We discussed strategy 2 here, now strategy 3.

Strategy No. 3: Maximize the survivor benefit

Maximize Social Security—for you and your spouse—by claiming later.

How it works: When you die, your spouse is eligible to receive your monthly Social Security payment as a survivor benefit, if it's higher than their own monthly amount. But if you start taking Social Security before your full retirement age (FRA), you are permanently limiting your partner's survivor benefits. Many people overlook this when they decide to start collecting Social Security at age 62. If you delay your claim until your full retirement age—which ranges from 66 to 67, depending on when you were born—or even longer, until you are age 70, your monthly benefit will grow and, in turn, so will your surviving spouse's benefit after your death.

Who it may benefit: This strategy is most useful if your monthly Social Security benefit is higher than your spouse's, and if your spouse is in good health and expects to outlive you.

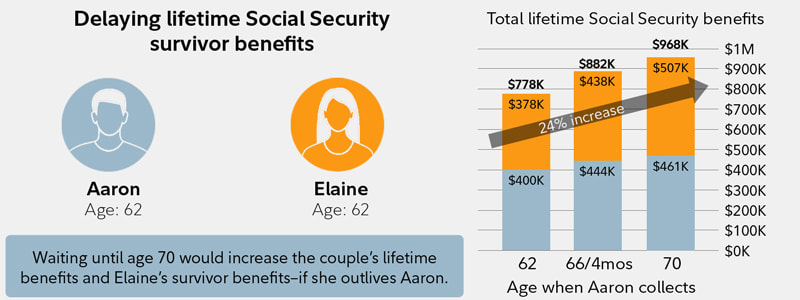

Example: Consider a hypothetical couple who are both about to turn age 62. Aaron is eligible to receive $2,000 a month from Social Security when he reaches his FRA of 66 years and 6 months. He believes he has average longevity for a man his age, which means he could live to age 85. His wife, Elaine, will get $1,000 at her FRA of 66 years and 6 months and, based on her health and family history, anticipates living to an above-average age of 94.

The couple was planning to retire at 62, when he would get $1,450 a month, and she would get $725 from Social Security. Because they’re claiming early, their monthly benefits are 27.5% lower than they would be at their FRA. Aaron also realizes taking payments at age 62 would reduce his wife's benefits during the 9 years they expect her to outlive him.

Strategy No. 3: Maximize the survivor benefit

Maximize Social Security—for you and your spouse—by claiming later.

How it works: When you die, your spouse is eligible to receive your monthly Social Security payment as a survivor benefit, if it's higher than their own monthly amount. But if you start taking Social Security before your full retirement age (FRA), you are permanently limiting your partner's survivor benefits. Many people overlook this when they decide to start collecting Social Security at age 62. If you delay your claim until your full retirement age—which ranges from 66 to 67, depending on when you were born—or even longer, until you are age 70, your monthly benefit will grow and, in turn, so will your surviving spouse's benefit after your death.

Who it may benefit: This strategy is most useful if your monthly Social Security benefit is higher than your spouse's, and if your spouse is in good health and expects to outlive you.

Example: Consider a hypothetical couple who are both about to turn age 62. Aaron is eligible to receive $2,000 a month from Social Security when he reaches his FRA of 66 years and 6 months. He believes he has average longevity for a man his age, which means he could live to age 85. His wife, Elaine, will get $1,000 at her FRA of 66 years and 6 months and, based on her health and family history, anticipates living to an above-average age of 94.

The couple was planning to retire at 62, when he would get $1,450 a month, and she would get $725 from Social Security. Because they’re claiming early, their monthly benefits are 27.5% lower than they would be at their FRA. Aaron also realizes taking payments at age 62 would reduce his wife's benefits during the 9 years they expect her to outlive him.

RSS Feed

RSS Feed