Q. What is Tax Gain Harvesting?

A. Most people are familiar with Tax Loss Harvesting, but Tax Gain Harvesting could be another important tax planning tool for the right situations.

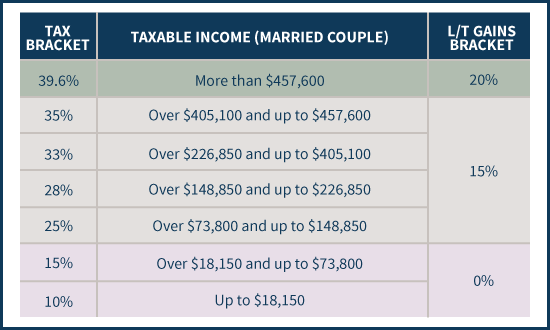

To start with, the table below shows the Tax bracket and income levels:

A. Most people are familiar with Tax Loss Harvesting, but Tax Gain Harvesting could be another important tax planning tool for the right situations.

To start with, the table below shows the Tax bracket and income levels:

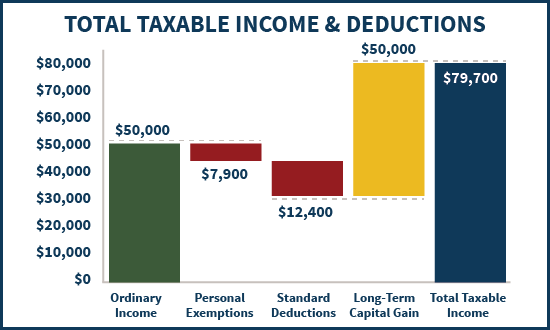

Now imagine a married couple who have $50,000 of ordinary income, and then recognize a $50,000 long-term capital gain. They will each be eligible for a $3,950 personal exemption (a total of $7,900 for the two of them), and the $12,400 standard deduction. Thus, their total deductions will be $3,950 x 2 + $12,400 = $20,300, which means their ordinary income will be $50,000 - $20,300 = $29,700 and their $50,000 of long-term capital gains go on top.

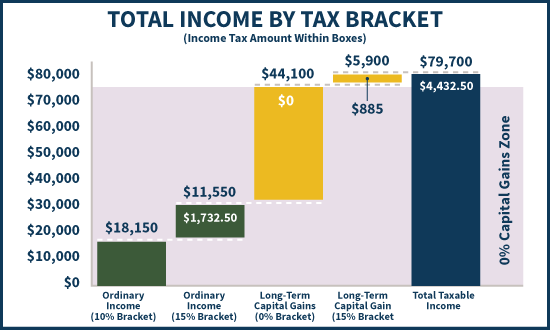

From there, the ordinary income fills up the tax brackets first, which means the first $18,150 falls in the 10% ordinary bracket, and the next $11,550 is in the 15% bracket. From there, the long-term capital gains kick in, which means the next $44,100 are eligible for the 0% long-term capital gains rate (up to the $73,800 threshold that forms the top of the "0% capital gains zone" shown below) and then the last $5,900 are taxed at the 15% long-term capital gains rate.

Ultimately, thanks to the favorable stacking sequence, the couple’s total tax bill will be only $18,150 x 10% + $11,550 x 15% + $5,900 x 15% = $4,432.50, or an effective tax rate of only about 4.4% on $100,000 of total income!

RSS Feed

RSS Feed