In our last blogpost, we discussed how to be prepared to live longer. Now the third way to protect your retirement income.

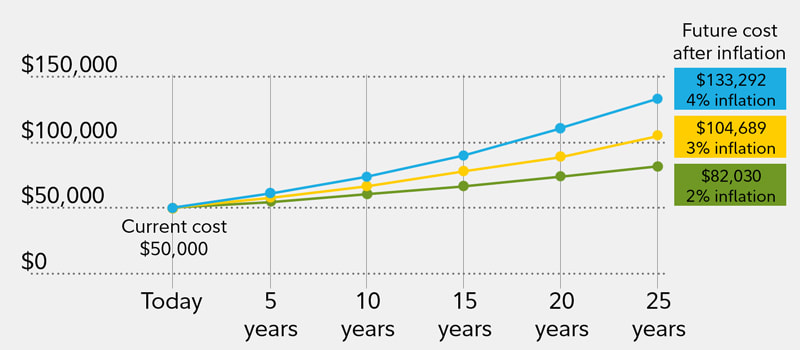

3. Be Prepared for Inflation

Inflation can eat away at the purchasing power of your money over time. Inflation affects your retirement income by increasing the future costs of goods and services, thereby reducing the future purchasing power of your income. Even a relatively low inflation rate can have a significant impact on a retiree's purchasing power.

Consider cost of living increases: Social Security and certain pensions and annuities help keep up with inflation through annual cost-of-living adjustments or market-related performance. Choosing investments that have the potential to help keep pace with inflation, such as growth-oriented investments (e.g., stocks or stock mutual funds), Treasury inflation-protected securities (TIPS), real estate securities, and commodities, may also make sense to include as a part of an age-appropriate, diversified portfolio that also reflects your risk tolerance and financial circumstances

In our next blogpost, we will discuss the fourth way to protect your retirement income.

3. Be Prepared for Inflation

Inflation can eat away at the purchasing power of your money over time. Inflation affects your retirement income by increasing the future costs of goods and services, thereby reducing the future purchasing power of your income. Even a relatively low inflation rate can have a significant impact on a retiree's purchasing power.

Consider cost of living increases: Social Security and certain pensions and annuities help keep up with inflation through annual cost-of-living adjustments or market-related performance. Choosing investments that have the potential to help keep pace with inflation, such as growth-oriented investments (e.g., stocks or stock mutual funds), Treasury inflation-protected securities (TIPS), real estate securities, and commodities, may also make sense to include as a part of an age-appropriate, diversified portfolio that also reflects your risk tolerance and financial circumstances

In our next blogpost, we will discuss the fourth way to protect your retirement income.

RSS Feed

RSS Feed