In our last blog post, we described three phases of retirement spending - Go-go, Slow-go, and No-go. Now we will show you how the actual retirement spending might look like.

Retirement Spending Smile

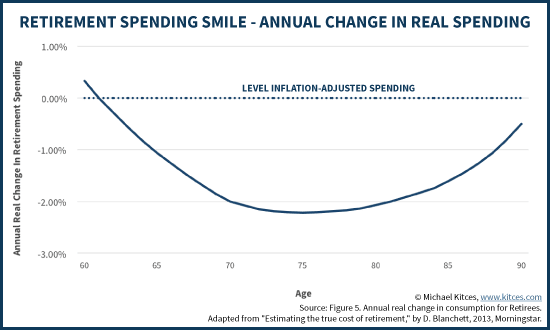

David Blanchett of Morningstar used the Rand Health and Retirement Study, which provides some longitudinal data on retiree spending behaviors over time and found that real retirement spending declined a little at the beginning of retirement, accelerated its decline in the middle retirement years and then slowed its decline again in the final decade, in a pattern that was dubbed the retirement spending smile.

Retirement Spending Smile

David Blanchett of Morningstar used the Rand Health and Retirement Study, which provides some longitudinal data on retiree spending behaviors over time and found that real retirement spending declined a little at the beginning of retirement, accelerated its decline in the middle retirement years and then slowed its decline again in the final decade, in a pattern that was dubbed the retirement spending smile.

Implication of 3 Phases of Retirement Spending

a. Composition Changes

While the total actual spending declines slightly each year, the composition of retirement spending changes quite significantly over time. For example, as retirees age, some spending categories steadily decline, e.g., insurance premiums, as life insurance, disability insurance and, eventually, automobile insurance become less necessary; transportation, as the household consolidates to one or even no cars; housing, as spending on new furniture and other household goods slows down; and clothing. Other categories, meanwhile, rise — most notably, health care.

b. Health Care Cost Rises, But Not That Much

We now know two things - 1) total retirement spending declines year after year; 2) health care costs rise year after year. This means that even though health care costs increase in later stage of life, the increase is not significant enough to push up the total retirement spending.

c. More Realistic Retirement Spending Budget

If you want to plan your retirement spending, it probably makes more sense to break the expenses into several major categories - basic spending (expenses you can't escape from), discretionary spending, health care, and taxes, then you can make different annual percentage change assumptions for these different categories of expenses.

RSS Feed

RSS Feed