocks altogether and owning zero-return cash. If you want to see a more thorough discussion of this topic, here is an excellent article. Are you ‘shopping’ for retirement solutions? You may have growth, guarantees, lifetime income, tax advantages and more on your list … but do you know annuities could offer you all? Here is a “Retirement Shopping” video. Roth 401(k)

People who have the option can contribute to a Roth 401(k) in order to accumulate assets in a Roth account. The proposed legislation does not limit these contributions, and the money can be rolled over to a Roth IRA when you leave your employer. In many cases, a Solo 401(k) can offer a Roth option as well. This would work in the same fashion as a 401(k) offered via an employer as far as the employee contribution component. Health Savings Account (HSA) HSAs are a great vehicle for people who have access to a high-deductible health insurance plan. Health savings accounts allow for pretax contributions and withdrawals to cover eligible medical expenses are tax-free. HSAs can act as another retirement account in that the money contributed to the HSA can be carried over from year to year if not used. This makes an HSA a great way to save for medical costs in retirement, essentially making it a tax-free retirement savings account. Many HSAs allow the money to be invested. If the money is not used for medical expenses in retirement, it can be withdrawn just like a traditional IRA with taxes due on the money. Contribution limits for an HSA are:

Life Insurance A whole life insurance policy, along with some other types of cash value life insurance, is another way to build tax-free income in retirement. This is more complex than a backdoor Roth to be sure, but if this is a fit for you this can be an alternative. Essentially, you would purchase the life insurance policy. Part of the premium funds the growth in cash value. They can withdraw the portion related to the premiums tax-free and take a policy loan against the rest of the cash value that will have accrued from dividends. The additional withdrawals will serve to reduce or eliminate the death benefit. Upon their death, the death benefit passes to your heirs tax-free. There are a number of cautions and caveats to this approach, including ensuring you don't withdraw too much so as to create a modified endowment contract situation. Additionally, the cost of the premiums and your need for the death benefit should also be considered. The House Ways and Means Committee recently passed $2.1 trillion in tax hikes that will help fund President Joe Biden’s American Families Plan. Among their proposals are the elimination of backdoor Roth and mega backdoor Roth IRA conversions. Both of these provisions could affect people who earn too much to contribute to a Roth IRA and those who want to ramp up their Roth account balances.

The proposed legislation would end the ability to convert after-tax contributions in both 401(k) plans and traditional IRAs to a Roth after Dec. 31, 2021, effectively killing both of these options. People who have been making after-tax contributions to their 401(k) plan to fund a mega backdoor Roth conversion need to make some decisions this year. If their plan allows for the conversion of this money to a Roth 401(k) account within the plan, this needs to be done prior to Dec. 31, 2021, if the legislation passes as is. Note that any earnings on these after-tax contributions will be taxable upon conversion. If the plan allows for in-service withdrawals in order to roll this after-tax money to an IRA and convert to a Roth, you will want to consider doing this by the end of the year. If none of these options are available to you, the after-tax contributions would be stuck in the plan until you leave the company. Unless this happens prior to Dec. 31, 2021, you will lose the opportunity to convert this money to a Roth if the proposed legislation passes. For people who may want to make an after-tax contribution to a traditional IRA and do a backdoor Roth conversion, this also needs to be done by Dec. 31 of this year if this legislation passes. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed