When you convert an IRA to Roth IRA, you need to note that all the IRAs you own are considered 1 IRA, no matter how many accounts you have. Your tax liability is based on 2 things: the taxable income generated by the conversion and your applicable tax rate.

To figure out how much of a conversion from a traditional IRA to a Roth IRA may be taxable, you need to note there are 2 types of contributions.

Estimating the taxable income from a conversion is straightforward if you've never made nondeductible contributions to any traditional IRA. If that is the case, whatever amount you convert will all be taxable income.

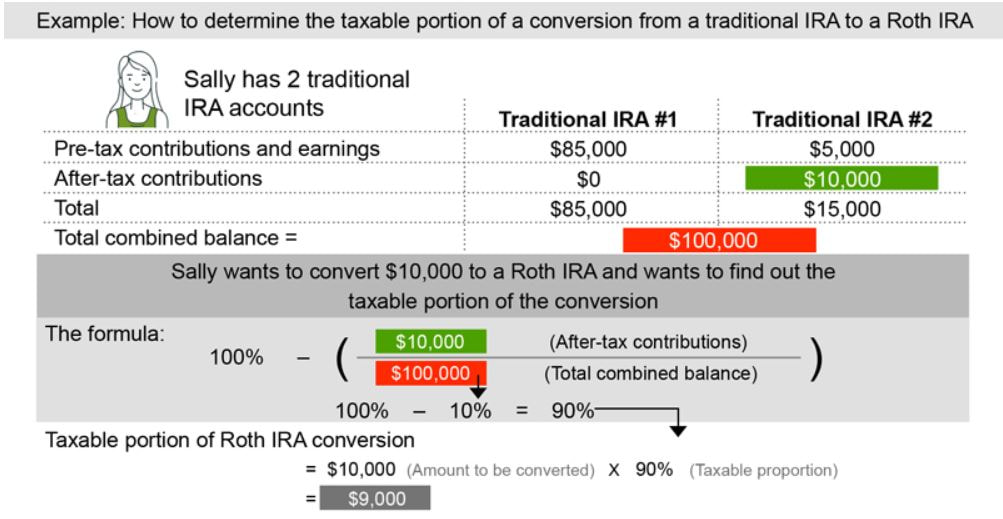

Note that earnings are always taxable when converted, whether they come from deductible or nondeductible contributions, so for purposes of figuring out taxes on a conversion, you can think of your balances as falling into just 2 categories: (1) nondeductible contributions, and (2) everything else. According to IRS rules, you cannot cherry-pick and convert just nondeductible contributions, leaving deductible contributions and earnings in the account, in order to avoid taxes. Instead, you must figure out the proportion of your total traditional IRA balances that is composed of nondeductible contributions, then use that percentage to find out how much of your conversion will not be taxable. Note that inherited IRAs are excluded in this calculation.

Keep state taxes in mind too. A Roth IRA conversion is a taxable event. If your state has an income tax, the conversion will generally be treated as taxable income by your state as well as by the federal government.

Below is an example that helps you understand how to estimate the taxable portion of the conversion.

To figure out how much of a conversion from a traditional IRA to a Roth IRA may be taxable, you need to note there are 2 types of contributions.

- Deductible contributions. These are contributions that are deducted from your taxable income for the tax year in which the contributions were made.

- Nondeductible contributions. Any contribution for which you do not take a tax deduction is known as a nondeductible contribution. Such contributions create what is sometimes called "basis" in your traditional IRA.

Estimating the taxable income from a conversion is straightforward if you've never made nondeductible contributions to any traditional IRA. If that is the case, whatever amount you convert will all be taxable income.

Note that earnings are always taxable when converted, whether they come from deductible or nondeductible contributions, so for purposes of figuring out taxes on a conversion, you can think of your balances as falling into just 2 categories: (1) nondeductible contributions, and (2) everything else. According to IRS rules, you cannot cherry-pick and convert just nondeductible contributions, leaving deductible contributions and earnings in the account, in order to avoid taxes. Instead, you must figure out the proportion of your total traditional IRA balances that is composed of nondeductible contributions, then use that percentage to find out how much of your conversion will not be taxable. Note that inherited IRAs are excluded in this calculation.

Keep state taxes in mind too. A Roth IRA conversion is a taxable event. If your state has an income tax, the conversion will generally be treated as taxable income by your state as well as by the federal government.

Below is an example that helps you understand how to estimate the taxable portion of the conversion.

RSS Feed

RSS Feed