The fixed index annuity products usually offer a powerful combination of benefits that help protect against many of today's common retirement concerns, as summarized in the chart below.

|

|

|

The fixed index annuity products usually offer a powerful combination of benefits that help protect against many of today's common retirement concerns, as summarized in the chart below.

0 Comments

GuaranteeShield from American Equity

Many retirement portfolios continue to be impacted during these uncertain times. Here is a product from AIG that you can secure an income base that is guaranteed to double after 10 years when the rider has not been activated. And when you are ready for income, you can count on up to 5.6% withdrawals for life. The financial planning magazine has a great and easy to read article that properly titled "A skeptic takes a second look at Single Premium Immediate Annuities (SPIAs)".

The author went from being a skeptic of SPIA to identifying the right people for SPIAs, and analyzed the Pros and Cons of SPIA. Pros of Single Premium Immediate Annuities:

It's a great read for people who are withdrawing for their portfolios wanting some longevity insurance, as SPIAs can make sense as part of the solution. In last blogpost, we discussed traditional annuities. Now we will discuss Income Annuities.

Income Annuities There are types of annuities that are expressly designed to provide a guaranteed income stream in retirement – income annuities. And although income annuities share some similarities with their traditional counterparts, they differ in important ways. Income annuities are designed for the sole purpose of providing a guaranteed stream of income, either immediately or in the future. An immediate income annuity typically is purchased with a single premium or “purchase payment” and requires that income payments begin within 12 months of the date your contract is issued. Income can be guaranteed for as long as you live or for a specific period of time. Because immediate income annuities guarantee a specific income amount, they offer very limited access to withdrawals, and only for some annuity options. Even if you choose an annuity option that allows withdrawals, it’s important to remember that withdrawing money from your contract can have a significant impact on the dollar value of future annuity payments. An immediate income annuity may be worth considering if you are nearing or already in retirement; want the security of guaranteed, predictable income; and need that income to start right away. If you think you might need that money down the road and you have limited additional liquid assets, an immediate income annuity is probably not the best choice for you. A deferred income annuity, on the other hand, is designed to provide guaranteed future income. A deferred income annuity generally permits multiple “purchase payments” over a period of time. On the annuity date you choose, all purchase payments are combined into a single, guaranteed income stream that will continue for as long as you live; some deferred income annuities offer period certain options as well. In this sense, a deferred income annuity can be used to generate a “pension-like” stream of future guaranteed income. A deferred income annuity differs from a traditional deferred annuity in important ways. In general, a deferred income annuity:

So which annuity should you consider? That depends on many factors. For retirement purposes, an annuity can work in conjunction with the savings in your 401(k) plans or IRAs (both of which can be affected by market ups and downs). And given the way life spans are stretching, there’s also a chance you may outlive your savings. An annuity can also work to supplement other sources of retirement income that are guaranteed, like a defined benefit pension plan or Social Security. With any annuity, it’s important to get the facts before making your decision. Retirement is your reward for decades of hard work—and part of that work is making sure you’ll have enough money for the kind of retirement you want. If you are looking for an additional source of predictable income now or in the future or a product that is designed to help you accumulate assets on a tax-deferred basis, annuities may be an option worth exploring. Retirement income can come from a number of financial sources; some guaranteed, some not. Annuities are an option for people who want to bulk up the guaranteed income portion of their retirement portfolio.

Generally, an annuity works like this: You purchase the annuity, either in a lump sum or a series of payments. In return, the annuity will make payments to you at a future date or series of dates. Annuities come in many different “flavors” – each of which is designed to help you achieve specific financial goals. They can work to build retirement savings, supplement other forms of retirement funding, or both. The different varieties of annuities can also be bewildering. Depending on individual circumstances, many people turn to a financial professional to help them navigate the choices. Traditional deferred annuities “Traditional” deferred annuities are the kinds of annuities with which most people are familiar. They are designed to help you accumulate assets on a tax-deferred basis as you save for long-term goals like retirement. Let’s look at two basic examples of traditional deferred annuities: “fixed” and “variable”. Deferred fixed annuities are “fixed” because they offer fixed interest rates. They are “deferred” because they require a waiting period before annuity payments can begin. During the deferral period, money in your contract is credited with a fixed rate of interest and grows at a steady pace. Because you don’t pay current income taxes on the earnings in your contract until you withdraw it, more of your money remains available to benefit from that steady growth. Fixed deferred annuities also offer annuity income options that can provide guaranteed income for life or a certain period of time (like 10 or 20 years). This type of annuity typically includes a withdrawal provision that allows you to access the money in your contract. It’s important to understand, however, that withdrawals may be subject to surrender charges, income tax, and even tax penalties. A fixed deferred annuity may be worth considering if you are looking for a conservative way to grow a portion of your assets and avoid market volatility. It may not be the best choice if you prefer greater growth potential (and don’t mind taking on the risk that goes with it) or if you need income that starts right away. Variable deferred annuities – Unlike fixed annuities, variable annuities are built to provide financial market exposure. Variable annuities generally offer a broad range of investment options – from more conservative fixed accounts to riskier growth options. Like a fixed deferred annuity, the money in a variable annuity also benefits from tax deferral. You don’t pay current taxes on earnings in your contract until you withdraw them – which means more of your money remains available to benefit from potential growth. A variable annuity also offers a variety of options when it comes to receiving income – including lifetime income options. Of course, greater growth potential involves more risk. A variable annuity can increase or decrease in value, depending on how financial markets perform. When considering a variable annuity, it’s essential to understand how the annuity works, including associated fees and expenses as well as the surrender charges, income tax and tax penalties that typically apply to deferred annuities. Just as important, you should have a clear sense of your financial goals and tolerance for risk. A financial professional can help you make an informed decision on whether a variable annuity is right for you. In next blogpost, we will discuss Income Annuities. Everyone needs residual income protection. If you can work only part time, you will still need your full-time incomes. This article below from Standard highlights the differences between the Basic and Enhanced Residual Disability riders to help you find the appropriate rider. Below is a flyer from AIG about how fixed annuities could be looked at using the consumption framework. It's a good read for anyone who is seriously thinking about retirement. You know that offering guaranteed income solutions can help complement a portfolio and instill confidence in your retirement plans. But some people, like those who plan to draw income based on returns from mutual funds and other assets in their portfolios, may not see the value guaranteed solutions offer. Unfortunately, there’s no way to predict how those investments will play out over time, especially in the face of life’s uncertainties. When evaluating investment options, consider guaranteed options such as Protective® Guaranteed Income Indexed Annuity. This product offers three guarantees to help people strengthen their retirement portfolios with predictable income they can count on. Below is a Protective flyer for its agents to use, if you are interested in this product, you can contact us here. In last blogpost, we discussed the difference for a spouse to be an annuity's joint owner or beneficiary. Now we will analyze the issue, also show you why a parent-child joint ownership of annuity also hurts you -

Joint Ownership Issues As stated before, required minimum distributions must begin at the death of any owner which means that when the first joint owner dies, the annuity must begin making distributions. The only exception is if the surviving spouse was named beneficiary, they could continue the annuity without current distributions. There is no real benefit to joint ownership as it does not extend the life of the annuity and it can be a detriment to continuing the annuity when the first owner dies. Many individuals believe that since they own their other property jointly, they should also own their annuity jointly. The better way to go would be to have each spouse name their spouse the beneficiary rather than making both spouses co-owners. Naming the spouse as beneficiary would allow a better tax outcome. Parent-Child Joint Ownership If a parent purchases a joint annuity with their child, the parent and child will own equal shares. A withdrawal requires two signatures and distributions are made out to both parent and child. If the parent paid the premium, they have just made a gift to their child of half the value of the annuity. If the parent wants to make a withdrawal, one half the distribution will be taxable to the child regardless of who receives the money. If the child is under age 59 ½ then the entire amount distributed is subject to a 10% penalty. If the parent owns the annuity jointly with a child or grandchild, making the child the co-owner makes no real difference in postponing distributions. If the child dies before the parent, the parent would be forced to begin liquidating the annuity even if they had supplied the money. The Bottom Line In most cases, using joint ownership only hurts the ability to sustain tax-deferred growth. Most owners think joint ownership will allow the annuity to continue until the second death and that they will obtain additional tax-deferred growth. In actuality, it is just the opposite. When the first owner dies it can trigger the required minimum distributions. Q. What is the joint ownership issue with an annuity?

A. Annuities provide excellent investment vehicles and tax-deferred growth. If you take two investment accounts with the same assets and one is taxable and one is tax-deferred, the tax-deferred account will always do better because it is not paying taxes until the money is distributed from the vehicle. Annuities are treated similarly to IRAs and qualified plans. The additional advantage of a non-qualified deferred annuity is that unlike a qualified plan or an IRA, no required minimum distributions need to be made during the life of the owner. Once the owner dies, the annuity must begin making post-death distributions to the beneficiary. Under IRC Section 72(s), upon the death of any owner, the annuity must begin to make post-death distributions to the beneficiary. The Tax Reform Act of 1986 changed the joint ownership of annuity taxation rules to prevent using joint ownership to avoid taxation of the annuity over two lives. This makes annuities distributable whenever one of the owners dies. However, if the other spouse is named as beneficiary, the taxation would then be postponed. When a surviving spouse is named the beneficiary of the non-qualified annuity, they may continue the annuity in their name. This is very similar to a spousal IRA rollover allowing the surviving spouse to continue to receive tax-deferred growth. If one spouse is the owner but names their spouse as the beneficiary, then the spouse who is named beneficiary can continue the annuity and continue to receive tax-deferred growth in the annuity. In next blogpost, we will analyze why a joint parent-child ownership also hurts you.. MYTH 1: Consumers hate annuities

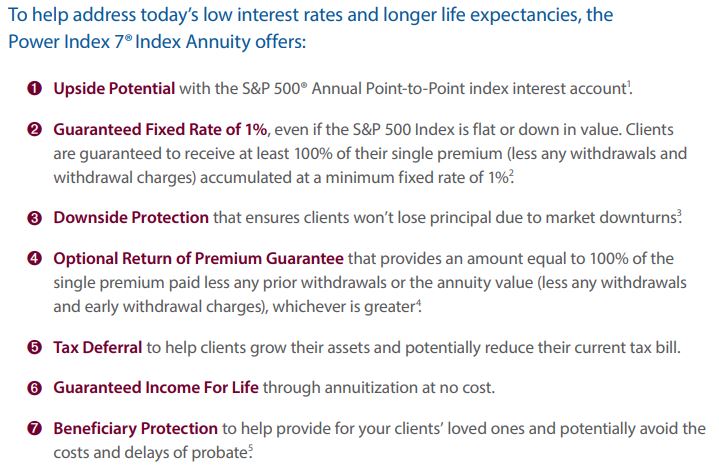

Truth: Although some people may not fully know the benefits of annuities, or hold outdated, incorrect opinions, a growing number are becoming educated and are choosing to add fixed indexed annuities (FIAs) to their retirement plans. In fact, recent annuity sales are shattering previous records. According to the LIMRA Secure Retirement Institute, FIA sales were $20 billion in the second quarter of 2019, 14 percent higher than prior year results. Indexed annuity sales are expected to grow by double digits to about $96 billion by the end of 2023, a 38 percent gain over 2018. Those who understand the benefits FIAs can provide — income protection and stability with little or no maintenance — are not surprised. MYTH 2: Annuities are not an accumulation vehicle Truth: With the innovation of uncapped crediting strategies, this is no longer true. Consumers can take advantage of a positive index performance without worrying about another 2008. An indexed annuity with a decent participation rate will help significantly reduce clients’ risk, but also give holders the growth they need. In fact, according to a study on traditional asset allocation conducted by Roger Ibbotson and Zebra Capital Management, FIAs help control financial market risk, mitigate longevity risk, and will likely outperform bonds over time. MYTH 3: Annuities are unnecessary with proper asset allocation Truth: The Ibbotson and Zebra Capital Management study also showed that “a major advantage of an FIA is the ability of the insurance provider to ‘transform’ equity returns into a more ‘tailored’ return/risk profile (eliminating downside risk and providing an opportunity for interest earnings based upon a portion of equity returns). This downside protection is very powerful and attractive to many individuals planning for retirement. Additionally, with today’s low interest rate environment coupled with experts’ modest expectations for bond returns in the near-term, FIAs should be considered. If you are concerned about low interest rate and long life expectancy, index annuity could be a solution, see 7 reasons cited by AIG for its Power Index 7 product below -  Please contact us if you are interested in annuity products.

As you approach retirement, you want to protect your savings from market losses. A Lincoln fixed indexed annuity offers the potential for growth beyond that of a traditional fixed annuity, since the indexed accounts have earnings tied to the performance of an outside index. When the index increases over the indexed term, the account will be credited with earnings determined by that account’s crediting method. But what happens if the index performs poorly and has a negative return? The “power of zero” gives the client protection – the indexed account will never decrease due to negative performance…the lowest return is 0%. In our last blogpost, we discussed factors to consider when purchasing QLAC. Now the question - which carriers have the best QLAC products? We recommend products from AIG, Lincoln, and Principal. Below is up-to-date information about AIG's QLAC product, including producer and consumer guides, sales ideas, fact sheets, and more. If you are interested in the other carriers' QLAC products, please contact us. In our previous blogposts, we discussed what is QLAC and showed an example of QLAC. Now we will discuss what factors to consider before purchasing QLAC.

The decision to purchase a QLAC is a personal one and should take into account your family's needs and financial goals. For instance, you may not want to take RMDs on the entire pretax balance of your IRA if doing so would provide you with more income than you need. But will your financial standing be as strong 20 or even 10 years from now? A QLAC would allow you to enjoy your earlier retirement years knowing that you have guaranteed income in place when you really might need it. Specifically, the following QLAC related decisions should be considers. Single or joint life? If you are married, you can choose a joint contract, which will provide income payments that will continue for as long as one of you is alive. Choosing a joint contract may decrease your income payments—compared with a single life contract—but may also provide needed income for your spouse should you die first. Include a cash refund death benefit? When purchasing a QLAC, the income lasts for your lifetime (joint contracts pay income for you and your spouse, as long as one of you is alive). You may also want to consider adding a cash refund death benefit. This provides for a lump sum paid to your beneficiaries if your lifetime payments do not exceed the dollar amount you invested in the QLAC. While a contract without the cash refund death benefit may provide higher income payments, it does not include beneficiary protection for your heirs. When to start income? A QLAC should be part of a broader income plan, to help ensure that your essential expenses like food, health care, and housing are covered during retirement—ideally with lifetime income sources such as Social Security, a pension, or lifetime annuities. Deciding on an income start date will depend on how this income stream will best fit into your overall plan. Here are some hypothetical examples of how someone might choose an income start date:

Need to change the income start date? For contracts that include a cash refund death benefit, you typically have the ability to change the income date by up to 5 years in either direction (subject to an age-85 maximum). For example, if you initially select age 78 as your income start date, you could subsequently change this date to any time from age 73 to age 83. Of course, the amount of income that you will receive will typically be adjusted to a lower amount if you decide to change the date to an earlier age, and a higher amount if you change the date to a later age. In our next blogpost, we will show you some of the best QLAC providers. In our last blogpost, we discussed what is QLAC, now we will show how to use QLAC to create steady later in life income streams.

Let's say you own one or more traditional IRAs with a total balance of $200,000 as of December 31 of the previous year. You would be limited to using $50,000, which is 25% of $200,000 and is less than $135,000, to fund the QLAC. But if your total IRA balance is worth $540,000 or more, the maximum you can contribute to a QLAC is $135,000. Keep in mind that in both cases the money that remains in your IRA or 401(k) is still subject to RMDs. An Example Let's assume a woman is approaching age 70½ and does not need her full RMD to cover current expenses. By investing a portion of her traditional IRA assets in a QLAC at age 70, she would not have to take RMDs on the assets invested in the QLAC, and she would receive guaranteed lifetime income starting at a date of her choice, up to age 85. During the deferral period, she would rely on Social Security, RMDs from the remaining money in her IRA, withdrawals from investments, and other income, such as part-time work or a sale of a business, to cover expenses. If she invests the $135,000 in a QLAC and defers to age 80, her guaranteed income would be $15,200 a year no matter what happens over time, and she would receive a total of $228,000 in payments if she lived to age 95—or more if she lived longer. In our next blogpost, we will discuss what factors to consider if you should purchase QLAC or not. Q. What is QLAC?

A. A QLAC is a Deferred Income Annuity (DIA) that can be funded only with assets from a traditional IRA or an eligible employer-sponsored qualified plan such as a 401(k), 403(b), or governmental 457(b). The US Treasury Department issued a rule creating Qualified Longevity Annuity Contracts (QLACs) in 2014. QLACs allow you to use a portion of your balance in qualified accounts—like a traditional IRA or 401(k)—to purchase a deferred income annuity3 (DIA) and not have that money be subject to RMDs starting at age 72. At the time of purchase, you can select an income start date up to age 85, and the amount you invest in a QLAC is removed from future RMD calculations. QLACs address one of the biggest concerns among individuals in retirement: making sure they don't outlive their savings. Why Purchase QLAC? There are two main reasons. First, you can delay required minimum distributions (RMDs) on the money in your QLAC. Without a QLAC, you would be forced to start taking distributions based on the total value of that retirement account at age 72 (formerly 70 ½) - and paying income tax on those distributions. Many people don’t need distributions at that age, and don’t want to pay tax on that money yet. With a QLAC, you won’t have any RMDs on premiums paid until age 85. Second, longevity. If you are worried about outliving your funds, a QLAC solves the problem. It provides guaranteed monthly income as long as you live. Plus, you get the amount you were promised at purchase, no matter what’s happened to the stock market or interest rate in the interim. You're effectively transferring that risk to the insurer. In our next blogpost, we will show you a few QLAC examples about how it works. Q. Will the Secure Act bill mean I could find annuities in my 401(k) plan?

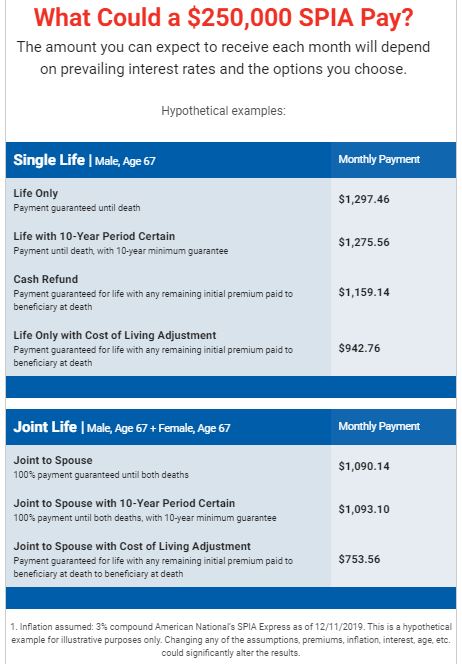

A. Based on an article at Barron's, one provision of the bill eases the path for employers to offer annuities as part of their retirement plans by providing safe-harbor language that takes them off the hook if an insurer whose products they use runs into financial trouble. (The employers continue to have fiduciary duty in picking appropriate products, or annuities in this case.) Academics have long discussed the merits of having some sort of guaranteed income option inside plans to help retirees when they start drawing on their nest egg. The concern is that the bill leaves the door open to all sorts of annuities, not just the low-cost, simple ones academics favor. Policy watchers would have liked some framework for what annuities are allowed in a plan. As for when retirement savers will find such options in their plans, State Street's Kahn recommends thinking along the lines of evolution, rather than revolution. Employers have been looking at all sorts of guaranteed lifetime-income options and financial-services companies have been working on solutions for years, including target-date funds that incorporate some sort of guaranteed income option, Kahn says. If nothing else, the bill will likely bring attention to the need for providing some sort of guaranteed income stream for retirees beyond Social Security. The product highlights below show how Protective Guaranteed Income Indexed Annuity provides three times the guarantees with: Guaranteed Income for Life Fueled by a 4% roll-up to the benefit base (which can double in 15 years) thanks to opportunities for bonuses along the way. Guaranteed Rate Cap for Term A guaranteed rate cap that won't change for the term so you will never be surprised by a lower renewal rate during the withdrawal charge period. Guaranteed Flexibility Two unique income options chosen at benefit election, with access to competitive withdrawal rates at key ages both now or later. If you are interested in knowing how much your $250,000 could lead to lifetime payment, below is a table from American National showing you an hypothetical example -  Q. Why every retiree should consider a Single Premium Immediate Annuity product in his or her retirement portfolio?

A. SPIA should be considered by every retiree for two reasons: 1. Eliminate Longevity Risk A SPIA is an excellent way to reduce the fear of running out of money. It can allow an individual to spend the growth in their portfolio on travel, new cars, hobbies and other activities of daily living that occur in retirement. Retirement has become a new Life Stage and people want to enjoy retirement but it takes income to do so and a SPIA provides that income and they will receive it as long as they are alive. 2. Avoid Unnecessary Losses in a Down Market By covering fixed and necessary living expenses with a SPIA, an individual has reduced the risk of loss in retirement portfolio. They no longer need to sell off assets in a downmarket in order to fund everyday living expenses. Their social security and Immediate annuity income cover all those necessary expenses. The Power Series of Index Annuities® with the Lifetime Income Plus FlexS guaranteed living benefit (GLB) rider provide with the flexibility to take Required Minimum Distributions (RMDs) without eliminating rollups or locking in withdrawal rate for life. See a hypothetical example below - income is guaranteed to grow for the first 10 contract years, even after RMDs begin. Plus, you can wait until you’re in a higher withdrawal age band to activate your rider and lock in more income for life. Grandparents can pass retirement income to grandkids. The document below shows how to make it happen. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed