Here is an updated version of 2022 tab tables from Athene.

|

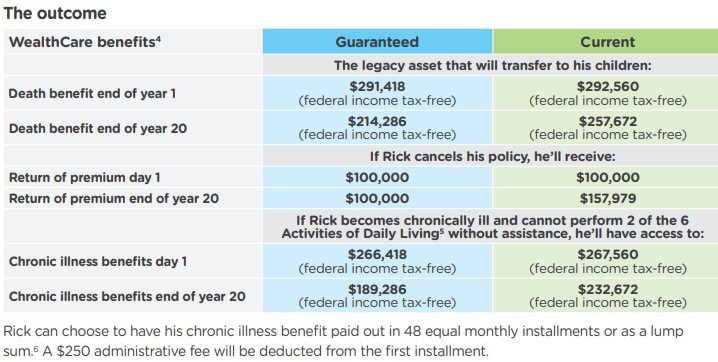

Taxes are constantly changing. And, this could lead to unanticipated tax risk for your clients and their heirs. That’s why many individuals are not waiting until retirement to prepare. Here’s an example of what someone could do now to protect their assets and their loved ones who will inherit them. Case Study: An asset for tax diversification Rick is age 55. He and his wife, Tina have two adult children. This couple recently sold their home and moved to a condo in town. They made a nice profit on the sale, and Rick is ready to use part of the money in a tax-efficient way. Rick’s goals • Finding an asset that offers tax-advantaged growth • Creating a legacy for his children without creating tax risk for them • Establishing his plan for care Rick’s concerns • Facing market risk and losing the profit he made on his home sale • Not knowing what income and capital gains taxes will be in the future The solution In conjunction with recommendation from Rick’s tax and estate planning team, Rick purchase a $100,000 Indexed Single Premium Universal Life Insurance policy as a differentiated asset within his portfolio. This will provide the liquidity of a full return of principal, tax advantaged growth, guarantees, an income tax-free legacy for his children, and income tax-free chronic illness benefits if he would ever need care. At the time of purchase, Rick chooses the Global Multi-Index Bonus HIGH PAR Strategy which can help his death benefit grow tax-deferred over time. He’ll have principal protection and will never face losses due to market performance. The outcome  Although having a retirement savings number is important, it’s also a moving target and fixating on one number runs the risk that you won’t adjust your savings goals to new circumstances, such as higher health care costs, inflation or the vagaries of the economy. Life isn’t stationary and your retirement plan, including any target savings number, shouldn’t be either.

Instead of focusing exclusively on the size of your nest egg, create a comprehensive retirement plan that you’ll refine and change over time. It should include your financial goals, a net worth statement, a working budget, debt management strategy, emergency funds and any insurance. Any retirement plan also should reflect your expected retirement lifestyle, investing horizon, risk tolerance, savings goals and estate planning. You’ll want to consider how your retirement savings would hold up under different scenarios, simulating extreme market conditions or unexpected life events, to be sure your bases are covered. A financial professional can help you do it or use Microsoft’s free online Retirement Financial Planner template. Revisit the plan every few years while you’re accumulating assets and whenever you have a life change, such as switching jobs, losing a family member or moving. As retirement nears, the plan should factor in your required minimum distributions to minimize your tax burden. You want an appropriate mix of taxable and nontaxable investments, such as a Roth IRA combined with a taxable brokerage account, as well as a balance of stocks, bonds, real estate and other assets. Many retirement spending models use the 4% rule in which retirees withdraw 4% from their retirement portfolio in the first year of retirement. Each year thereafter, they adjust the dollar amount of their withdrawals by the previous year’s rate of inflation. The rule is designed to prevent retirees from running out of money during a 30-year-retirement. Your current spending also may be nothing like your retirement expenses because when we have more leisure, we often spend more. In retirement, health care costs escalate dramatically. Working households spend about 6% of their annual budget on health expenses, versus 14% for retirees, according to the Kaiser Family Foundation. You need to allow for flexibility because your life is going to change over time. Although you may be perfectly healthy now, things could happen, and there could be additional costs associated with your care. Q. How can an annuity be used by an individual as an estate planning tool?

A. In order to avoid the potential tax and financial repercussions that a lump sum transfer can create, many individuals wish to protect their heirs by providing structure to the way assets are inherited. For these taxpayers, annuities, though commonly used as retirement income planning tools, can provide the solution. The reasons for using an annuity as a wealth transfer vehicle often mirror those that apply when a taxpayer is planning for retirement—the annuity creates a stream of consistent income over time, guaranteeing that the taxpayer’s beneficiary is provided for far into the future. This strategy can protect heirs who might be otherwise unable to manage a large one-sum payment, or who might have financial problems that could cause them to spend a large sum too quickly. Q. If an annuitant dies before a deferred annuity matures or is annuitized, is the amount payable at the annuitant’s death subject to income tax?

A. Yes, to the extent there are any gains. An annuity contract generally provides that if the annuitant dies before the annuity starting date, the beneficiary will be paid, as a death benefit, the greater of the amount of premiums paid or the accumulated value of the contract (although some contracts may provide additional “enhanced” death benefits as well). The gain, if any, is taxable as ordinary income to the beneficiary, and is measured by subtracting (1) investment in the contract (reduced by aggregate dividends and any other amounts that have been received under the contract that were excludable from gross income) from (2) the death benefit, including any enhancements. Below is part of a recent WSJ article that discusses 4 major questions that investors are wrestling with, and any one of which could hit stocks hard.

Will inflation hammer profit margins? Companies are faced with soaring input costs, with producer prices rising even faster than consumer inflation, itself the highest year-over-year rate since 1982. Investors are closely focused on which businesses have the power to raise prices to offset higher costs. On Friday Clorox stock plunged 14%, the worst in the S&P 500, in large part because it warned about rising costs. Amazon was up 14% in part because its planned increase in the price of a Prime subscription reassured investors that it can offset soaring delivery and labor costs. Will Covid-era gains fade? Lockdowns accelerated the switch to many online services, but some will prove temporary. No one wants to be like Peloton Interactive, whose home cycling workout has proved tougher to sell when customers have the choice of outdoor exercise, and whose stock has lost three-quarters of its value since its peak a year ago. Some of the reason for Netflix’s big fall after its earnings was because it turns out people prefer real life to home movies; similarly, Clorox disinfectant sales have fallen back, and PayPal growth has slowed. Will Big Tech eat itself? One of the most attractive features of the leading online platform companies is the defensive benefit they get from being big, what are known as “network effects.” People use Facebook because other people use Facebook, so everyone has to use Facebook. Except, not so much. Meta stock tumbled 26% on Thursday primarily because TikTok is beating it in the competition for young eyeballs. Amazon and Apple made Meta’s situation worse, Amazon because it is snaffling advertising dollars at a rapid rate, Apple by changing privacy settings, something Facebook has struggled with. Competition has already hit several other tech themes. Netflix has to spend heavily to maintain its position because of the streaming wars with services from Amazon, Disney, Comcast and others. Uber Technologies got an early lead in online taxi services, but it turned out to be an easy model to copy and many other services sprang up around the world, competing both for customers and drivers. The pattern is a standard one in tech: Microsoft has long since lost its virtual monopoly in operating systems and word-processing software, while IBM’s dominance of PC hardware is ancient history. The battlegrounds of the future are cloud computing and self-driving cars, and the competition is keen. So far there’s no sign of a slowdown in the cash milked from the cloud by Amazon, Microsoft and to a lesser extent Alphabet, but all are investing heavily, and it might become competitive in time. True self-driving cars aren’t for sale yet, but Alphabet, Apple and Tesla are all spending heavily on development and, in the case of Alphabet’s Waymo, some limited services. Amazon and Intel have bought in to the area, and a bunch of traditional carmakers have made progress, too. Whoever cracks it first might get a big lead, and would deserve a big valuation, but competition, as well as regulation, would surely follow. Will bond yields carry on up? Growth companies are highly sensitive to bond yields, because so much of their lifetime profits lie further in the future than cheaper businesses. Bond yields jumped again on Friday on the back of a strong jobs report, taking the 10-year Treasury yield up to where it started 2020 for the first time since then. If the economy stays strong and yields keep rising, it will be a headwind for the big growth stocks. Should annuity buyers time the market? That is the question this thinkadvisor.com article tries to answer. Its conclusion? See below:

The Fed is expected to raise rates at least three times in 2022 and end its asset purchases in Q1. The trajectory of the coronavirus pandemic and fate of President Biden's economic plan could upend those expectations. Strategists recommend that investors stay in the short end of the yield curve and stick with high-quality securities.

The above is the summary of the bond strategies recommended by thinkadvisor.com for 2022, if you want to read for more details, follow this link. Thinkadvisor.com has an article that introduces the new state birthday rules, and calling it one of the least known opportunities for seniors.

Medigap Basics The Medicare Part A hospitalization program pays hospital bills, and the Medicare Part B program pays outpatient and physician services bills. Medigap policies can help consumers pay their Medicare Part A deductible and meet the traditional Medicare copayment and coinsurance requirements. Consumers can also buy Medicare Advantage plans. Those policies tend to offer enrollees broader coverage than the traditional Medicare program, in exchange for giving the enrollees financial incentives to use in-network providers and requiring the enrollees to get preauthorization for some medical procedures. Many producers strongly prefer selling consumers Medigap policies, because they see both the rules for producers and the coverage rules for the patients as being more flexible. For producers, one obstacle to selling Medigap policies has been higher monthly premium costs for Medigap coverage. Another obstacles has been the difficulties unhappy Medigap users have with switching policies. Medigap Enrollment Period Rules Health insurers, and some voluntary public health benefits programs, use “open enrollment period” systems, or limits on when people can buy coverage without going through much, or any, medical underwriting, to encourage healthy people to pay premiums even when they feel fine. The idea is to keep healthy people in the risk pool, by raising the possibility that they could break legs or suffer heart attacks, and have no way to get health coverage, outside the open enrollment period. Federal law creates a one-time, six-month Medigap policy open enrollment period period after a consumer’s 65th birthday. After that, Medigap users must show they qualify for a special enrollment period to switch Medigap policies. Users can get special enrollment periods easily when they move to new markets. Otherwise, they may have to show that their Medigap plan issuer has broken federal government rules or shut down. Idaho, Illinois and Nevada The new Idaho birthday rule is set to take effect March 1 2022. It will create a 63-day plan switching period beginning on the policyholder’s birthday. The new policy must offer the same level of benefits as the existing coverage or a lower level of benefits. The Medigap policy user can either switch insurers or change to a new Medigap policy from the same issuer. Idaho will switch to a community rating system for Medigap enrollees, meaning that premium rates will no longer be based on the age of the applicant. In Illinois, a new birthday rule will take effect Jan. 1, 2022. The Illinois rule will let Medigap users ages 65 through 75 have annual Medigap open enrollment periods lasting 45 days after their birthday anniversaries. The new policy must offer the same level of benefits as the existing coverage or a lower level of benefits. In Nevada, a new birthday rule will take effect Jan. 1, 2022, and provide 60-day plan switching periods starting on the first day of a Medigap user’s birthday month. Eligible consumers can buy new coverage, with the same or lesser benefits, from either their existing carriers or new carriers, without medical underwriting. A consumer cannot use the new rules to get policies with extra, innovative benefits, such as dental insurance, vision insurance, hearing benefits or gym memberships, officials say. Why the Quirks? One reason the new birthday rules are complicated is that insurers and government officials have been trying to give consumers ways to switch coverage without increasing the odds that some especially generous or well-run Medigap issuers will attract large numbers of new enrollees with very high health care costs. Another reason is that Congress created the Medigap program before the Medicare Advantage plan, and it left much more responsibility for regulating Medigap policies in the hands of the states. States have more ability to tailor Medigap rules to suit local needs, but that means producers who do business in two or more states may have to use different strategies for clients in different locations. Financial-planning.com has an article analyzes if Roth IRA conversion is still a risk worth taking this year, see below -

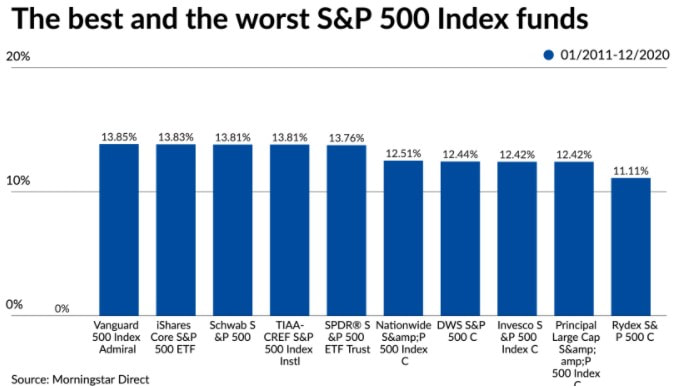

Go all out on contributions to retirement plans Didn’t max out your contribution limits last year? The IRS allows contributions for 2021 to be made through April 15, 2022. That’s three days before this year’s April 18 filing deadline, which was extended due to the Emancipation Day holiday in Washington, D.C. Some contributions are deductible, so they’ll lower the total amount of income on which taxes fall, a savings to the taxpayer. For 2021 returns being filed now, Americans could contribute a maximum $6,000, plus an extra $1,000 if aged 50 or older, to a traditional individual retirement plan (IRA) or Roth IRA. So an older married couple can put in a maximum $14,000. Traditional IRAs are generally funded with money on which taxes haven’t yet been paid, while Roth plans are fueled by after-tax dollars. Pretax contributions grow tax-deferred, with the owner paying ordinary rates on future withdrawals. While investors can also contribute money on which they’ve already paid taxes, they pay ordinary tax on withdrawals, making after-tax contributions to a traditional IRA a double tax hit. In contrast, Roth plans grow tax-free, with no levies on withdrawals. Deductions get complicated, depending on how much a taxpayer makes and whether she or a spouse has a workplace retirement plan. A traditional IRA owner who doesn’t have a workplace retirement plan (or whose spouse lacks one) or whose income is below $76,000 gets a whole or partial deduction. If a married couple filing jointly has one spouse with an employer-sponsored retirement plan, typically a 401(k), then an IRA contribution by the other spouse is no longer deductible once their joint income hits $214,000. Straightforward Roth IRA plans are a little different. The contribution limits are the same. But while there are no income limits on who can contribute to a traditional IRA, contributions to Roth plans now are limited to people who made under $140,000 last year (under $208,000 for couples). Because their assets grow tax-free and don’t bear future taxes, Roth contributions aren’t deductible. The Roth conundrum It’s still not clear what might happen to so-called backdoor Roth conversions, a mainstay of large retirement accounts and estate planning for the wealthy, under stalled legislation in Congress. While emerging versions of the Build Back Better tax-and-spending bill aim to limit or ban the ability of high earners to own Roths through indirect methods, the legislation is mired in infighting by Democrats. But some tax and retirement experts think that it’s probably safe to take advantage of their current tax benefits, even as legislators work to curb them. January 31, 2022 8:36 PMBackdoor conversions involve an investor converting a traditional IRA into a Roth. They’re a way for wealthy people to sidestep the income limits for direct contributions to a Roth. An early version of the House bill banned conversions of after-tax dollars in IRAs and 401(k)s. The House passed a somewhat softened version of that proposal last November. The legislation, which has to be passed by the Senate, would outlaw so-called mega-backdoor Roth conversions starting Jan. 1, 2022. The strategy came under a spotlight when ProPublica showed how PayPal co-founder Peter Thiel used it to transmute less than $2,000 worth of pre-IPO shares into a $5 billion account. The bill would still allow regular Roth conversions but would ban people with higher incomes from doing them starting in 2032. Last December, the Senate offered its own version of Build Back Better that proposes those same limitations. The backdoor strategy involves using hefty after-tax contributions to a 401(k) plan that permits them. Under IRS rules, a taxpayer could put as much as $58,000 last year into a workplace retirement plan ($64,500 for those 50 or older). One chunk of the money reflects the maximum pre-tax amount of $19,500 ($26,000 if 50 or older), while the remainder, up to $38,500, reflects after-tax dollars. The limits include any company matches. The taxpayer then converts her 401(k) to a tax-free Roth. The higher amounts can swell a retirement portfolio far beyond what direct contributions to an ordinary Roth can. Christine Benz, Morningstar’s director of personal finance, wrote in a Jan. 21 research note that it’s “unlikely” that when a final bill makes it to President Joe Biden’s desk for signature, if indeed one does, the proposed curbs would be retroactive to the start of this year. “Given that these contributions and conversions are currently allowable,” she wrote, financial advisors have “been urging their clients to go ahead with them until the law officially changes." Benz quoted Aron Szapiro, the head of retirement studies and public policy for Morningstar, as saying that the likelihood of a retroactive ban on after-tax contributions is "close to zero.” Of course, nothing’s final on Capitol Hill until it’s final. Nonetheless, Benz wrote, “given that backdoor Roths are one of the few mechanisms that higher-income heavy savers can use to achieve tax-free withdrawals and avoid RMDs in retirement, many such savers are apt to conclude that it’s a risk worth taking." Morningstar Direct said that the 10-year annualized return through last December for index funds in all forms ranges from 14.61% (for the Rydex S&P 500 H) to 16.49% (for the iShares S&P 500 Index K). The nearly 2% difference means that $50,000 invested in the Ryder fund would hand an investor just over $195,500 after a decade, while the same amount in the iShare fund would yield more than $230,000 — a roughly $34,500 difference. The fees charged by mutual funds range widely, so it’s not surprising that returns for those funds vary, even if they’re passively following a benchmark. What about returns by the four low-cost ETFs? They also vary in their performance, even though they’re roughly charging the same low costs and following the same benchmark. Blame benchmark-tracking glitches and their lucrative practice of lending stock to big banks, a move that can paradoxically cause a fund that passively mirrors an index to, in fact, beat that index.  There may be a silver lining for crypto investors selling at huge losses during the recent market turmoil: a quirk in the Tax Code that lets people minimize what they’ll owe the government down the road.

Unlike stocks and bonds, cryptocurrencies aren’t subject to federal rules that bar people from claiming deductions if they sell an asset at a loss and then buy an identical or similar asset within 30 days before or after the sale. That provides a unique opportunity for people suffering steep losses to sell and reap future tax savings, then buy more virtual tokens at cheaper prices, according to crypto tax filing software firms. This is a great time to store your capital losses, because when you exit the market at a future date at a huge gain, you can use these losses After surging 60% in 2021 — and touching an all time high of nearly $69,000 in November — Bitcoin has fallen 20% to under $37,000 this year. The impact of crypto’s January turmoil won’t show up on investor’s 2021 tax returns. However, thousands of crypto investors who piled into the asset class last year must account for those investments as they file their returns during the next few months. Investors who sold crypto at a loss and then purchased similar assets at a lower price — a move that some refer to as wash sales — are free to take advantage of the tax strategy, according to TaxBit, a crypto tax software company. Some Democrats tried to close the loophole in a roughly $2 trillion spending bill that failed late last year. “Tax-loss harvesting” Strategy Under the strategy, investors can use their losses to offset any gains in a given year. If they don’t have gain to offset, they can deduct up to $3,000 in losses from ordinary income. Any excess capital losses above that amount can be used to lower tax bills in subsequent years. With all the tax legislation oxygen taken up by BBB, many have forgotten about Secure 2.0, but it’s still waiting to see the light of day.

Keep an eye on this bill. Of all the the bills that could be enacted in 2022, this one has the best chance, having passed out of committee unanimously, with full bipartisan support. See if you may be affected by these proposals in 2022: ‘Rothification’ Secure 2.0 includes provisions allowing both SIMPLE and SEP Roth IRAs. In addition, plan catch-up contributions would be required to be made to Roth plan accounts, and plans could allow participants to have employer matching contributions made as Roth contributions. Other Proposed Changes

Thinkadvisor.com recently had an article that highlights the flaws of target date funds, it's worth a reading if you have or plan to invest in target date funds.

Highlights of the article include:

Mutual funds generate capital gains taxes each time they sell an underlying holding that has appreciated, even if an individual investor holds on to her fund. So that cost is passed on to her. By contrast, ETFs use an obscure tax loophole to cash in on appreciated holdings by swapping assets with a buyer — in this case, major banks.

For example, a fund sells an appreciated stock in its “basket” of shares to a bank and immediately buys back “substantially similar” shares. Because no cash has traded hands, there’s no capital gains tax on those profits. Or an ETF can sell a losing stock, deduct the loss, then buy back similar stock. The deduction boosts the returns of the fund. Of course, when an investor sells her ETF, she owes capital gains tax on the profits. But until she does, the capital gains taxes on internal trades made to keep the fund in line with its benchmark are “washed away.” With active trading strategies, the tax perk for the new semi-transparent and opaque ETFs is even more significant. As well as potentially more prone to scrutiny. Sen. Ron Wyden, who heads the Senate Finance Committee, called in Sept. 2020 for an end to ETFs’ use of “in-kind” transactions to avoid triggering capital-gains taxes. In 2001, Vanguard, the world’s second-largest asset manager, acquired a patent for a novel, tax-efficient fund structure that blends a mutual fund and an ETF by bolting on an ETF share class to its existing stock mutual funds. The patent expires in May 2023, which could open the flood gates to lookalike funds from competitors — and to greater scrutiny by regulators and critics, who argue that the structure’s tax benefits are controversial.

Vanguard’s secret sauce has several benefits. Ordinarily, investors in a mutual fund owe capital gains taxes when that fund sells stock. The Vanguard patent uses an obscure, decades-old tax loophole to eliminate those levies both in a mutual fund and an ETF. The loophole says that when withdrawals from a fund are paid with stock, not with cash, there’s no capital gains hit for the investor. For withdrawals, Vanguard uses rapid trades to whisk appreciated stock out of both a mutual fund and its sister ETF, then rapidly injects stock back in. A 2019 Bloomberg investigation detailed how those so-called “heartbeat” trades are fueled by big banks. Investors can swap their mutual fund shares for shares in a “sister” ETF, all without owing taxes on the profits. The tax erasure not only reduces taxes on paper profits but also allows investors to defer paying taxes on their profits until they ultimately sell their mutual fund. Because the patented structure involves two classes of shares, it gives investors the choice of holding a single investing strategy as a mutual fund or as an ETF. Vanguard’s secret method bolts an ETF onto an existing mutual fund, in contrast to competitors that issue stand-alone ETFs. While the entire investment holds the same securities, the ETF portion has a separate class of shares. The structure allows Vanguard “to have an ETF product that is almost identical to its mutual fund counterpart, which gives investors a wider range of product choice,” Shapiro said. “One fund, two share classes — that is unique.” Prior Cerulli research cited in the firm’s U.S. Exchange-Traded Fund Markets 2021 report showed that nearly four in 10, or 38%, of ETF issuers were considering adopting the Vanguard model once its patent expires. “Managers considering launching active ETFs should also keep an eye on the dual-share-class structure used by Vanguard, which comes off patent in 2023,” the Cerulli ETF report said. The benefit to financial advisors is that they “wouldn’t have to dig into specific differences between what’s in the mutual fund and what’s in the ETF,” Shapiro said. Still, he added that “it’s an open question” whether the new breed of active ETFs will get a green light to use the Vanguard recipe, given the controversy over its tax benefits. “It’s not clear that the SEC would approve it,” he said. Just 8 quick questions can help check your retirement readiness. Size up your situation with the Integrity Life Quick Check one-pager to prep for new year planning. For archived newsletters, please visit here.

When reviewing different Medicare options, some retirees might first look at the cost of premiums when selecting from the available plan options. However, because not all Medicare plans are created equal (and because retirees will have varying needs for medical care), choosing a plan with a lower premium could end up costing a retiree more in the long run.

One of the major decisions when enrolling in Medicare is whether to choose traditional fee-for-service Medicare or Medicare Advantage. Medicare Advantage plans can be attractive for some retirees because they often have lower premiums than the alternative of using traditional Medicare with Medigap and Part D prescription plans, and can come with additional benefits, such as prescription, dental, and vision benefits. Nonetheless, these plans can have high maximum out-of-pocket limits that could be reached if the insured has significant medical needs. Further, Medicare Advantage plans steer retirees to ‘in-network’ providers, meaning that a policyholder could end up paying significantly more for care if they are seen by an ‘out-of-network’ provider. Similarly, retirees choosing among Medigap policies might be tempted to choose the plan with the cheapest higher-deductible premium (which could result in significant out-of-pocket expenses if the retiree ends up needing expensive medical care), or at the opposite end, the plan with the most comprehensive coverage (which might lead the retiree to pay more in premiums when they could afford the deductibles and coinsurance of a plan with cheaper premiums). In the end, there is no ‘one-size-fits-all’ approach to selecting Medicare plans Navigating Medicare enrollment can be a tricky task for retirees, a Medicare specialist can help choose a particular plan that fits the retiree's situation the best.

First, the agent-vetting process can occur as the retiree is approaching Medicare eligibility age (typically 65), and a good agent should be familiar with the pros and cons of starting Medicare at the age of eligibility if the retiree has other options (e.g., a workplace retirement plan). Also, a good agent will also guide the retiree through the process of applying for Medicare Parts A and B, even though they will not earn a commission for doing so (as Medicare specialists are typically only compensated for Medigap supplemental policies, Medicare Part D prescription drug plans, and Medicare Advantage plans). Next, agents should be able to explain how the retiree’s Medicare premiums will be impacted by the Income-Related Monthly Adjustment Amount (IRMAA) based on the income. Finally, the agent can then help the retiree choose among Medigap, Medicare Part D, and Medicare Advantage plans for their specific state. For example, if the retiree is considering a Medicare Advantage plan, having an agent that is familiar with the insurance carriers and hospital networks in the retiree's state can help choose a plan that includes the best medical providers for the individual situation. Q. I am moving to another state where my Part D drug plan is not available. Can I get another plan?

A. If you have Original Medicare, you can get a new Part D plan without penalty if you do it in a timely way. If you get your medication coverage from a Medicare Advantage (MA) plan, it's a bit more complicated. You will likely need to switch to a new plan for all your coverage, as plans often do not cross state lines. The timetable is the same for original Medicare or an MA plan: your special enrollment period starts a month before your move and lasts until two months after the month you move. Q. If I am enrolled in Medicare, but I am still working, can I still contribute to my HSA?

A. No, you can no longer contribute to your HSA because you can only contribute tax-free dollars to an HSA if you have a high-deductible plan and no other health coverage. If you enroll in Medicare, you can still use HSA money to pay for out of pocket costs, but you cannot continue to make contributions to it. Note, you can still contribute to FSA, but you do have to use the FSA dollars in the same or following year. If you haven’t done so already, it’s time to get ready to file your taxes. Whether you use a tax professional or prepare your taxes yourself, the first step is to get organized, and a tax preparation checklist can help you do that. Here are some tips to help you get started.

*Collect your income records : Employers/companies send out W-2s and 1099s by the end of January. Review these documents carefully as soon as you receive them; if you find a discrepancy, you have plenty of time to get a corrected document. *Collect copies of year-end bank, brokerage, and investment account statements: These may contain needed cost-basis, transaction type, gain/loss information. They can also serve as proof of IRA contributions. *Organize and validate your deductible expenses and eligible tax credits (some may include) : *Work-related receipts *Receipts/payment records for charitable donations *Payment records of eligible medical co-payments *Education costs/student loan interest *Mortgage interest statement *Homebuyer tax credit *Check out one-time benefits that might apply: Investments in certain energy-efficient products (such as water heaters, central air conditioners, new windows and doors, and insulation) could make you eligible for tax credits this year. If you installed a solar energy system (or other type of renewable energy system) you may be eligible for a tax credit. Details about these types of tax credits are available at: www.energysavers.gov. **Locate last year’s tax return: You may need to reference important information for this year’s return. Direct indexing offers investors the opportunity to purchase shares of the component companies of an index itself, rather than a mutual fund or ETF tracking the index, creating opportunities for tax-loss harvesting when the prices of individual companies within the index fall.

Because of the previous inability to purchase fractional shares and the transaction costs of buying each company in an index, this strategy was generally only available to those with significant assets (in addition, those in higher tax brackets would also get more benefits from the tax-loss harvesting). But with the now-wide availability of fractional share purchases and zero-fee transactions, direct indexing has been opened up to a wider range of investors. And now, Fidelity plans to take the next step by offering its Fidelity Managed FidFolios direct indexing products to individual investors with as little as $5,000 to invest. Investors will initially be able to choose from three account strategies: U.S. Large Cap, International, and Environmental Focus. The latter strategy represents a potential growth area for direct indexing platforms, with Environmental, Social, and Governance (ESG) and Socially Responsible Investing (SRI) becoming increasingly popular. Rather than relying on the ESG/SRI criteria of a given mutual fund or ETF, direct indexing allows investors to customize the index for their particular preferences (e.g., removing gun manufacturers or tobacco companies). The FidFolios will have an initial expense ratio of 0.40%, creating a fee hurdle to overcome (compared to index ETFs which have expense ratios near zero) through its tax advantages and/or its customization abilities. Below is a case study from AIG about how to maximize income during the early years of retirement. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed