We shared strategy 1 here, now strategy 2.

Strategy No. 2: Claim early due to health concerns

A couple with shorter life expectancies may want to claim earlier.

How it works: Benefits are available at age 62, and full retirement age (FRA) is based on your birth year.

Who it may benefit: Couples planning on a shorter retirement period may want to consider claiming earlier. Generally, one member of a couple would need to live into their late 80s for the increased benefits from deferral to offset the benefits sacrificed from age 62 to 70. While a couple at age 65 can expect one spouse to live to be 85, on average, couples who cannot afford to wait or who have reasons to plan for a shorter retirement, may want to claim early.

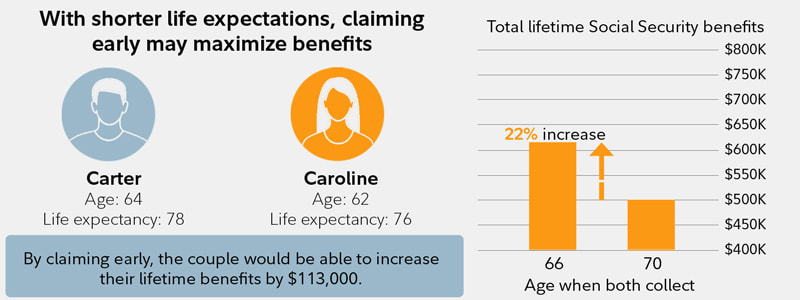

Example: Carter is age 64 and expects to live to 78. He earns $70,000 per year. Caroline is 62 and expects to live until age 76. She earns $80,000 a year.

By claiming at their current age, Carter and Caroline are able to maximize their lifetime benefits. Compared with deferring until age 70, taking benefits at their current age, respectively, would yield an additional $113,000 in benefits—an increase of nearly 22%.

Strategy No. 2: Claim early due to health concerns

A couple with shorter life expectancies may want to claim earlier.

How it works: Benefits are available at age 62, and full retirement age (FRA) is based on your birth year.

Who it may benefit: Couples planning on a shorter retirement period may want to consider claiming earlier. Generally, one member of a couple would need to live into their late 80s for the increased benefits from deferral to offset the benefits sacrificed from age 62 to 70. While a couple at age 65 can expect one spouse to live to be 85, on average, couples who cannot afford to wait or who have reasons to plan for a shorter retirement, may want to claim early.

Example: Carter is age 64 and expects to live to 78. He earns $70,000 per year. Caroline is 62 and expects to live until age 76. She earns $80,000 a year.

By claiming at their current age, Carter and Caroline are able to maximize their lifetime benefits. Compared with deferring until age 70, taking benefits at their current age, respectively, would yield an additional $113,000 in benefits—an increase of nearly 22%.

Read strategy 3 here.

RSS Feed

RSS Feed