Take these eight steps now:

- Contribute to your retirement accounts.

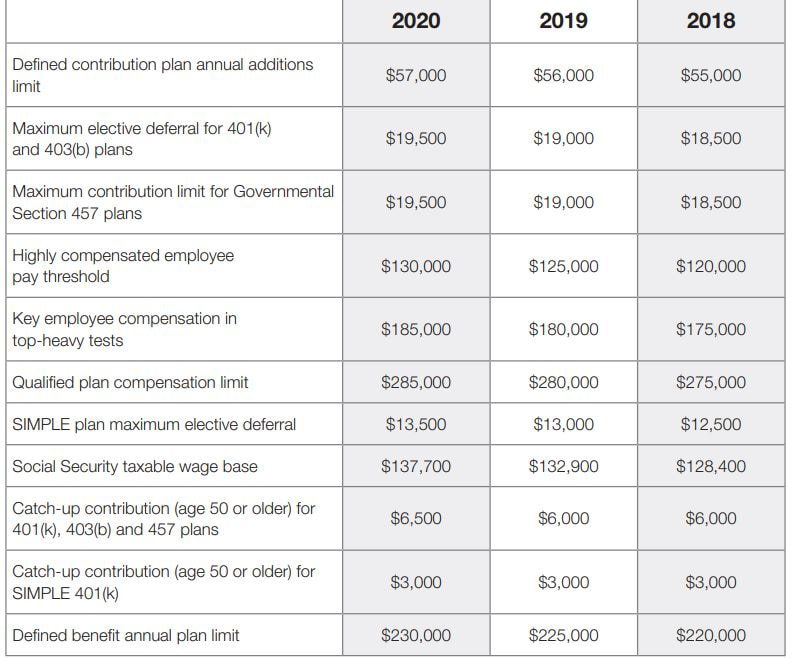

If you work for a company that matches your 401(k) contribution, try to contribute at least up to the percentage they match. Otherwise, you’re leaving money on the table. - Make your required minimum withdrawal from your IRA.

Do you have a traditional IRA? Starting at 70 ½, the IRS requires you to withdraw a certain amount each year, known as a required minimum distribution (RMD). - Use up your flexible spending account (FSA).

Find out the deadline for using this money if you have an FSA, since you will lose it if you don’t use it by the deadline. - Think through your holiday spending.

Now is the time to also think about paying down any debt or padding your emergency fund. - Check your credit reports.

If you haven’t checked your credit reports in the last 12 months, the end of the year is a great time to do so. - Consider year‑end charitable giving.

In addition to using your dollars to support a cause you are passionate about; many charitable contributions of money or property are also tax deductible. - Assess the last 12 months.

Reflect on how you did this year from a financial standpoint. Think about what went right and what would you like to adjust. - Plan for the next 12 months.

If your assessment of the past year calls for some changes, use that information to start planning for the new year.

RSS Feed

RSS Feed