The document below is a good description of QLAC and how to grow protected lifetime income while you defer RMDs.

|

Q. Why people usually advise wait until 70 to take social security benefits?

A. It's because you will be buying the best annuity in the world! Here is an example with numbers to illustrate: Consider someone who is age 66 right now, if she delays taking social security until she is age 70, she will have to pull about $36,000 annually from her savings over the 4 years in order to replace the benefits that she would have gotten if she claimed. In return, however, when she does claim at age 70, she will get a monthly benefit that is $1,040 higher than it would be had she claimed at age 66. To buy that $1,040 monthly payment with inflation protection as an annuity in the private market, it will cost her $252,000! So in return for using $150,000 for 4 years, she would get a government annuity that is worth $252,000, that is a discount of 40%! First, What Is DIA? Is your mindset turning toward how to safeguard your retirement standard of living for many years ahead? A deferred income annuity (DIA) provides protected lifetime income in the future. While the income stream can be started as soon as 13 months after purchase, it also can be delayed for a long time (40 years in some cases). Bottom line: The longer the deferral period, the larger the income payout amount. Next, What is QLAC? A qualified longevity annuity contract (QLAC) is a special type of DIA and it brings added advantages. It allows traditional IRA owners and defined contribution plan participants to ignore the QLAC funds in those accounts when calculating their RMDs. As long as the QLAC distributions are delayed, the associated Required Minimum Distributions (RMDs) and taxes are too. 2 Reasons why a QLAC stands out for modern retirements include:

Overview Flexible premium. May include a first year interest rate enhancement. 10% surrender charge free withdrawals each contract year. 7 year surrender period. PRINCIPAL GUARANTEE FEATURE The Minimum Guaranteed Surrender Value is return of premiums paid less any cumulative withdrawals. INTEREST RATE ENHANCEMENT American National may offer an interest rate enhancement on all premium payments received in the first 36 months of the contract for one year. This enhancement is not guaranteed and is subject to change. INTEREST RATE GUARANTEE The declared annual effective interest rate for the initial premium and each subsequent premium payment will be guaranteed for two years from the date the premium payment is received. After two years, the interest rate is declared annually. MINIMUM GUARANTEED INTEREST RATE: NAIC Index. See rate sheet for current rate. RATE LOCK: 60 days for 1035 Exchanges, CD Rollovers, Mutual Fund Transfers and Institutional Transfers SURRENDER CHARGE SCHEDULE: Year 1 2 3 4 5 6 7 8+ % 7 7 7 6 5 4 2 0 SURRENDER CHARGE FREE WITHDRAWALS 10% of annuity value as of the beginning of each contract year, including first year SURRENDER CHARGE WAIVERS*

In last blogpost, we discussed how does DIA work, now we will discuss how to determine if DIA is right for you.

Does DIA Make Sense For You? These DIA products tend to be most beneficial for pre-retirees between the ages of 55 and 65 who are planning to retire in 5 to 10 years. In addition to reducing market and longevity risk—an advantage of all fixed annuities—DIAs have the following advantages over immediate annuities:

If you are interested in DIA or other annuity products, please contact us. In last blogpost, we showed you a case study how DIA could be combined with 401k to create secure retirement income. Now we will explain how DIA works.

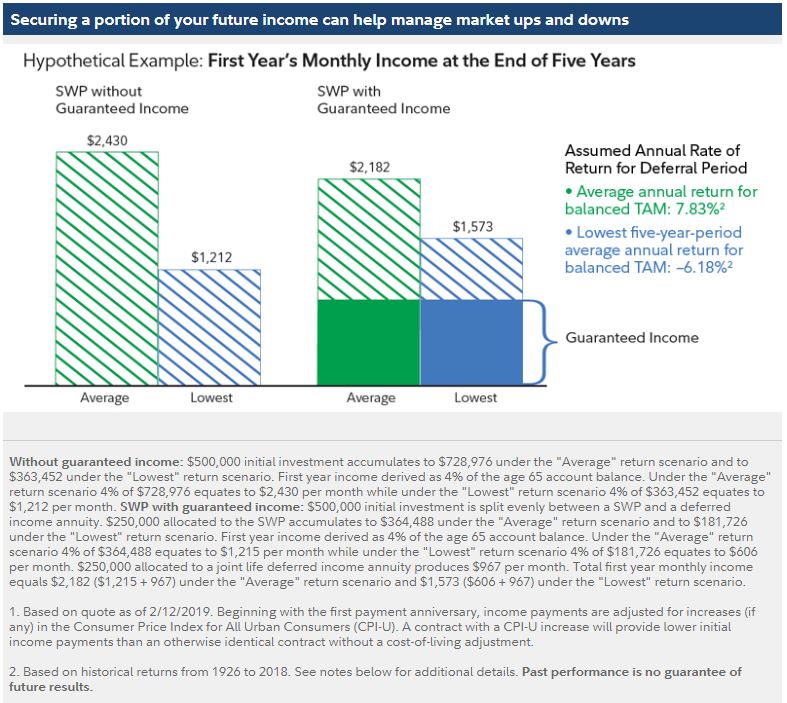

How Does DIA Work? Income annuities are different from other investment options because they offer longevity risk pooling (referred to as mortality credits). Effectively, assets from annuitants with shorter life spans remain in “the mortality pool” to support the payouts collected by those annuitants with longer life spans. Put simply, the longer you live, the more money you will receive. This is why it is so challenging for an individual investor to replicate this income stream. DIAs are able to leverage the mortality credits and turn a portion of your savings into a stream of income beginning anywhere between 2 and 40 years that will last over your lifetime. By investing in a DIA you are starting the planning process ahead of your retirement age. In return for investing early, you are potentially securing a higher income amount than if you waited and invested in an immediate income annuity. Why Guarantee Your Income? Guaranteed income products serve a very particular purpose. They can shift some key retirement risks--longevity and market risk—off your shoulders and onto the issuing insurance company. When you buy a DIA, you shift the risk of outliving your income to the insurer, who promises to pay you a certain amount of income for either a predetermined period of time or the rest of your life. The insurer also assumes the interest and market risk associated with your DIA investment; even if the market and interest rates are down significantly during your deferral period, you still get the same guaranteed rate of income. However, DIAs, like any investment product, aren't right for everyone. There is an element of trading growth potential for a guaranteed future lifetime income stream. Part of that trade-off is giving up some flexibility (access), which is why it’s better to allocate a portion, rather than all, of your savings to a DIA. The amount you commit to a DIA is irrevocable, but the tradeoff is being confident that your income will be there when you need it. In our next blogpost, we will discuss how to determine if DIA is right for you. In last blogpost, we showed you what is DIA and its advantages. Now we will use a case study to show its value. Consider a hypothetical example of how a DIA might work under different market conditions. Imagine a 60-year-old couple with a hypothetical retirement portfolio of $500,000 who wants to generate income starting at age 65. The example below illustrates 2 different ways of creating income: Option 1 The couple decides to invest their $500,000 in a balanced target asset mix (TAM) (50% stock/40% bonds/10% short term), then starts taking income at age 65. The plan is to use only a Systematic Withdrawal Plan (SWP) with an initial 4% annual withdrawal rate and payments increasing 2.5% on each payment anniversary thereafter. Option 2 The couple decides to diversify and splits the $500,000 as follows: (1) $250,000 is invested in a balanced TAM for 5 years; then, at age 65, income is taken using a SWP with an initial 4% annual withdrawal rate and payments increasing 2.5% on each payment anniversary thereafter; and (2) $250,000 is used to invest in a joint life deferred income annuity contract with a cash refund and Consumer Price Index (CPI) cost-of-living adjustment (COLA), with payments starting at age 65.  As you can see, assuming average historical returns for the balanced TAM, the portfolio with the guaranteed income generated first-year monthly income that is $248 less than that generated from the portfolio without the guaranteed income. Because deferred income annuities are not exposed to market volatility, the income amount remains consistent regardless of a market downturn. Therefore, when historically low returns are assumed in the example, the portfolio with the guaranteed income outperformed the portfolio without the guaranteed income—generating first-year monthly income that is $361 higher.

One of the strongest reasons to buy a DIA is the foundation it provides for your retirement income plan. You establish a guaranteed level of income no matter what happens over the next several years, and are one step removed from the anxiety of watching the markets move every day with your retirement in sight. Another consideration with deferred income annuities is the ability to invest incrementally over time by making additional payments. While most income annuities only allow a single investment, DIAs allow you to make additional investments to the annuity before your income payments—each additional investment subject to the interest rates available at the time of purchase—so you can increase your retirement income stream. By building your income plan in increments, you can stagger your investments with a range of interest rates and possibly take advantage of higher interest rates. In next blogpost, we will discuss how does DIA work. With pensions increasingly a thing of the past, most Americans now need to build their own streams of income for a retirement that could last decades. The success of your individual retirement income plan will rely on 2 key factors:

The Solution - Deferred Income Annuity (DIA) That's where guaranteed income annuities may be able to help. These products are able to deliver a stream of income that you can rely on for either a predetermined period of time, or for the rest of your life. And, specifically, deferred income annuities (DIAs) let you lock in a stream of guaranteed income years before retirement, while reducing the effect of market volatility on your retirement income plan. The Advantages of a DIA The advantage of a DIA is that it offers a degree of certainty. You can secure a portion of your retirement income years before entering retirement so you don't have to wait until the moment you retire to know what your investment will deliver in income. You can gain peace of mind and some flexibility with your other assets. For some, using a portion of retirement assets to lock in guaranteed income for the first several years of retirement is an attractive option; knowing the income is secure, some investors may have the confidence to invest part of their retirement assets more aggressively during those early years. While DIAs are an efficient way to generate income, keep in mind that you are giving up access to the assets you dedicate to this solution and the opportunity for potential market performance. In next blogpost, we will show you a case study how DIA combined with your 401k investment could provide secure retirement income. A single premium tax deferred fix annuity is a good option for retirees seek fixed income. American Pathway SolutionsMYG offers:

Please see the product flyer below for more details: Saving and paying for college can be a challenging goal and you may be among the many people who worry about the financial pressure that funding higher education can bring. Thankfully for parents and grandparents, it's never too early to start saving and there are many options to help you prepare for one of the most important milestones in the lives of your children or grandchildren.

529 plans A common option used for paying for college and educational expenses is a 529 plan, which is an education savings plan sponsored by a state or state agency. A 529 plan can be purchased not only by parents, but also grandparents and other relatives. When you purchase a 529 plan, your earnings grow tax-deferred and any qualified withdrawals are tax-free. As a child reaches college age, he or she can use the accumulated funds to pay for qualified expenses including tuition, room and board, books and computer equipment. While 529 plans have many advantages and can be useful in preparing for the future, there are limitations to consider as well. Limitations of 529 plans include:

Plus, if your child receives a scholarship, you will likely only need a portion of the money saved in your 529 plan. If you end up with remaining funds or if a child decides not to enroll in school, the beneficiary can be changed to another family member. However, if you do not have other family members looking to attend, you may have to pay significant penalties to withdraw your savings for other purposes, depending on the rules of your state's 529 plan. Using an annuity One tool to consider as part of an overall college saving strategy is a fixed or fixed indexed annuity. A significant benefit of these products is your account value can grow tax-deferred and is protected from downside market risk. So when the market is up, your money can grow, but when the market is down, you do not lose any of your hard-earned savings. Plus, if your child receives a scholarship or decides to pursue another path besides college, the money in your annuity can be accessed for other purposes. Keep in mind that annuities are designed to help you reach long-term savings goals. While most annuities allow you to withdraw a certain amount each year without penalty, you'll likely pay charges on withdrawals over that amount during the annuity's withdrawal charge period. This period typically ranges from five to 10 years or more, depending on the annuity. Helping pay tuition As with many financial plans, there is no time like the present to begin saving. An annuity purchased when your children are young can assist with tuition costs down the road. One option would be to purchase an annuity with a withdrawal charge period that coincides with the length of time it takes for your child to reach college age. For example, if on your child's 8th birthday you purchase an annuity with a surrender charge period that ends in 10 years; your child will be 18 and entering college. At this time, you'll be outside the withdrawal charge period, meaning you'll have full access to the annuity's value to supplement tuition payments. It's important to remember that withdrawals from an annuity may be subject to state and federal income tax. In most cases, withdrawals taken before age 59½ will also be subject to a 10 percent IRS penalty.  If you are interested in knowing more about this product from American National, please contact us.

This article below covers the 4 major retirement risks well and shows why annuity could be an effective tool to prevent these 4 common risks. New contracts reached a 10-year high as key stakeholders praised a bill before the U.S. Senate which could expand the products to more 401(k) plans.  Fixed indexed annuities (FIAs) can play an important role in one's retirement plans by offering growth potential, protection from loss due to market downturns, and the option for guaranteed lifetime income. Yet many people are less familiar with annuities in general — and FIAs in particular — than with financial products such as mutual funds. What's more, because FIAs have features of insurance and growth potential, they can seem more complicated than they really are.

In this blogpost, we answer five questions people commonly ask about FIAs, so you can make more informed decisions about adding annuities to your retirement plans. 1. How can a FIA help my retirement savings grow? The opportunity to build retirement savings is a feature of FIAs that many people find appealing. FIAs offer the potential for interest credits that are tied to the performance of a stock market index — without having to invest directly in the market. If the index rises, you will receive a portion of that increase in the form of interest credits. If it declines, you may receive zero percent interest credits — but you'll never receive less than zero. What's more, the buildup within an FIA is not taxed until it's withdrawn, similar to retirement savings vehicles such as 401(k)s and non-Roth IRAs. 2. Why won't I benefit from all of the index gain? This is a trade off: you may be willing to accept some limits on your upside potential in exchange for protection from loss due to market downturns. 3. What happens if the markets go down? Savings in an FIA won't lose money in a market downturn because they are not invested directly in the markets. What's more, FIAs lock in previous interest gains, so that growth is also protected. 4. How do I use an FIA to help pay retirement expenses? As annuities, FIAs can provide a guaranteed stream of income. Adding annuities to a retirement income plan can help build a larger retirement "paycheck" that won't fluctuate — unlike withdrawals from investments whose value rises and falls with the market. 5. Where does an FIA fit in my overall retirement plan? FIAs can help meet a number of your needs, depending on your current mix of financial products, goals and primary concerns. Here are some major benefits: o Accelerating retirement savings: Unlike 401(k)s and IRAs, FIAs have no contribution limits for non-qualified premium. This feature may be especially appealing if you are older and looking to boost retirement savings, or if you have maxed out annual 401(k) and IRA contributions. o Protection against longevity risk: Depending on the annuity, you may include an income rider for an additional fee. The rider can be used to provide a source of guaranteed income that can last a lifetime. o Tax management: Unlike withdrawals from 401(k)s and IRAs, which are fully taxable (except Roth IRAs), you only pay taxes on the interest earned in your FIA for non-qualified premium. Because the income from an FIA is typically made up of a combination of interest and the return of your original premium, only a portion of it is taxable. This feature can help you use FIA income in conjunction with fully taxable withdrawals from other sources to lower your overall tax burden in retirement. Case Study: Help Your Parents Stop Worrying

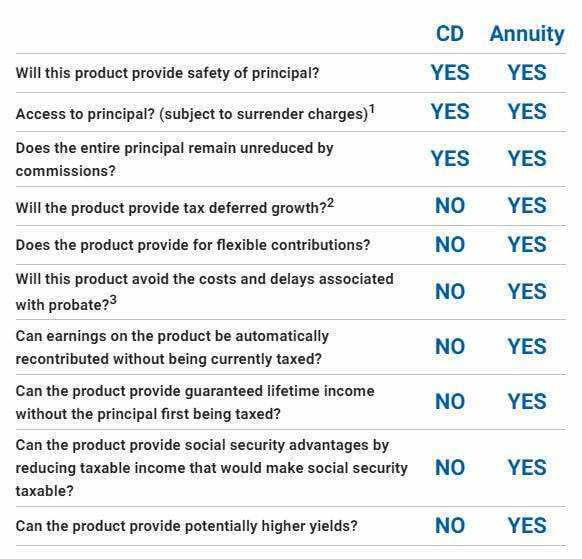

Anthony DiPaolo grew up in a poor New York neighborhood but he was happy as a child as he had a used computer his father had purchased for him that allowed him to go into his own world. After working his way through college, Anthony went to work for a Silicon Valley start-up. He was able to grow and develop his love for computers while working for a company that grew rapidly and gave out stock options. Twenty-five years later Anthony at the age of 47 had accumulated a net worth of ten million as his company was sold and his stock options paid out. Anthony would visit his parents at least once per year and would ask them if they needed anything. Each time they would tell him they were fine. On a recent trip home Anthony talked to his cousin who would check in on his parents and his cousin told him that his parents really had very little money and were not eating right as they tried to stretch their meager social security benefits. His cousin said they were too proud to ask Anthony for money. Anthony called his financial advisor back in California and asked him what he could do for his parents. He had offered them money before but they always refused. Anthony‘s advisor told him he could purchase a Joint and Survivor Immediate Annuity for his parents that would provide them sufficient funds to meet their lifestyle needs. It was money they could not outlive and they would not have to ask Anthony for money. Anthony and his agent went over the application with his parents, had them sign as annuitants, and explained to his parents that they would soon begin receiving checks each month from an insurance company that would pay for their food, clothing, housing and entertainment. Anthony’s parents were extremely proud people and did not want to ask their son to take care of them but by providing his parents a monthly income that they needed, he eliminated the need for them to ask him for money. Each month they would have enough money to meet all of their needs. Anthony could go home knowing that his parents would have the money to live on while preserving his parents pride in not having to ask their child for money. Q. Would an index annuity using an S&P 500 annual point-to-point crediting method hurt or help earnings? A. This is a fair question. For an index annuity using an S&P 500 annual point to point crediting method, it could actually help people against sequence of return risk and the cap may not have the effect on earnings as people often expect. See the document below for actual numbers. Based on a marketing flyer from American National which has a huge lineup of annuity products (see here), there are 8 ways to access money if you need it from your fixed annuity:  Q. I heard that a deferred annuity is better than CD, is it true? A. You might not realize that fixed annuities offered by insurance companies usually are better than CDs, see the CD vs Annuity comparisons below for yourself.  If you want to see further how much have insurance companies' fixed annuities' interest rates today and how they changed over the past years, please see American National's page here.

The Palladium® Single Premium Immediate Annuity from American National offers a number of income payment options and a Cost of Living Adjustment (COLA) that can be added to many of those options. INCOME PAYMENT OPTIONS

COST OF LIVING ADJUSTMENT (COLA)The Cost of Living Adjustment is an additional option that can be added to most of the available income options at the time of application. Palladium SPIA offers a 3% compounding COLA. Below are some income stream case studies from American National so you can see how other retirees take advantage of annuity products to achieve income streams. In our last blogpost, we introduced the concept of Fixed Annuity, now we will specifically discuss the Lincoln MYGA -

In our last blogpost, we introduced Lincoln Finance Group's MyGuarantee fixed annuity, now we will discuss a few general points of a Fixed Annuity:

In next blog post, we will show you more details of the Lincoln MYGA annuity.  For people who have a sizable amount of money sitting on their CD accounts, this annuity from Lincoln Financial Group - MyGuarantee Puls Annuity (MYGA) - is very simple, and the interest rate is way above the competition for the same surrender period, and certainly way more than any interest rate you could get at any bank. For example, the 5-year MYGA offers a 3.5% interest rate. If you compare that to the big national banks on Bankrate.com, and this annuity beats every one of their five-year guarantees, PLUS you can take out 10% every year penalty-free, let your money grow tax-deferred (unlike CDs), AND there’s no “re-lock” provision on the back end like many other CDs or annuities, you are truly free to do with the money what you want. You can leave it be at the new rates five years from now without locking it back in, or you can take their ball and go home… free and clear… no games. The product brochure is below and in next blogpost we will explain what is Fixed Annuity and why it's better than CD. Q. What is the difference between a longevity annuity and a deferred annuity?

A. A deferred annuity provides for an initial waiting period before the contract can be annuitized (usually between one and five years), and during that period the contract’s cash value generally remains liquid and available. Beyond the initial waiting period the contract may be annuitized, though the choice remains in the hands of the annuity policy owner, at least until the contract’s maximum maturity age at which it must be annuitized. By contrast, a longevity annuity generally provides no access to the funds during the deferral period, and does not allow the contract to be annuitized until the owner reaches a certain age (usually around 85). In other words, many taxpayers purchase traditional deferred annuity products with a view toward waiting until old age to begin annuity payouts, but they always have the option of beginning payouts at an earlier date. With a longevity annuity, there is generally no choice, but this also allows for larger payments for those who do survive to the starting period; as a result, for those who survive, longevity annuities typically provide for a larger payout (often, much larger) than traditional deferred annuity products. Most taxpayers who purchase longevity annuities do so in order to insure against the risk of outliving their traditional retirement assets. The longevity annuity, therefore, functions as a type of safety net for expenses incurred during advanced age. Where a deferred annuity contract may be more appropriately categorized as an investment product, the primary benefit of a longevity annuity is its insurance value. The flyer from AIG below shows the Power Series of Index Annuities from AIG that could act as long-term retirement solutions and potentially provide people who prepare for retirement with growth opportunities and protection from market downturns. Meet Carl. He's 65 and a former school teacher. He enjoyed his students. But he is ready to start enjoying retirement now. He's more interested in income certainty than growth. Find out how can he ensure that his money can last from the case study below. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed