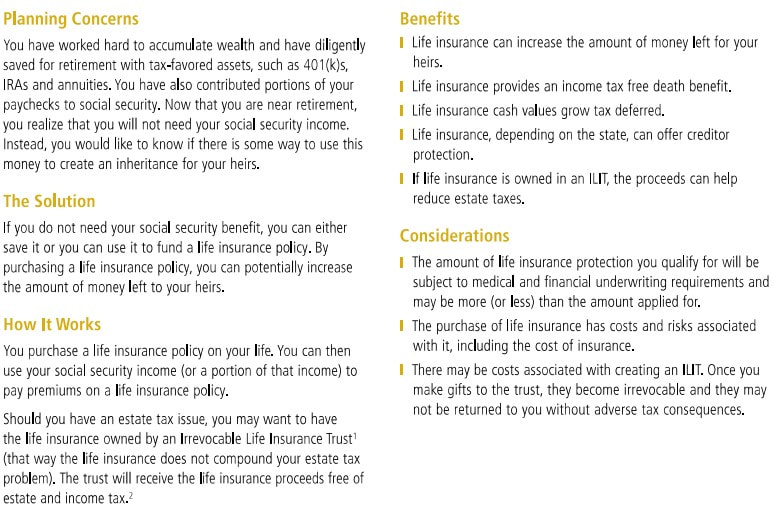

The following AIG flyer shows a scenario where one could use a combination of Term and GUL to protect from both pre- and post-retirement risks!

|

In The 2022 Policygenius Life Insurance Trend Report, 3 trends are noted.

Growth in no-medical-exam life insurance The COVID-19 pandemic has accelerated changes in consumer shopping habits, with shoppers demanding convenience and more no-medical-exam policies that allow consumers to apply for term life insurance using digital health information. According to Kartik Sakthivel, vice president and chief information officer at LIMRA, nine in 10 insurance executives surveyed in 2020 reported that their customers “have an increased appetite for the digital shopping experience,” a trend that continued into 2021. Internal Policygenius data corroborates this trend. From October to December 2021, roughly 56% of life insurance applications submitted through Policygenius were for no-medical-exam policies, compared to 26% in January to March 2021. In addition to providing convenience, accelerated underwriting policies can be more affordable options for shoppers. Policygenius Life Insurance Price Index data from the last year shows that no-medical-exam term insurance policies are competitively priced compared to term policies requiring a full medical exam — and some applicants even paid less for no-medical-exam term coverage. For example, 25-year-old females buying $250,000 in coverage paid 1.6% less in 2021 for no-medical-exam term policies than they did for traditional policies. Strong demand from younger age groups According to Mark Friedlander, director of corporate communications at the Insurance Information Institute, 2020 life insurance sales “were largely driven by younger age groups” and there was a year-over-year increase of 7.9% in life insurance sales for policyholders 44 and under from 2019 to 2020, the last year for which he has complete data. In terms of the amount of coverage purchased through Policygenius in 2021, people 18-44 bought the vast majority (84%) of policies exceeding $1 million in coverage, and 81% of policies from $750,001 to $1 million. Older Gen Xers and Baby Boomers — people age 45 to 64 — bought only 16% of policies over $1 million in coverage, and those 65 and up didn’t buy any of these policies. Compared to other demographics, Gen Xers and Baby Boomers also bought less coverage overall through Policygenius in 2021: 85% of policies bought by people over 65 and 87% of the policies bought by people age 45 to 64 were for under $250,000. Stability in life insurance pricing The life insurance industry saw a significant increase in death claims due to COVID-19 in 2020. “Death benefits paid in 2020 jumped to $87.5 billion, up 15% from $76 billion in 2019, the largest increase in nearly 25 years,” according to Friedlander. One carrier on the Policygenius platform saw a similar rise in death claims in 2020 — and an even bigger increase in 2021. Legal & General America, the parent organization of the Banner Life and William Penn life insurance companies, saw a 12% increase in death claims, measured by dollars paid, from 2019 to 2020. Death claims rose again last year, increasing 17% from 2020 to 2021. Despite this increase, as well as inflation, life insurance prices stayed consistent throughout 2021, with only nominal changes. Based on Policygenius data from April 2020 to April 2021, older smokers saw a surge in life insurance pricing, but pricing adjustments in May 2021 and the following months brought prices back to April 2020 levels. Consumers will likely continue to see price stability as insurers gather long-term data on COVID-19’s impact on mortality rates. Tax-advantaged product solutions can help clients save more for retirement and potentially grow their savings faster. Most clients may be familiar with 401(k)s and IRAs, but there's another tax-advantaged vehicle to consider for retirement planning: fixed indexed annuities (FIAs).

FIAs are insurance products that offer growth potential and guaranteed income for retirement. Funds in an FIA earn interest credits based in part on the upward movement, if any, of a reference stock market index, such as the S&P 500®. Since money in an FIA is not directly exposed to stock market risk, FIAs also provide protection from loss due to market downturns. What's more, this combination of growth potential and protection comes with tax advantages that can complement other savings and investment vehicles in your clients' retirement portfolios. Here is a look at three key tax benefits of FIAs and how they can contribute to a tax-smart approach to retirement planning.

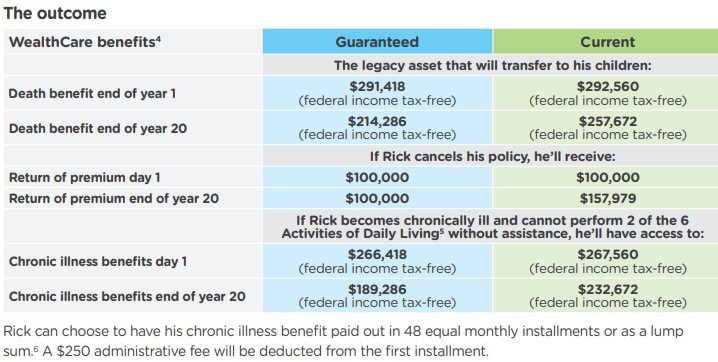

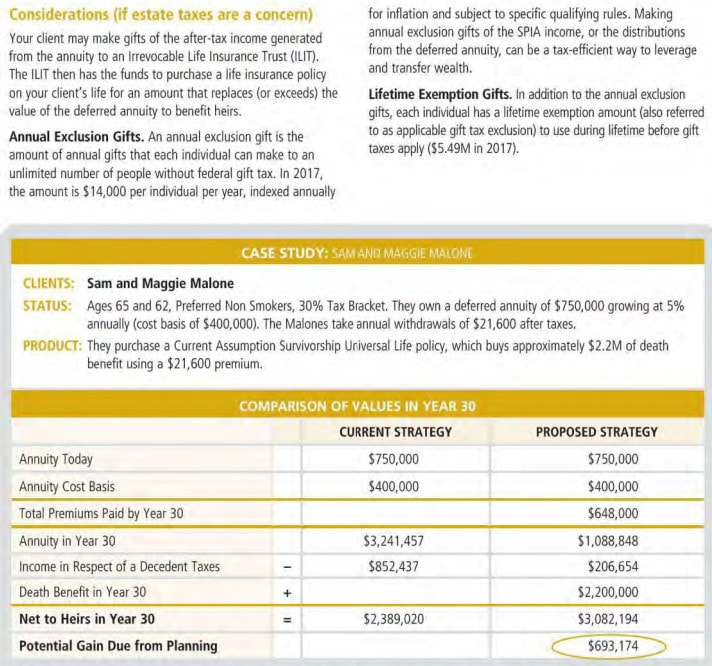

The big picture With their tax benefits and ability to provide growth potential and protection, FIAs can play an important role managing taxes within a retirement savings plan. They may complement other sources of growth potential and retirement income, including stocks, bonds and mutual funds held in taxable brokerage accounts; savings in tax-deferred accounts like 401(k)s; and other tax-advantaged vehicles such as Roth IRAs. Using a mix of these tools can be vital to helping clients minimize the effect of taxes, manage risk and provide growth potential before and after retirement. Taxes are constantly changing. And, this could lead to unanticipated tax risk for your clients and their heirs. That’s why many individuals are not waiting until retirement to prepare. Here’s an example of what someone could do now to protect their assets and their loved ones who will inherit them. Case Study: An asset for tax diversification Rick is age 55. He and his wife, Tina have two adult children. This couple recently sold their home and moved to a condo in town. They made a nice profit on the sale, and Rick is ready to use part of the money in a tax-efficient way. Rick’s goals • Finding an asset that offers tax-advantaged growth • Creating a legacy for his children without creating tax risk for them • Establishing his plan for care Rick’s concerns • Facing market risk and losing the profit he made on his home sale • Not knowing what income and capital gains taxes will be in the future The solution In conjunction with recommendation from Rick’s tax and estate planning team, Rick purchase a $100,000 Indexed Single Premium Universal Life Insurance policy as a differentiated asset within his portfolio. This will provide the liquidity of a full return of principal, tax advantaged growth, guarantees, an income tax-free legacy for his children, and income tax-free chronic illness benefits if he would ever need care. At the time of purchase, Rick chooses the Global Multi-Index Bonus HIGH PAR Strategy which can help his death benefit grow tax-deferred over time. He’ll have principal protection and will never face losses due to market performance. The outcome  Q. How can an annuity be used by an individual as an estate planning tool?

A. In order to avoid the potential tax and financial repercussions that a lump sum transfer can create, many individuals wish to protect their heirs by providing structure to the way assets are inherited. For these taxpayers, annuities, though commonly used as retirement income planning tools, can provide the solution. The reasons for using an annuity as a wealth transfer vehicle often mirror those that apply when a taxpayer is planning for retirement—the annuity creates a stream of consistent income over time, guaranteeing that the taxpayer’s beneficiary is provided for far into the future. This strategy can protect heirs who might be otherwise unable to manage a large one-sum payment, or who might have financial problems that could cause them to spend a large sum too quickly. Q. If an annuitant dies before a deferred annuity matures or is annuitized, is the amount payable at the annuitant’s death subject to income tax?

A. Yes, to the extent there are any gains. An annuity contract generally provides that if the annuitant dies before the annuity starting date, the beneficiary will be paid, as a death benefit, the greater of the amount of premiums paid or the accumulated value of the contract (although some contracts may provide additional “enhanced” death benefits as well). The gain, if any, is taxable as ordinary income to the beneficiary, and is measured by subtracting (1) investment in the contract (reduced by aggregate dividends and any other amounts that have been received under the contract that were excludable from gross income) from (2) the death benefit, including any enhancements. Should annuity buyers time the market? That is the question this thinkadvisor.com article tries to answer. Its conclusion? See below:

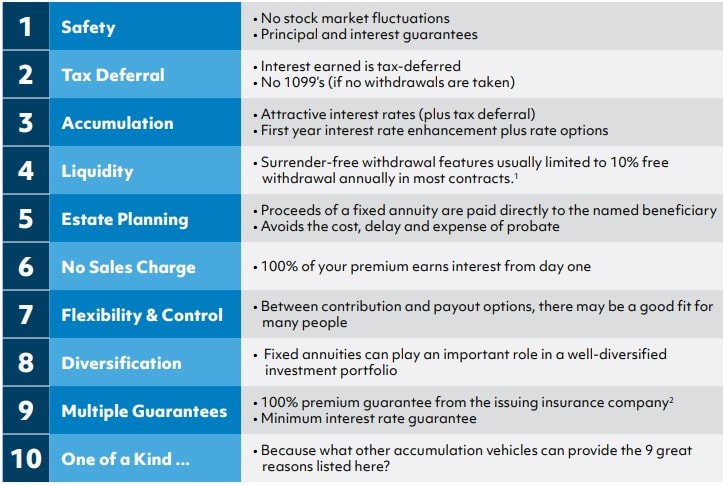

Below is a case study from AIG about how to maximize income during the early years of retirement. Safety, tax deferral and accumulation are just a few of the many reasons to include a fixed annuity in retirement portfolio.  In last blogpost, we compared different retirement income sources.

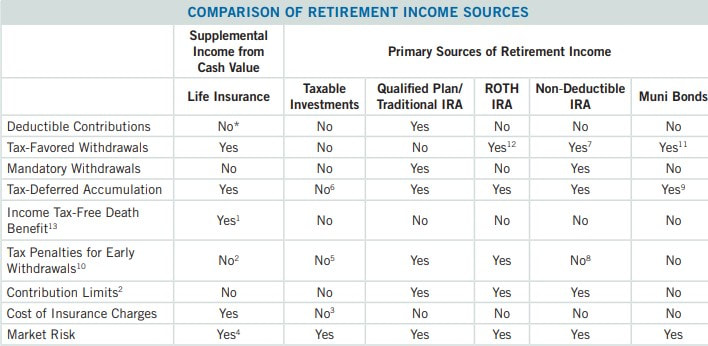

THINGS TO CONSIDER The primary purpose of life insurance is for death benefit protection, and this strategy assumes this to be a priority objective for the policyowner. 1. Life insurance premiums are not tax-deductible. 2. Life insurance policies classified as Modified Endowment Contracts (MECs) may be subject to tax when a loan or withdrawal is made, and a federal tax penalty of 10% may also apply to a MEC if the loan or withdrawal is taken prior to age 59½. 3. The policy cash value available for loans and withdrawals may be worth more or less than the original investment amount, depending on the performance of the policy crediting rate. Life insurance policies may also have surrender charges in the early policy years. Other factors that will affect cash values are the timely payments of premium and the performance of underlying investment accounts, where applicable. 4. Withdrawals and loans can reduce the policy death benefit and cash surrender value and may cause the policy to lapse. Lapse of a life insurance policy can cause the loss of the death benefit. Lapse of a life insurance policy with an outstanding loan may cause adverse income tax consequences. 5. For life insurance, the cash value available for loans and withdrawals may be worth more or less than the original premiums paid. Withdrawals from a life insurance policy may be subject to income tax after withdrawals exceed cost basis. 6. Taxable investments may be subject to income tax and/or capital gains tax. 7. Distributions from non-deductible IRAs must be pro-rated if the client has deductible IRA monies or earnings in the non-deductible IRA. 8. Contributions to qualified plans and traditional IRAs may be tax-deductible, subject to certain limits. 9. While qualified distributions from a ROTH IRA are generally federal income tax-free, if the ROTH IRA is a rollover IRA, a waiting period may apply before distributions will be tax-free. 10. The tax treatment of income from municipal bonds will vary with the type of bond and the issuing municipality. LIFE INSURANCE IN RETIREMENT PROVIDES THE FOLLOWING BENEFITS: 1. In the event of premature death during your working years, the income tax-free death benefit can protect your family, replace income, and complete financial obligations. 2. The policy’s cash value can be used to help supplement the income from your other retirement assets.  BENEFITS OF LIFE INSURANCE IN RETIREMENT PLANNING

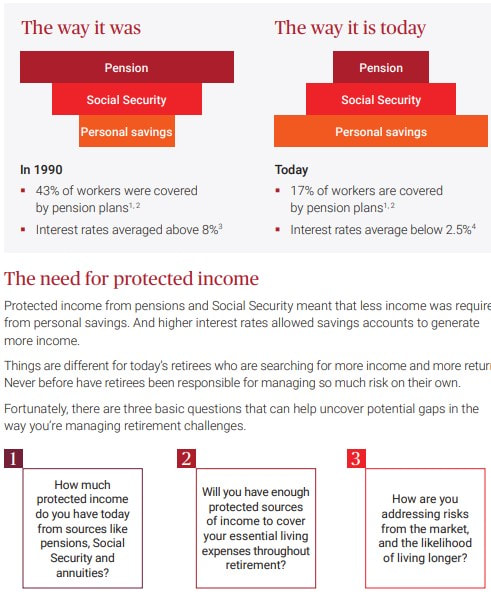

1. The life insurance death benefit will generally be received income tax-free by heirs. 2. The life insurance cash values can grow tax-deferred. 3. As long as the policy is not a Modified Endowment Contract (MEC), the client can generally take tax-free withdrawals up to basis out of the policy, and tax-free loans thereafter from the available cash value. 4. Accumulated cash value may be accessed by you or remain in the policy. In next blogpost, we will discuss 10 things to consider related to the table above. 3 questions to help uncover any gaps in your retirement plan -  1. Your estate should not typically be the named beneficiary of the policy. This will avoid:

2. Two or more backup (secondary) beneficiaries should be named. 3. At least every three years, a written confirmation of the status of policies and beneficiaries should be requested from the insurer’s Home Office. 4. The insurance product should match the problem. Be sure you have the right policy for your needs. 5. Above all, verify there’s enough life insurance to provide food, clothing and shelter, and to pay off debts so that those you love can continue in their present lifestyle. 6. Don’t name minors as outright beneficiaries. Instead:

7. Consider an ownership transfer of life insurance to others to save federal estate taxes. 8. Check to see if your business or practice can provide your family with insurance on a more cost-effective basis. 9. Remember that term insurance, by definition, will expire and contractually becomes more expensive as you grow older. 10. Don’t buy life insurance as though it were a commodity. The knowledge of your financial professional, the integrity of the insurer, and their commitment to service can make a major difference as to the cost effectiveness of the life insurance. In last blogpost, we discussed life insurance as an asset strategy. Now we will show it in action.

Helen’s objectives: Helen wants to make sure that her children and grandchildren receive a meaningful inheritance. While Helen expects to receive a 7% return on her investments over time, she is concerned that, in today’s environment, the assets might underperform. For example, if her assets receive only a 5% average annual return over time, her beneficiaries might receive substantially less than her expectations. Assuming a blended income and capital gains tax bracket of 27.5%, that 2% difference in return rate over 28 years could result in a difference of more than $3,000,000 in the legacy for her children. A down market near Helen’s death could have that type of effect on years of wealth accumulation. Helen’s wealth transfer strategy: As a hedge against that risk, Helen’s financial professional suggests she take $30,000 each year, or 1% of her accessible assets, and direct the funds to a life insurance policy on her life. She can own this policy outright, although she may want to consider using a trust. If structured properly, life insurance owned by an irrevocable trust will generally keep the proceeds of the life insurance out of the insured’s estate. This will prevent the proceeds from being subject to estate taxation. Estate taxes aren’t an issue for Helen, but for others they could be an issue. Helen’s results: Assuming a policy on Helen’s life (a 60-year-old female who receives an underwriting category of preferred non-tobacco user), her beneficiaries might see the following results. Each year’s life insurance premium is $30,000. That may purchase a life insurance benefit of $2,000,000. Helen’s portfolio is reduced slightly due to the premium expense, but the life insurance benefit gives her a potentially more effective transfer strategy. Additionally, the death benefit will ensure a return of the funds contributed, something few other financial assets can offer. In effect, by using her assets to buy life insurance, Helen is giving up some upside potential for greater safety in her wealth transfer strategy. By directing this relatively small amount of her net worth into life insurance, she adds a stabilizing element to the dollars ultimately transferred to her family (provided the policy stays inforce). If Helen received a lower rate of return, using life insurance could help offset the risk of loss or underperformance. Through the purchase of life insurance, Helen has, at least in part, shifted the risk of underperformance from her to the insurance company, provided she continues to pay the required premiums. Make a difference with life insurance Ultimately, at her life expectancy, Helen’s purchase of life insurance increases the amount passing to her beneficiaries.

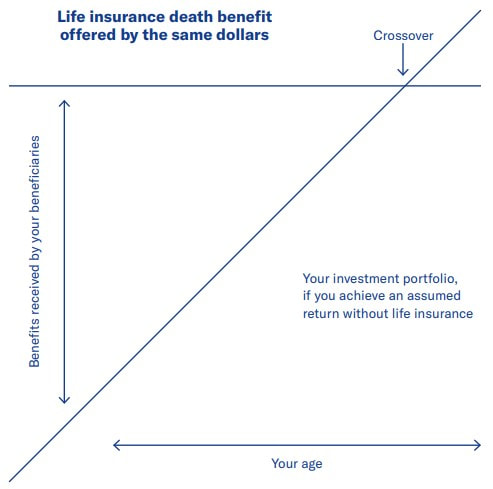

The greatest strength of life insurance lies in the ability to provide money to a family when someone passes away. Sometimes this amount can be many multiples of the premiums that were paid into the insurance policy. Many people think of life insurance only as a way to provide for a family after the loss of a breadwinner. But some families are also using life insurance as an asset to ensure that an inheritance can be passed on to their family, regardless of how their other assets perform. This is increasingly important to many families who are still uneasy after the 2008 market crash and unsure of where the market is headed. A badly timed down market can devastate a planned legacy for years. The chart below shows market fluctuations in recent years, based on the 5-year S&P 500® Index, without dividends. By taking a portion of your assets each year to cover the cost of life insurance premiums, you may be able to hedge a portion of your portfolio against fluctuations in the marketplace, because payment comes from the life insurance company, not your assets directly. Knowing that your beneficiaries will be cared for may also allow you to make other choices with your remaining assets — perhaps a more aggressive, growth-oriented strategy, or you might invest more conservatively, knowing you don’t need as much growth. How the strategy works A hypothetical example of how the strategy works can be seen in the chart below. It shows what you might expect from the same dollars if they were paid into a life insurance policy as premiums, or if they were placed in a hypothetical investment account. In the early years, life insurance death benefits typically offer substantially more than the hypothetical investment. As time goes on, the leverage offered by life insurance may be reduced as the non-life insurance assets grow and compound. At some point there is a crossover, where the growth in the investment account outweighs the benefit provided by the life insurance policy. Of course, it’s hard to know which strategy is more beneficial unless someone knows their precise life expectancy, and whether it is before or after this crossover point. However, this is a conversation you can have with your financial professional. They can run numbers for you and estimate the internal rate of return in the years before and after your life expectancy. For you to get the most out of your policy’s life insurance benefit, it has to stay inforce until you pass away. If your policy ends or terminates, or if you otherwise dispose of your policy before your death, your beneficiaries would receive a substantially reduced benefit, and any proceeds they would receive above the premiums paid into the contract could be subject to income taxation.  In next blogpost, we will show a case study to illustrate life insurance as an asset in action.

Case Study:

Chris is currently contributing to his employer-sponsored retirement savings accounts up to the 4% his company matches. He is also contributing to his Roth IRA up to the maximum contribution amount. He wants to live a comfortable retirement and would like to retire early, so he is saving as much as he can now and is looking for opportunities to maximize his retirement income potential. Chris’s Life Insurance Needs: Chris is a 40-year-old father of three who is currently in good health. In addition to his need for supplemental retirement savings, he also has a need for life insurance coverage to protect his children and spouse in case something should happen to him. Key facts and considerations:

To accomplish his goals, he looks at a combination of temporary and permanent life insurance solutions. He chooses to:

When Chris Retires After 20 years, Chris’ kids are grown up and on their own, so he lets his term policy expire. Based on a 6% projected crediting rate, after 20 years, Chris’ IUL policy is projected to have a death benefit of $374,290 and a cash value of $174,290. Chris decides to retire at age 60. Based on his projected cash value, Chris is able to start taking level distributions from his IUL policy in the amount of $14,329 per year for the next 20 years. This income stream will be income tax free (as long as the policy stays in force). If he waits to start taking his income until age 65 (still stopping premiums at age 60), his projected distribution amount increases from $14,329 to $18,097 for 20 years. An Added Benefit By purchasing an Income Advantage IUL policy, the client also receives an additional benefit. All policies come with Accelerated Death Benefit Riders for Terminal and Chronic Illness – included at no additional cost and with no additional underwriting. For Chronic Illness, the client can receive a benefit of up to $1,000,000 or 80% of the specified face amount (whichever is less). Centers for Medicare and Medicaid Services recently update their "Understanding Medicare Advantage Plans" brochure detailing the differences between original Medicare and Medicare Advantage plans. See the document below. Proposed tax increases. Elimination of Stretch IRAs. Worries over longer lifespans. Now is a compelling time to promote the advantages of nonqualified annuities. Take a loot at this flyer for timely market facts. If you have a deferred annuity, below is a case study to maximize its value by using Life Insurance.  Why Make a Life Insurance Gift?

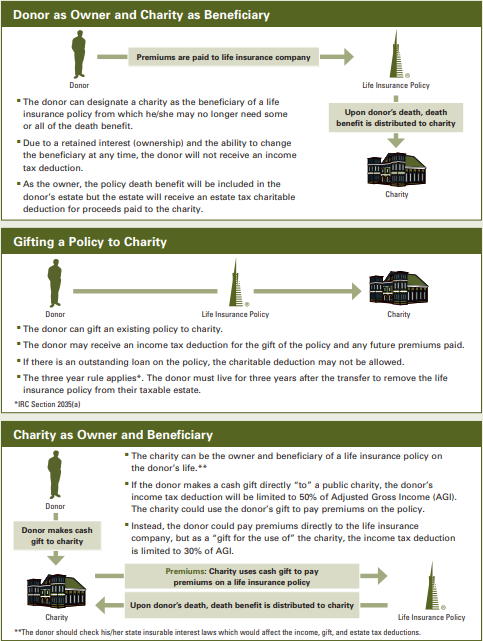

An insurance policy has the potential to create a substantial, cost-effective gift to charity through the policy's death bene t. The result is a gift that is much larger than the donor may otherwise have been able to make. Also, unlike a charitable bequest made in a will, a life insurance gift does not become a matter of public record and is made without the delays of probate. Premiums paid by the donor after a lifetime gift of a policy to charity are deductible for income tax purposes when the donor itemizes. When the charity is named as the policy beneficiary, the death proceeds paid to the charity are deductible for federal estate tax purposes. How Can a Donor Make a Gift of Life Insurance? A donor has three basic choices in making a charitable gift of life insurance:

What Are the Tax Considerations? A charitable gift of an existing life insurance policy can generate an income tax charitable deduction provided the donor assigns all rights. When considering a charitable gift of an existing policy, the donor has two choices:

Generally, when you make a charitable donation, you write a check that may be tax-deductible. However, there is another way you can give that allows your favorite charity to continue to receive your support, even after you’re gone.  John Smith wants to provide a significant gift to help a charity that he has volunteered much of his time to over the past several years. He has a life insurance policy that he has used to help fund the education of his two children. Now that both of them have their college degrees, John is considering three options in order to provide a gift to his charitable organization.

First, John can make the charity the beneficiary of part of his $500,000 life insurance policy. Since John would continue to be the owner of the policy, he would not receive an income tax deduction but his estate would receive an estate tax deduction for the portion that goes to charity. On the other hand, John can gift his life insurance policy to the charity and can claim an income tax deduction in the year that the policy is gifted. By transferring ownership of the policy to the charity, John has given up control and any benefits from the policy his children might receive, but the policy proceeds may be excluded from his estate. The three year rule applies, if John were to die within three years following the gift of the policy, the policy would be included in John’s estate. John can also allow the charity to purchase a new life insurance policy on his life. By allowing the charity to make the initial purchase of the policy, the policy proceeds will be excluded from his estate. In addition, John may receive an income tax deduction for cash gifts to the charity to make premium payments. |

AuthorPFwise's goal is to help ordinary people make wise personal finance decisions. Archives

September 2022

Categories

All

|

RSS Feed

RSS Feed